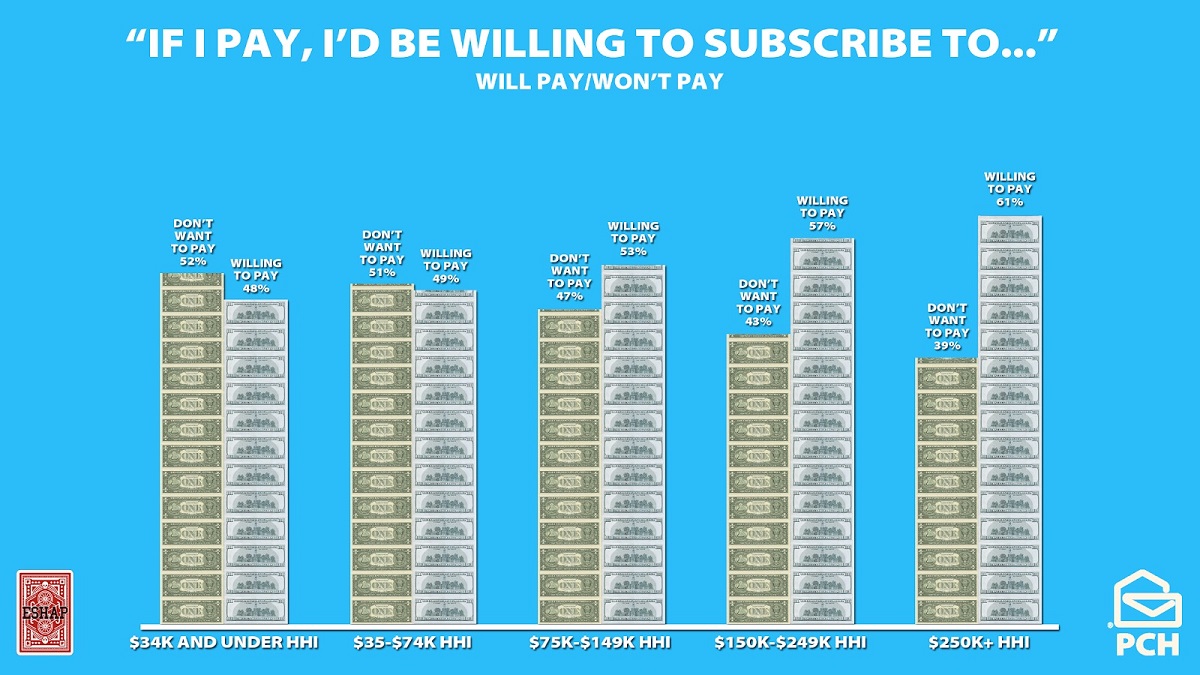

Enterprises worldwide are increasing budget for growing data storage needs as public cloud storage capacity continues to expand at a relentless pace.

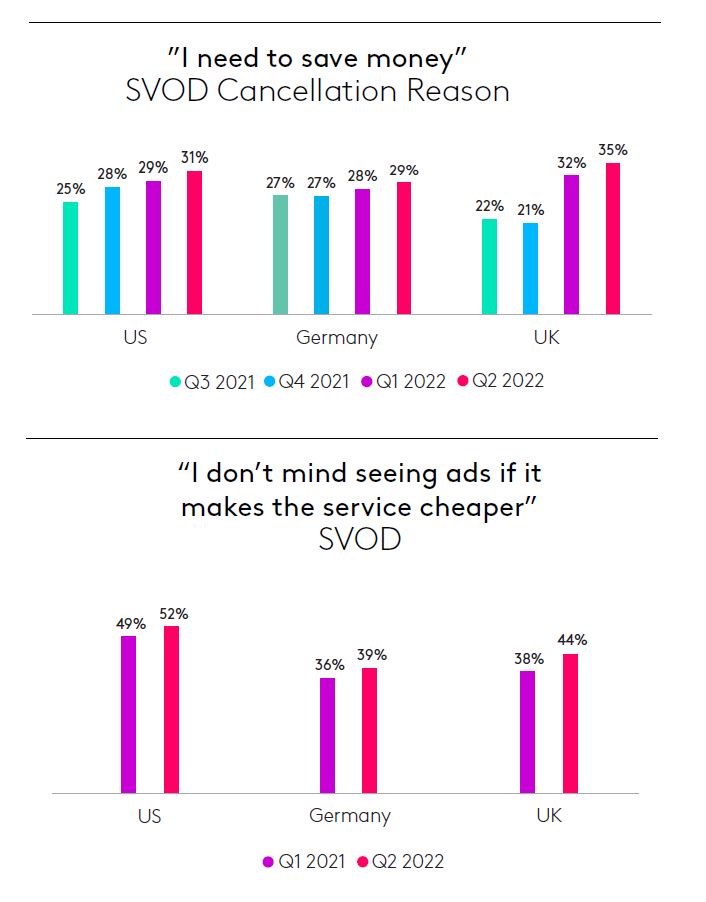

The cloud storage market is plagued by inefficient budgeting and overspending. Data from Wasabi sheds light on an unfortunate truth: storage services fees account for 48% of total cloud storage bills on average.

While the perceived value of enterprise data might be limitless, storing and accessing that data, on the other hand, has a very real cost. More than half of organizations exceeded their cloud storage budget in 2022. This highlights a significant pain point for enterprises, and an opportunity to improve as they assess cloud storage spending going forward.

The majority of organizations will spend more on expanding cloud storage capacity in 2023 despite a huge number of them blowing their budgets in 2022.

The “ugly truth” is that enterprises are spending almost as much on storage fees as they are on storage capacity, finds storage vendor Wasabi, which compiled the “2023 Cloud Storage Index Executive Summary Report,” pointing to significant improvements to be gained in billing/fee structures and multicloud deployments.

Wasabi analyzed survey results from 1,000 IT decision-makers worldwide to provide insight into how corporations across sectors including energy, finance, and media are strategizing cloud storage.

Its data confirms the relentless pace of data growth in the cloud, with 84% of respondents expecting the amount of data they store in the public cloud to increase this year.

Today, organizations allocate 14% of their total IT budgets to public cloud storage services, on average. Wasabi expect this proportion to expand, as overall IT budgets grow slowly or remain relatively stagnant in 2023, and more dollars are allocated to high-growth IT segments like cloud infrastructure.

However, more than half (52%) of organizations exceeded their budgeted spend on cloud storage in 2022, illustrating a significant pain point which many users may look to address this year.

The worst offenders were new adopters. 72% of respondents who adopted public cloud storage services in the past 12-24 months exceeded their budget.

The reasons why organizations exceeded their budget expectations include incurring higher data operations fees (e.g., cross-region replication, object tagging, transfer acceleration) than expected.

Cr: Wasabi

Also, migration of “additional applications/data” to the cloud was higher than originally anticipated. Others reported higher API call fees (e.g., reads/writes) and higher data retrieval fees than expected.

“Fees can be notoriously difficult to predict,” said Andrew Smith, senior manager of strategy and market intelligence at Wasabi. “As a result, they are a major reason why more than half of organizations we surveyed said that they exceeded their budgeted spending on cloud storage services in 2022. Understanding the cloud storage bill was the number one challenge associated with cloud storage migration. The survey data also sheds light on one of the industry’s unfortunate truths: A large proportion of storage bills are allocated to various fees. Specifically, respondents said storage fees account for 48% of their total cloud storage bill on average.”

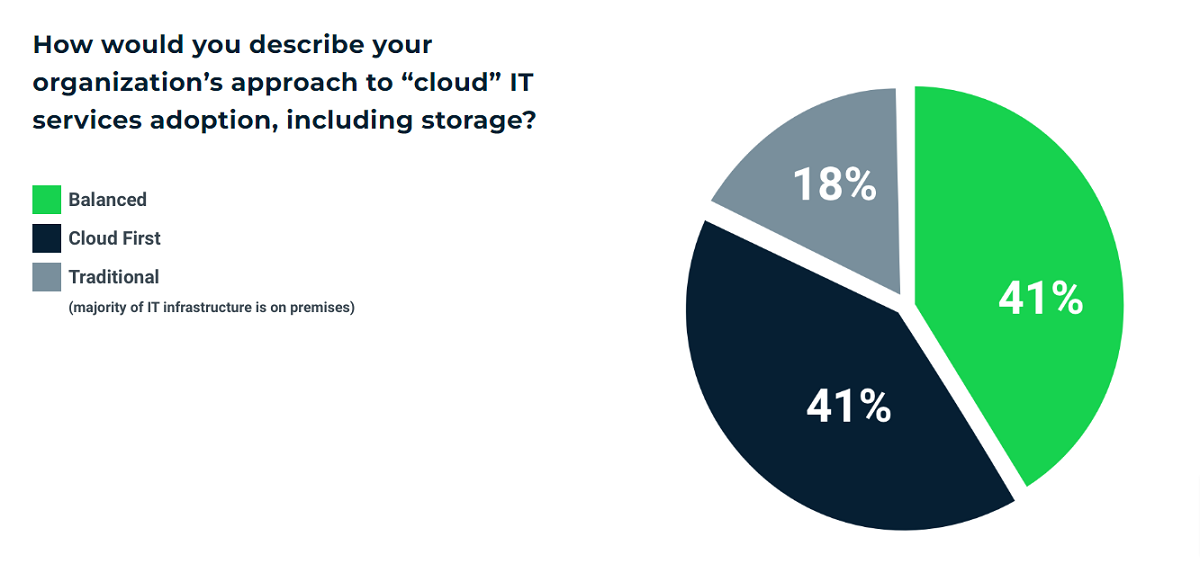

Wasabi’s survey also confirms that many enterprises are using more than one public cloud infrastructure provider: 57% of organizations use more than one public cloud storage provider.

“Nothing groundbreaking here, but what is interesting are the reasons why many organizations have adopted multiple cloud providers for storage, and what they believe the key benefits and challenges of this type of strategy are,” noted Smith.

Almost 90% of those surveyed indicated that they had migrated storage from on premises to the public cloud within the last year. Interestingly, the top reasons driving migration were not cost related. Instead, users were spurred by the need for better infrastructure resilience, durability, and scalability.

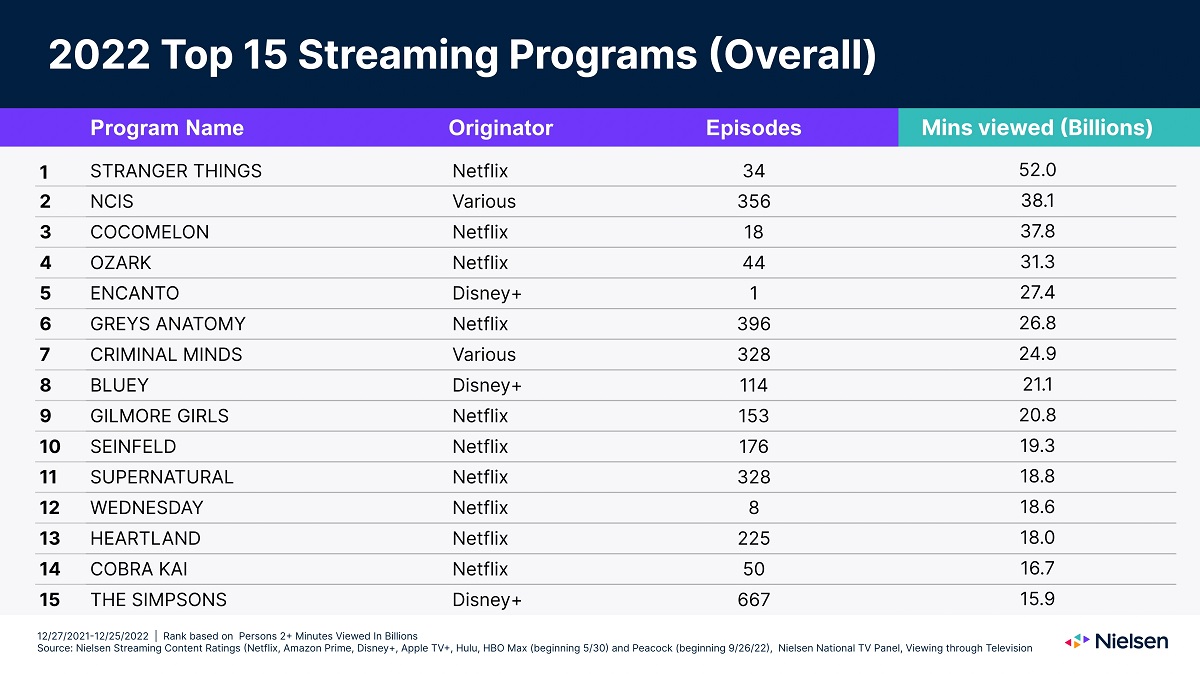

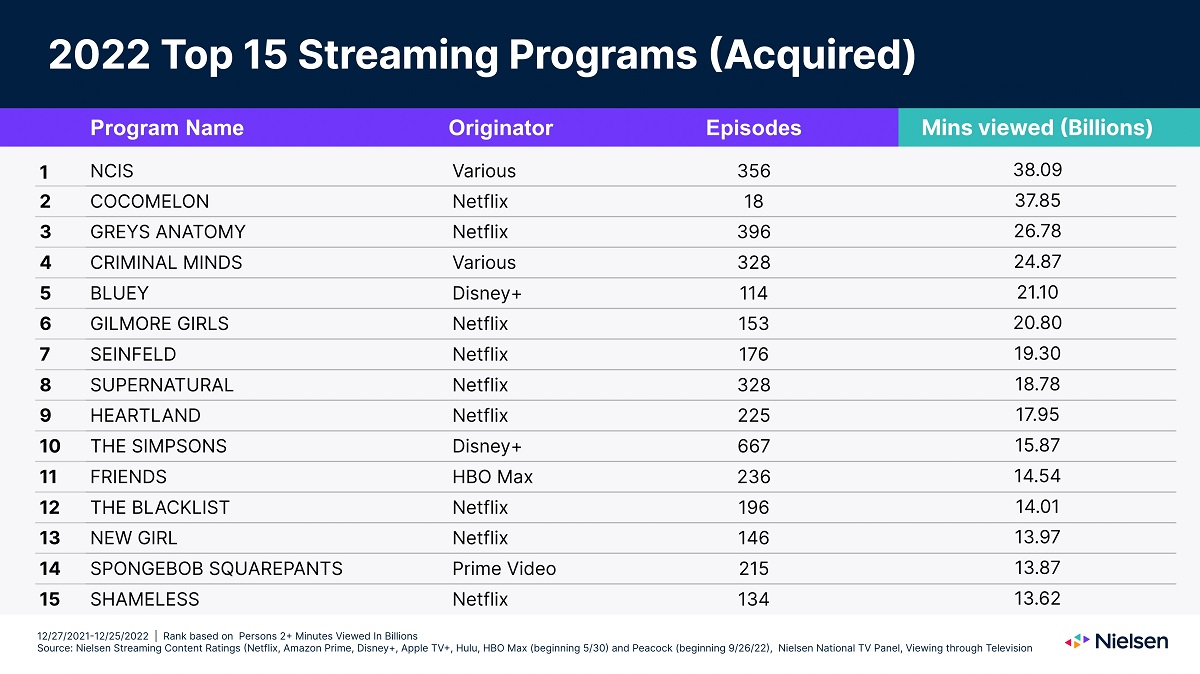

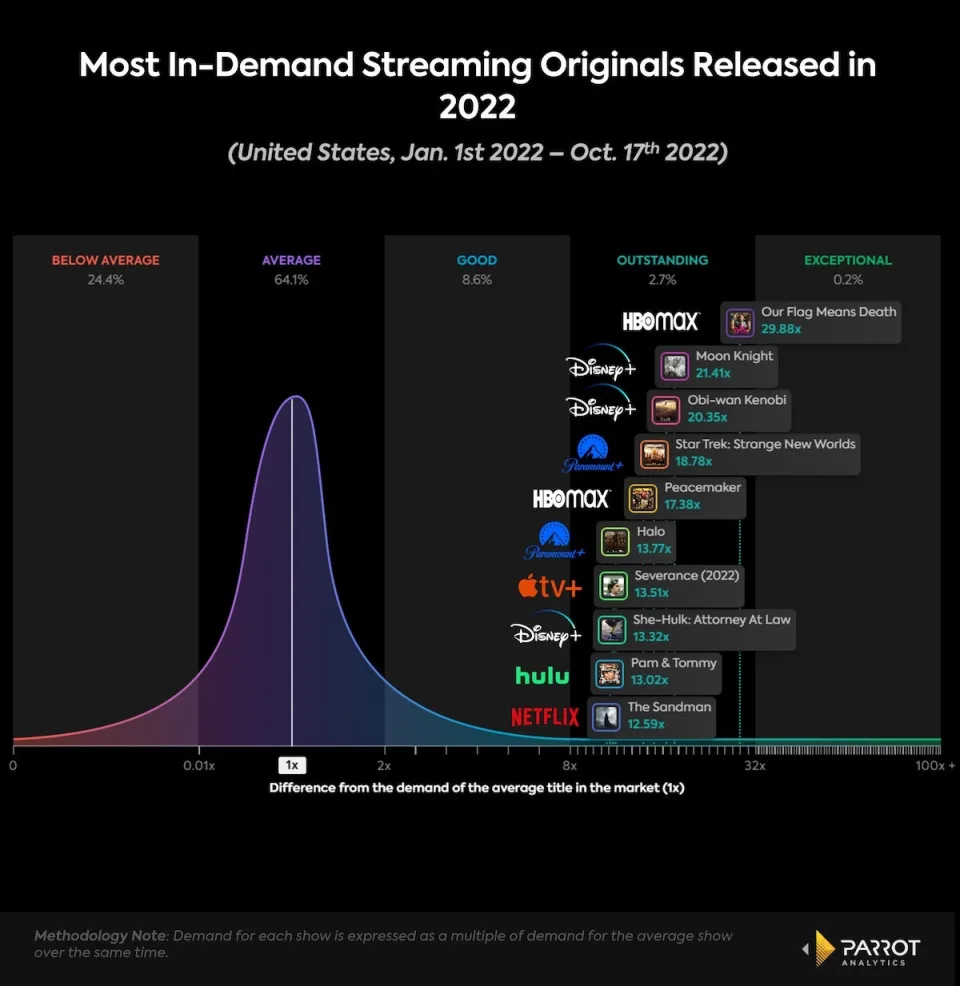

Americans streamed more than 19 million years’ worth of content last year, a total that was at least partly driven by original film and drama, according to Nielsen. Among the most popular hits were Netflix’s Stranger Things and Disney+ animated feature Encanto.

In the ratings agency’s end-of-year streaming rankings, Netflix shows lock-out the top ten. Stranger Things came out on top of both original and acquired content as the most streamed TV show in 2022, amassing 52 billion minutes viewed for a total of 34 episodes (spanning all four seasons).

The dominance of original content is underscored even more by the fact that there are only 34 episodes of Stranger Things, while there are 192 episodes of The Office, finds Nielsen.

The overall streaming figure of 19 million years is up 27% over 2021 (15 million years’ worth) but not quite achieving the earlier pandemic record-highs of 2020.

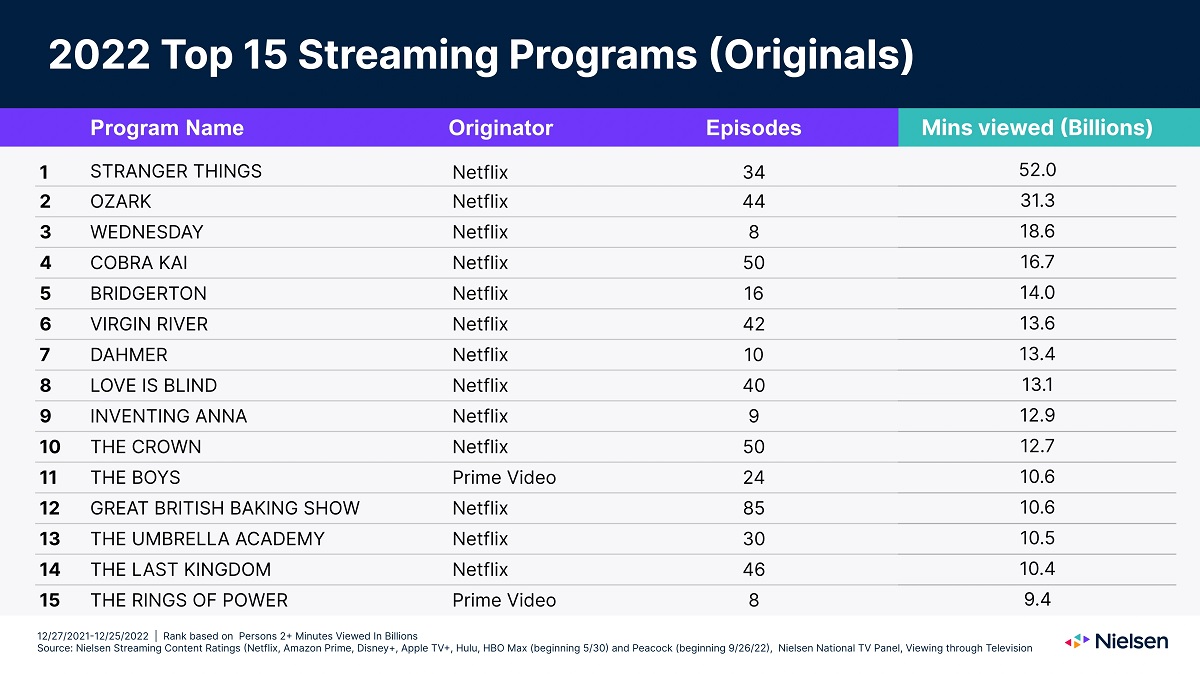

Another notable Netflix title on the originals ranking was Wednesday, taking third place at 18.6 billion minutes streamed despite debuting in late November with just 36 days of availability on Netflix to make the cut for this chart. Ozark came in second in the original-only list (31.3 billion minutes) but fourth place in the overall ranking.

Netflix locks out the top 10 streaming episodic shows with Amazon Prime’s The Boys coming in at 11 and The Rings of Power at number 15 (9.4 billion minutes).

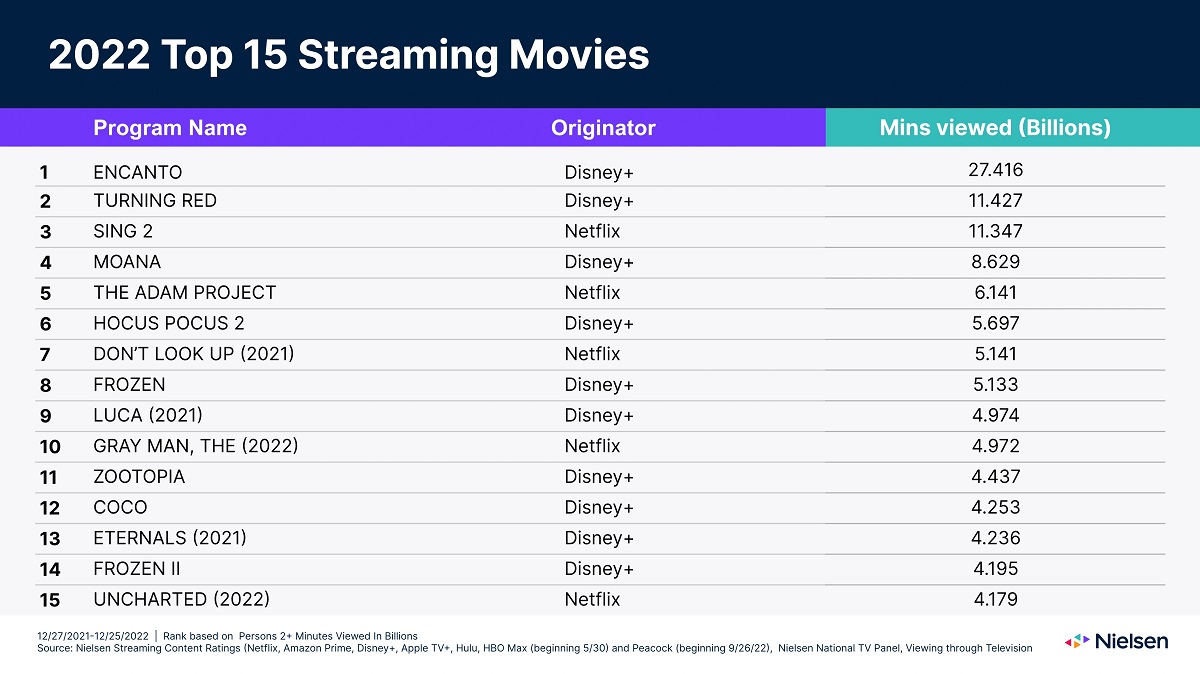

When it comes to original movies on streamers, Disney is the winner.

Encanto was the most streamed movie in 2022 with 27.4 billion minutes viewed and taking fifth in Nielsen’s original and acquired streaming ranking. Turning Red (11.4 billion minutes), Moana (8.6 billion minutes) and Hocus Pocus 2 (5.7 billion minutes) were other big hits for Disney+.

As you can see from the chart, it’s far from all about originals. The long-running procedural drama NCIS was the second most-watched show in 2022, gaining 38.1 billion minutes viewed across 356 episodes.

Nielsen said, “This highlights the immense attraction that library content holds for viewers who spent billions of minutes throughout the year watching popular titles like Grey’s Anatomy, Bluey, Seinfeld, Criminal Minds and the Simpsons.”

Whether acquired or original, though, Netflix still dominates as originator. The streaming service took 10 out of the 15 spots among 2022 streaming programs overall. Disney+ nabbed three spots followed by two spots for programs on multiple platforms. Netflix in fact was in command across overall, original and acquired streaming programs. Disney+ only overtook the behemoth in streaming movies thanks in part to its deep library of family favorites.

But will Netflix be able to stay top dog in 2023? HBO Max and Peacock, both of which will see their first full years of Nielsen rankings inclusion in 2023, could shake things up.

Big content spends, tapping emerging markets, and automated versioning: these are just a few of the strategies OTT companies are turning to in the fight for dominance in the global marketplace. Stay on top of the business trends and learn about the challenges streamers face with these hand-curated articles from the NAB Amplify archives:

How streamers can use the lessons learned from the past year in 2023 to help rebound from recent subscriber losses and stock price declines.

February 6, 2023

Jim Louderback: Five Developments Now Disrupting the Creator Economy

BY JIM LOUDERBACK

TL;DR

YouTube’s ad revenue continues to slide, but Shorts growth may buoy results later this year for everyone.

Snap is suddenly relevant to creators with some making over $20k a month.

Twitter will pay creators – but there’s a predatory twist.

Some early signs of TikTok views flattening out amid a new focus on transparency – but questions remain about trust and oversight.

The Supreme Court’s revisiting of Section 230 might be the most devastating move of all.

This Week 2-6-2023: Big changes are underway in the creator economy as top platforms deal with revenue drops and competition from new players. YouTube’s ad revenue continues to slide, but Shorts growth may buoy results later this year for everyone. Snap is suddenly relevant to creators with some making over $20k a month. Twitter will pay creators – but there’s a predatory twist. Some early signs of TikTok views flattening out amid a new focus on transparency – but questions remain about trust and oversight. And the Supreme Court’s revisiting of Section 230 might be the most devastating move of all. All that plus a new BHAP feature in this week’s newsletter! It’s the first full week of February and here’s what you need to know.

YouTube’s Terrible Quarter – What it Really Means: The ad recession has arrived, with YouTube’s quarterly ad revenue declining 8% from last year. At the very least that means less payout to creators, which should continue to incent those creators to diversify their revenue mix off-platform. YouTube also disclosed Shorts views jumped to 50 billion per day, and it started sharing Shorts ad revenue with creators last week as well. Is the revenue problem structural or cyclical? I think it’s mostly cyclical, as advertising is typically first to drop during a business pullback. But as short-form video eats into longer-form viewing it’s imperative that YouTube monetize those 50 billion DAUs at close to VOD rates. Longer term I think more creators will see these platforms as top-of-funnel awareness machines and instead focus on conversion instead of just creation.

Signs of a Possible TikTok View Decline: DoubleT may have hit the wall – or maybe it’s just a victim of its own success. Brendan Gahan teamed up with Trendpop to look at average views for videos that surpassed 100k. In January those videos saw over 20% less views per video than a month ago. It’s not definitive, but an interesting signal. Couple that with threats of shutdown, an errant balloon spiking U.S.-China tension and Shorts growth and perhaps there’s fire inside the smoke. In a related story, Trung Phan unpacks the TikTok Family Guy Pipeline, calls the platform “the apex predator in the attention game” and calls for it to be banned. Compelling analysis. Also sludge.

Twitter’s Predatory New Pay to Play Scheme: Twitter claims that it now pays creators, but also says that you won’t get paid unless you pay them first. That’s right, unless you buy a paid “Blue Check” plan, any money you’ve earned won’t actually accrue to you. It’s a predatory plan, because it will likely inspire a legion of hopeful creators to pony up month after month – when only a lucky few actually make any money. Shame on Twitter for preying on the little guys.

Supreme Court Decision Could Change Social Media Forever: You’ll be reading a lot about “Section 230” over the next few months. That’s because the Supreme Court will be revisiting the law that protects social platforms from being responsible for content on their platforms. It might just cause a few algorithmic changes – but it could also drastically impact everything from Reddit upvoting to Wikipedia community updates, Yelp reviews and Discord communities. I’m concerned, as governments have shown a frustratingly consistent inability to understand how technology and the internet really work.

TikTok’s Plan for Transparency – More Questions Than Answers: TikTok has developed an elaborate plan to separate its U.S.-based data from the rest of the world, along with building a monitoring and compliance infrastructure. The Platformer was invited to hear about it, and detailed what they learned (not much) from that discussion. Lawfare has a more in-depth look at how “Project Texas” will work, but it seems most of the onus of trust is passing on to Oracle. Security researcher Klon Kitchen (as quoted by the Platformer) says that “TikTok is adopting a ‘catch me if you can’ strategy like the one previously employed by Huawei.” My issue is that even if data is stored on Oracle Cloud’s U.S. servers it can still be accessed from anywhere in the world. And why is Oracle nominating the key oversight team? Can we trust Oracle? Lots of questions, not a lot of answers.

YouTube exec Andrew Leonard attempts to create a creator/influencer/celebrity taxonomy. I’m not sure that story-telling is the key differentiator but worth a read.

Great post on what really works on TikTok from Duolingo’s Zaria Parvez – the brain behind the bird. Can’t wait for the rest of the series.

An interesting look at the strategy and tactics that an interactive multi-player game used to create organic TikTok videos that drove over 100k installs.

TikTok comes up with its own “Strike” system – I still have PTSD from YouTube’s early efforts.

WEEKLY BHAP: I recently spoke about the creator economy at a corporate retreat, and then led a discussion on the future. As part of that I put together some big predictions to use if the audience was quiet. I didn’t need them. So instead of dropping them into the bit bucket I’m going to surface one each week until I run out of ideas. Here’s this week’s BHAP:

Either this year or next year U.S. workplace regulators will make an example of a top YouTube-led company by suing them for labor law violations, discrimination and/or ignoring harassment on the job. Similar to how the SEC made an example of Kim Kardashian last fall for pumping a crypto security without disclosure, toxic workplace cultures among creator-led companies will be under the microscope. I’ve heard a lot of anecdotal stories about creator-led companies violating workplace law – in large part because they just don’t know and haven’t been trained. This issue will soon come to the fore.

Thanks so much for reading and see you around the internet. Send me a note with your feedback, or post in the comments! Feel free to share this with anyone you think might be interested, and if someone forwarded this to you, you can sign up and subscribe on LinkedIn for free here!

Three different topics impacting the Creator Economy: The ban or sale of TikTok, Meta’s latest layoffs, and the release of GPT4.

March 17, 2023

Posted

February 1, 2023

Nominations Are Open for the NAB Show Excellence in Sustainability Awards

TL;DR

NAB Show is now accepting entries for the Excellence in Sustainability Awards, recognizing outstanding innovations in media technology that promote the conservation and reusability of natural resources and foster economic and social development.

Excellence in Sustainability Awards categories include the Sustainability Champion Award, the Sustainability Leadership Award, and the Sustainability Product or Service Award.

Winners of the NAB Show Excellence in Sustainability Awards will be recognized during a Main Stage ceremony at NAB Show on April 16, 2023, in Las Vegas.

NAB Show is now accepting entries for the Excellence in Sustainability Awards. The awards recognize outstanding innovations in media technology that promote the conservation and reusability of natural resources and foster economic and social development.

“Sustainability efforts not only benefit the planet and society but also make good business sense,” said Chris Brown, executive vice president of Global Connections and Events at the National Association of Broadcasters.

“In addition to providing global recognition for sustainability leaders within our industry, NAB Show is committed to working with our vendors and partners on progressive approaches that inspire the NAB Show community to take collective action in this area.”

Excellence in Sustainability Awards categories include:

The Sustainability Champion Award — Honoring individuals who demonstrate a passion in influencing their team or organization to achieve a more sustainable pathway.

The Sustainability Leadership Award — Honoring organizations that have launched or completed sustainability initiatives.

The Sustainability Product or Service Award — Honoring products or services that significantly improve sustainability or provide sustainable market alternatives that addresses a critical environmental challenge. Products/Services must be available in 2023.

An independent panel of sustainability experts will judge submissions and select winners in each category for small, medium, and large businesses and non-profit organizations.

Winners of the NAB Show Excellence in Sustainability Awards will be recognized during a Main Stage ceremony at NAB Show on April 16, 2023 in Las Vegas.

The program, announced in December, is supported by Amazon Web Services (AWS), a leading cloud provider and a leader in the media technology sector.

“We are honored to support this award and the important work our industry is doing to become more sustainable,” said Marc Aldrich, general manager of Media & Entertainment at AWS. “The media and entertainment community is continuously finding new ways to reduce our carbon footprint, from cutting back on the number of production vans for broadcasts, to flights needed, to energy output from facilities. AWS is proud to do our part in supporting these efforts through our customers and partners by running our business in an environmentally friendly way.”

The Excellence in Sustainability Awards are managed by Barbara Lange, CEO of Kibo121, a consultancy firm that guides media technology organizations on their path to sustainability.

For more information and to submit a nomination, click here.

Media & Entertainment has a big environmental impact — think carbon emissions, waste and energy use. The video entertainment industry’s carbon footprint has surpassed even that of the airline industry, prompting technology developers and other companies to step up with innovative approaches and practices. Explore handpicked articles from NAB Amplify to discover why sustainability is the number one priority for M&E, along with the latest trends in creating a greener future:

When it comes to internet use, companies, consumers and standards organizations are considering new sustainability practices.

January 31, 2023

Posted

January 31, 2023

CES 2023: Controlling the Connected Home and Media Delivery/Distribution

TL;DR

Smart TVs now represent the most important point of entertainment aggregation, control, and data collection inthe connected home, according to Parks Associates.

Eighty-seven percent of US internet households subscribe to at least one OTT video service. More than half of US broadbandhouseholds now combine one of Netflix, Amazon Prime or Disney+ services with at least one other subscription OTT service to form theironline video service portfolio.

Increases in connected deviceownership, increased streaming video, and a largeremote workforce have further strengthened theimportance of home internet.

Smart TVs now represent the most important point of entertainment aggregation, control, and data collection in the connected home, according to a new report from Parks Associates, “2023 Top Insights – Smart Home,” based on findings from the Consumer Electronics Show.

The research analysts report that annual home service spending is $340 billion across home phone, internet, mobile, security and video services, amid continued growth of value-added services and connected devices in the home.

Consumers now place more value on their home’s internet service than previously. Increases in connected device ownership, increased streaming video, and a large remote workforce have further strengthened the importance of home internet.

Parks reports that consumers are seeking new bundles and services incorporating multiple service offerings, including home internet, pay-TV, landlines, mobile phones, and home security. The rise of these bundles, including broadband value-added services, has more than offset the decline in traditional bundles, it finds.

Such bundling and aggregation offer the traditional TV broadcaster “a path forward to reimagine video offerings in a multi-channel, multi-platform world,” the analyst says.

Data about consumer viewing via connected TVs allow providers to offer an improved experience with more relevant and personalized experiences for the viewer. Meanwhile, advertising partners can execute targeted marketing campaigns based on specific interests and behaviors. Parks cites new technologies promising to bring the “shoppable ad” vision to reality on TV through T-commerce experiences.

Content remains king — that is, the most significant factor influencing consumers’ viewing decisions regarding retention, engagement, and customer acquisition, per Parks’ report. Of this, live content has become a key component of many OTT service offerings and a staple of the consumer video portfolio, with good reason.

Sports programming, the biggest and most valuable component of live TV, is migrating from traditional broadcast television to internet streaming channels. Parks thinks that this transition makes it challenging for sports fans to locate content but that this creates opportunities for providers if they can attract fans with a bundled experience.

Internet service providers, meanwhile, are “modifying their relationships with pay-TV, treating the service as a value-add to home internet, and transitioning away from legacy cable head ends to cloud-based infrastructure and streaming TV services.” The goal is to reduce operational costs and widen service appeal, says Parks.

The analyst also notes that piracy is a real problem, potentially costing more than $67 billion dollars worldwide. It expects streaming services to experiment with new ways to protect content and to explore business models that can help recoup lost revenue from password sharing.

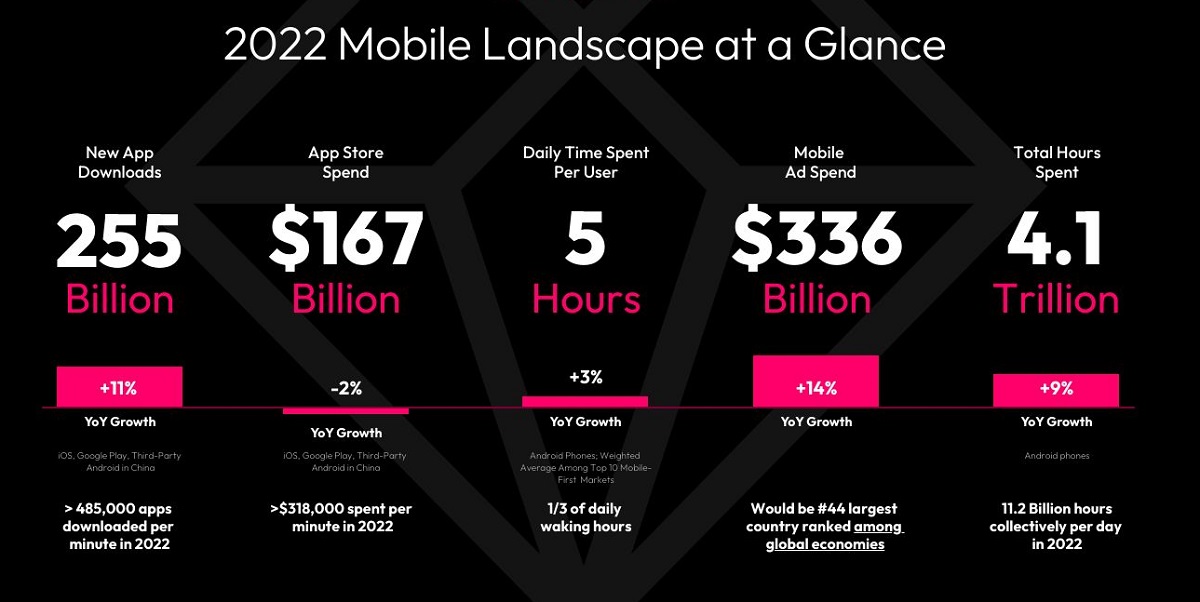

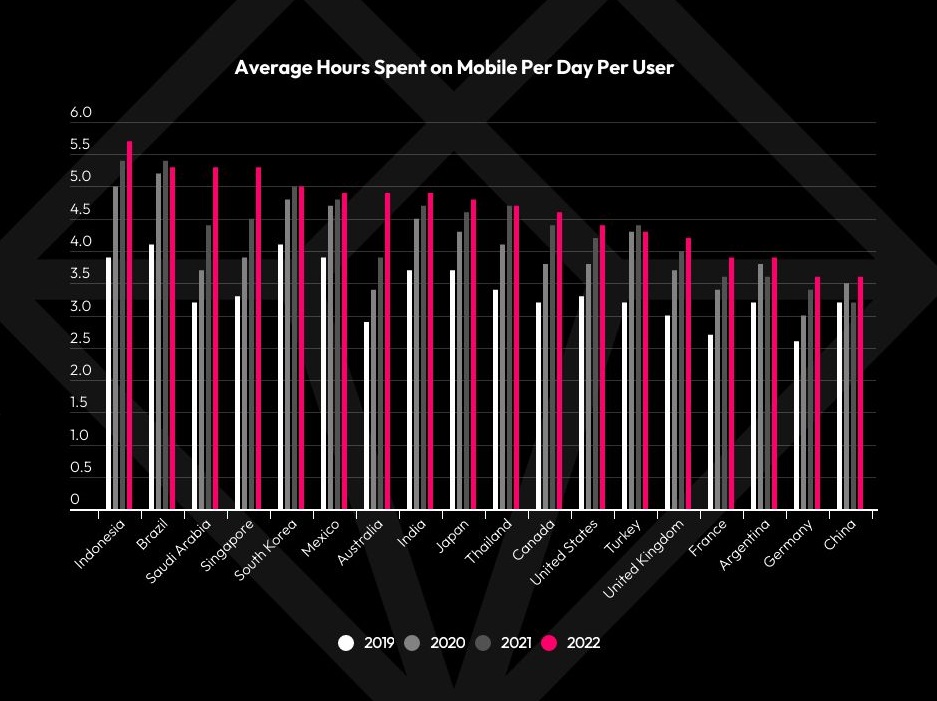

We’re spending up to five hours on our mobile phones every day, with exclusive sports content serving as a crucial on-ramp for new users, according to mobile data analytics provider Data.ai.

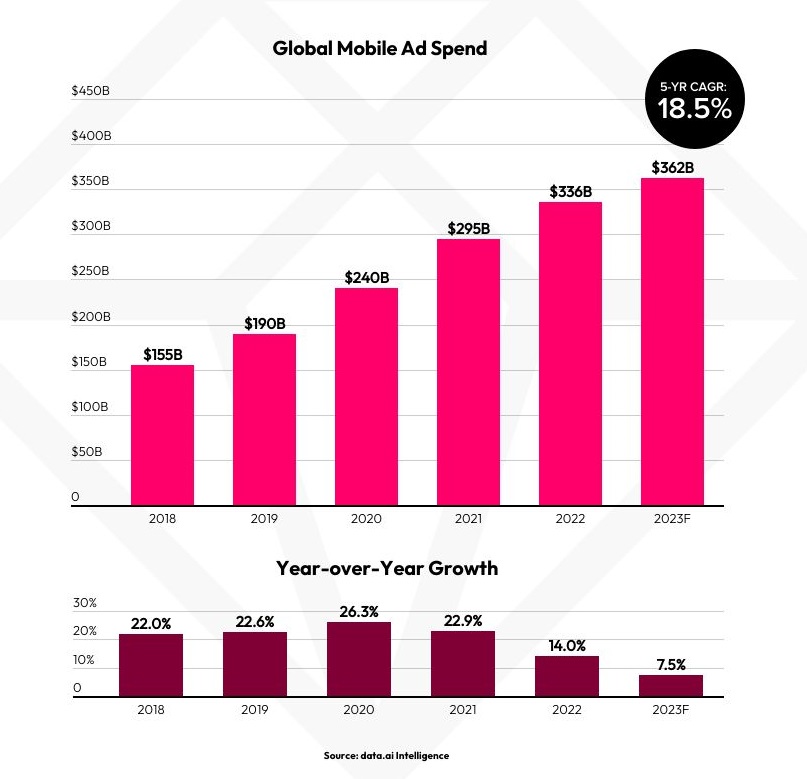

Its “State of Mobile 2023” report further explores a boom in downloads that saw mobile services downloaded a record 255 billion times globally last year. As a result, mobile ad spend is on track to hit $362 billion in 2023, after surpassing $336 in 2022, despite tightening marketing budgets.

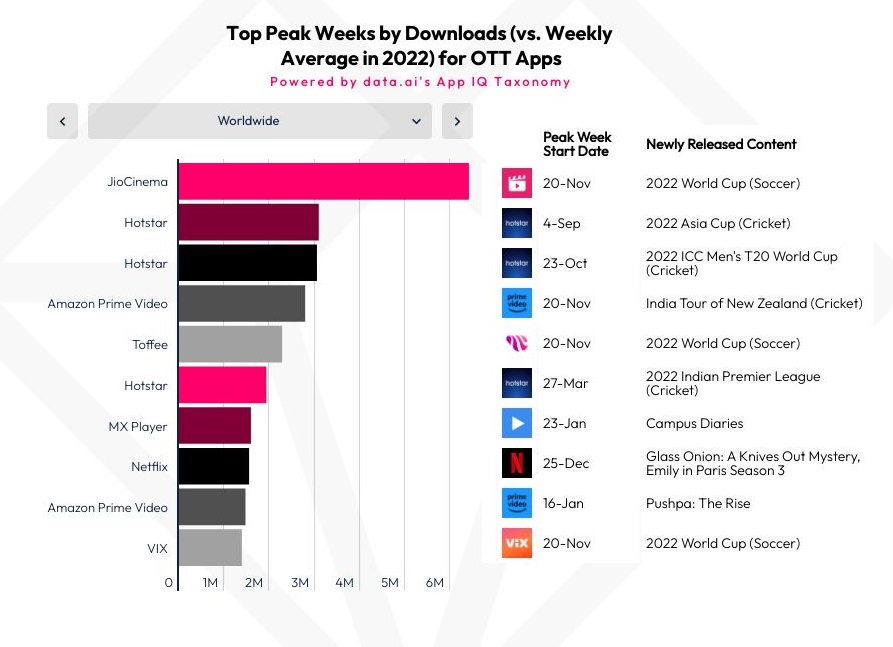

Adding coverage of major sporting events can be a “highly effective-albeit expensive-way” to add new users to popular streaming services, is one is one takeaway.

Globally, streaming of the World Cup matches and top cricket tournaments in India drove the biggest download spikes.

In the US, the World Cup also drove large adoption spikes for Peacock TV and fubo TV, while streaming deals with the NFL helped Peacock TV, Paramount Network and Amazon Prime Video.

FOX Sports and Canada’s TSN GO also saw “huge increases” in adoption as a result of their FIFA World Cup coverage.

DAZN and ESPN are the “clear standouts” in terms of consumer spending in the sports app category, earning more in 2022 than the rest of the top 10 sports apps combined. Nearly all of ESPN’s revenue comes from the US, while DAZN has managed to monetize across more markets by casting a wide net in terms of its sports coverage in different markets. Some of DAZN’s content includes Serie A in Italy (where frequent blackouts don’t appear to have dented its popularity) and Nippon Professional Baseball in Japan, as well as pay-per-view boxing.

Time spent per day has reached five hours in the top mobile-first markets. Cr: Data.ai

Time spent per day has reached five hours in the top mobile-first markets. Cr: Data.ai

Despite tightening marketing budgets, mobile ad spend is on track to hit $362 billion in 2023 after surpassing $336 in 2022. Cr: Data.ai

Globally, streaming of the World Cup matches and top cricket tournaments in India drove the biggest download spikes. Cr: Data.ai

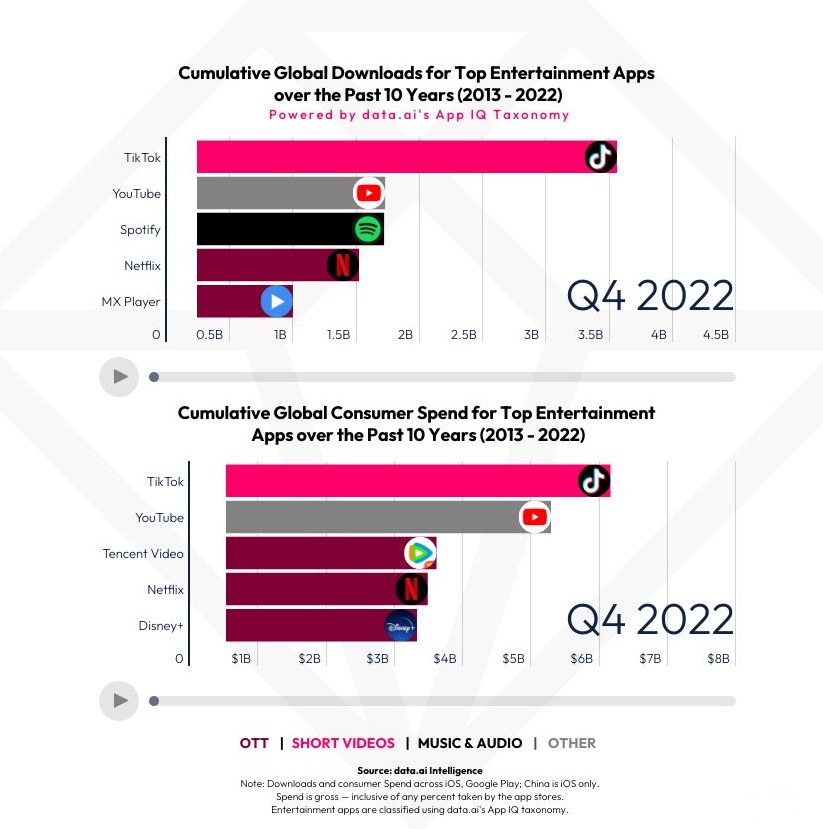

Led by TikTok, shortform video apps dominated consumer attention in 2022. Cr: Data.ai

Sports betting apps downloads peak at the start of the NFL season each year and the Super Bowl. The report found that sports betting installs reached 4.3 million at the start of the 2022-2023 NFL season, up 8% year-over-year and more than four times the total from September through October 2018. FanDuel emerged as the market leader in 2022, with BetMGM, DraftKings, and William Hill vying for the number two spot.

Data.ai observes that sports betting apps over-index for a male audience in the 25-44 age range, a similar demographic to those likely to use financial apps, for example, for cryptocurrency trading.

Non-sports content that created the biggest download spikes included Euphoria (HBO Max), Halloween Ends (Peacock TV) and House of the Dragon (HBO Max).

The United States market may be saturated by OTT providers but there’s still room for growth in Europe and Asia. That said, many European markets became more concentrated between 2020 and 2022, largely explained by the massive launch by Disney+ in the region. The report finds that OTT (over-the-top) apps such as Netflix and Disney+ grew 12% year-over-year to $7.2 billion.

“Look for other OTT providers to attempt to emulate Disney+’s successful global expansion,” is Data.ai’s note.

Spending on other apps (non-gaming) increased by 6% year-over-year to $58 billion, largely driven by subscriptions and purchases in OTT, dating, and short videos. Downloads increased 13% year-over-year to 165 billion.

Shortform video apps, led by TikTok, dominated consumer attention in 2022. Users of these apps streamed a whopping 3.1 billion hours of user-generated content daily, up 22% year-over-year, and spent $5.6 billion, up 55% year-over-year, fueling the creator economy.

“TikTok’s recent success was well beyond that of other Entertainment apps,” the report finds. “Over the past 10 years TikTok has more than twice as many downloads as the next closest app, YouTube.”

Other findings in the report: Time spent per day has reached five hours in the top mobile-first markets.

Downloads of mobile apps grew to 255 billion (+11% YoY), and hours spent peaked at 4.1 trillion (+9% YoY). Meanwhile, consumer spending across all app stores, cooled to $167 billion (-2% YoY) for first time ever due to decline in gaming spend, which was previously bolstered by pandemic conditions. However, non-gaming mobile services and subscriptions reached record spend.

“For the first time, macroeconomic factors are dampening growth in mobile spend,” says Data.ai CEO Theodore Krantz. “Consumer spend is tightening while demand for mobile is the gold standard. In 2023, mobile will be the primary battleground for unprecedented consumer touch, engagement and loyalty.”

6G may already be on the horizon, but there’s still a lot to understand about the benefits — and limitations — of 5G, which is rolling out across the US but has yet to reach peak saturation. Dive into these selections from the NAB Amplify archives to learn what, exactly, 5G is, how it differs from 4G, and — most importantly — how 5G will bolster the Media & Entertainment industry on the road ahead:

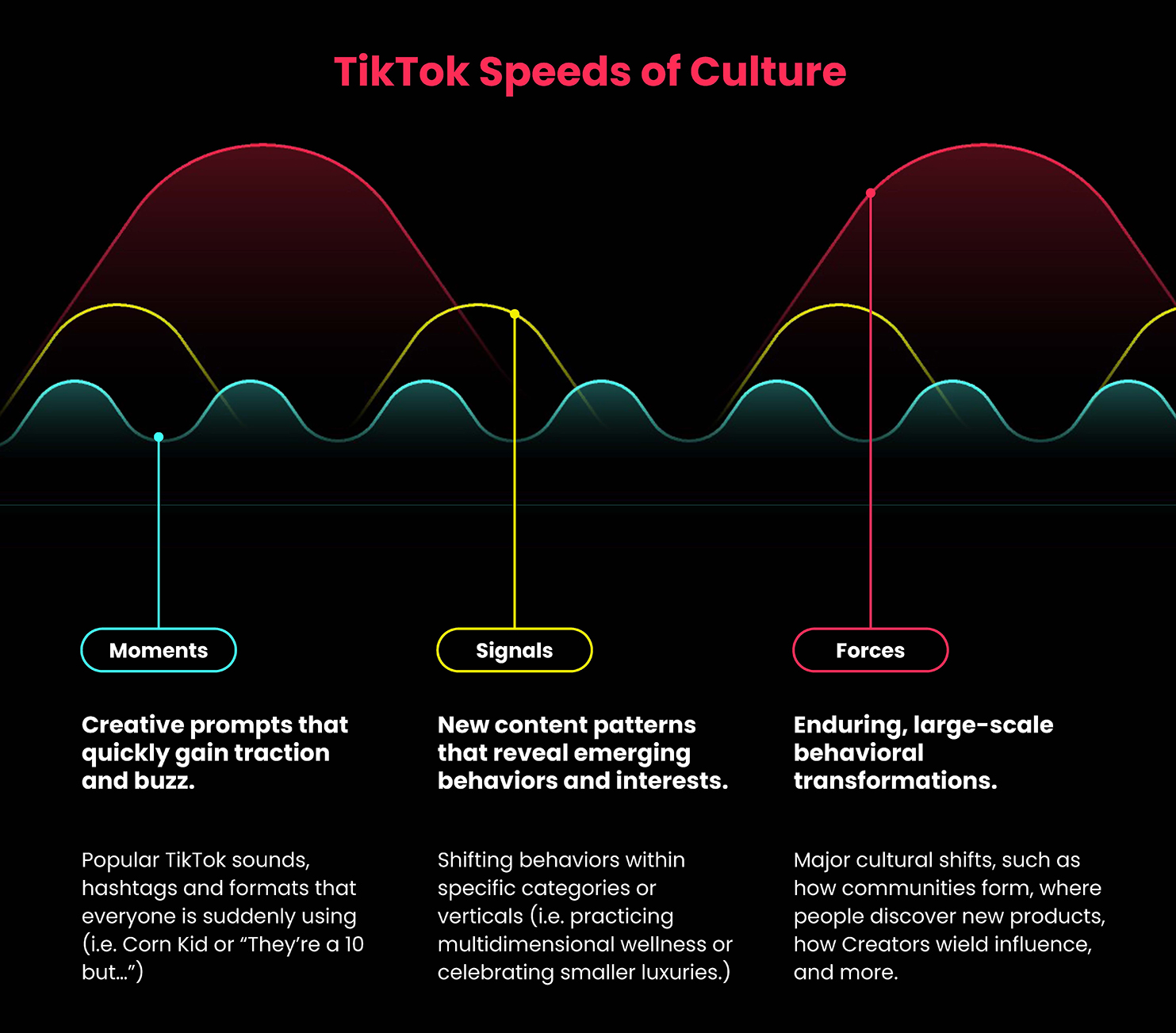

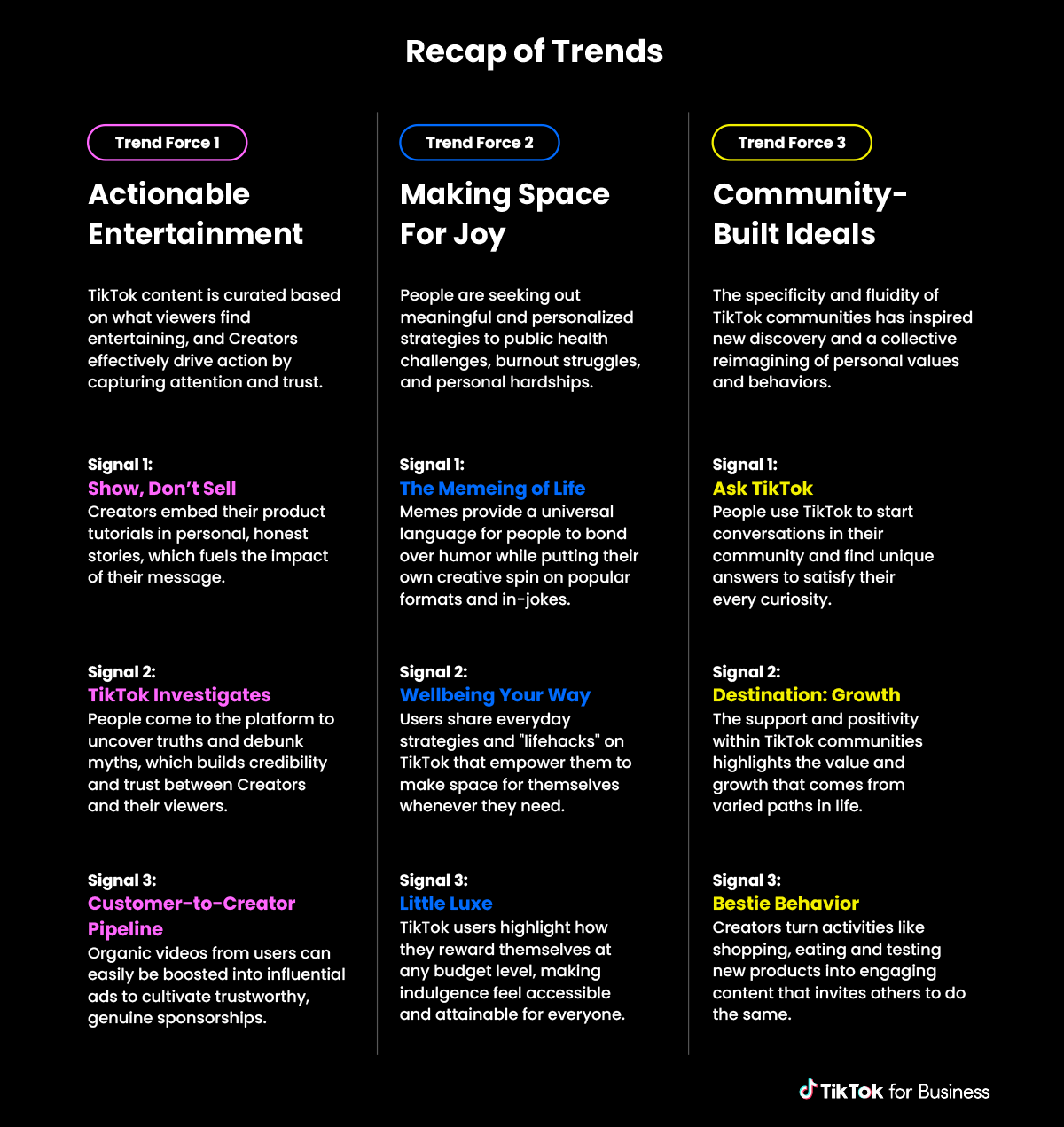

TikTok provides key messages for brands wanting to engage with the billions of users on the shortform video platform in a new report.

TikTok claims it fosters endless opportunities to spread joy; among TikTok users who took an action off-platform as a result of TikTok content, 90% said the platform makes them happy and never gets boring.

TikTok’s big prediction? In 2023, TikTok-first entertainment will inspire people to test out new products and ways of thinking and behaving.

If you’re looking for clues for how TikTok is shaping global culture and politics you won’t find them in its own report, a glossily produced brochure enticing brands to work with creators and influence users of its platform.

Much of what the shortform video giant says in its “What’s Next: 2023 Trend Report” could have been plucked from similar marketing messages produced over the years for YouTube. And maybe that’s the point. Move over Google, there’s a new place for investors to roost.

“Essentially, [TikTok] is a space where people can find new ideas on how to explore their passions and live their lives,” we learn. “And as people seek out ways to break the status quo, they’ll look to peers and role models who have the confidence to live life the way they want to.”

Sofia Hernandez, global head of business marketing for TikTok, is quoted, also saying not a lot: “2022 was the year people realized they didn’t have to live their lives as they always have done — with different points of view and ideas transcending cultures on TikTok. Next year we’re going to see more of this — as our communities get more confident and inspire positive change together.”

Against the backdrop of the increasing cost of living, apparently what people want is to have fun. They want humor, they want to feel happy and healthy. They want to feel part of a community and, above all, they want to be entertained.

It’s not rocket science, but TikTok says its platform is the best place for advertisers to reach audiences and that to do so they should work with creators.

Four out of five users say TikTok is very or extremely entertaining, per the report. “This means that when advertising messaging is delivered like an ad, but loved like entertainment, brands can see incredible business results,” TikTok explains. “For brands, the most effective messages on TikTok are uplifting, funny and personalized, or entertaining their audiences. Brands can build on this entertainment value by using editing techniques like syncing sounds to transitions or adding text overlays — which are effective at keeping viewers’ attention.”

The report differentiates content on TikTok from other platforms, where it is “personalized” based on broad identity categories or simple browsing histories. In fact, TikTok is 1.8 times more likely to introduce people to new topics they didn’t know they liked compared to traditional social platforms, per the report. We learn that content is curated on the platform based on what viewers find entertaining, so it captures their attention and trust.

“The trust is a result of who’s making the content. When a viewer sees a video from a creator they can relate to or from an expert they’re more likely to take the information to heart.”

Among people who took an “off-platform” action as a result of a TikTok video, 92% say they felt a positive emotion that ultimately resulted in an off-platform action. Meanwhile, 72% say they obtained reviews from creators they trust on TikTok, more than any other platform.

TikTok’s big prediction? In 2023, TikTok-first entertainment will inspire people to test out new products and new ways of thinking and behaving.

We are also led to believe that “people come to the platform to uncover truths and debunk myths, which builds credibility and trust between Creators and their viewers,” which may be news to those concerned about TikTok’s potential for political bias or cultural sway, though in truth these levels of mistrust have yet to reach Twitter and Facebook-style proportions.

Have longer video footage at your disposal? TikTok advises you to let artificial intelligence automatically cut video clips and save yourself time on editing, “so you can focus on the fun stuff.”

Joy, we also understand from the report, is a growing factor in people’s purchasing decisions worldwide, so it should be a key element of marketing strategies in 2023.

“Create TikTok content that helps people carve out joy for themselves, or even provides it through humor, relaxation and relatable points of view. Different creative approaches and tools can help you incorporate these elements into the videos you make for the platform.

In 2023, “messaging on TikTok — and beyond — should speak to this desire for levity and encourage people to make more room for themselves.”

Technology and societal trends are changing the internet. Concerns over data privacy, misinformation and content moderation are happening in tandem with excitement about Web3 and blockchain possibilities. Learn more about the tech and trends driving humanity’s digital future with these hand-curated articles from the NAB Amplify archives:

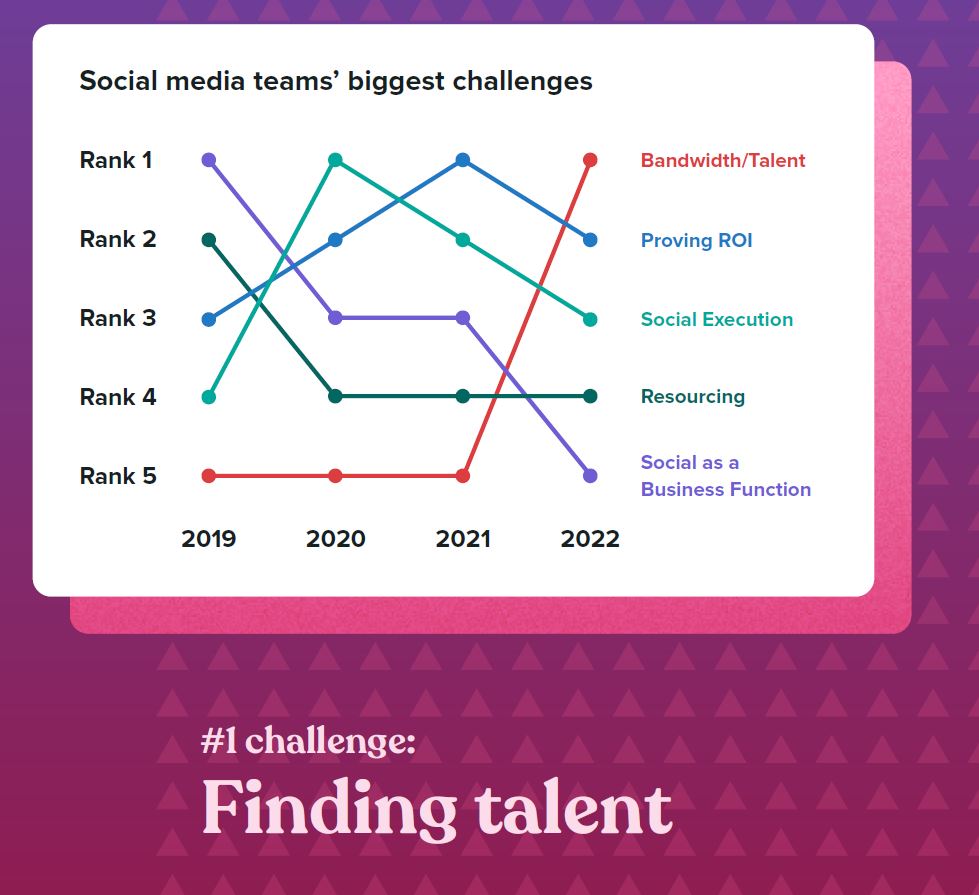

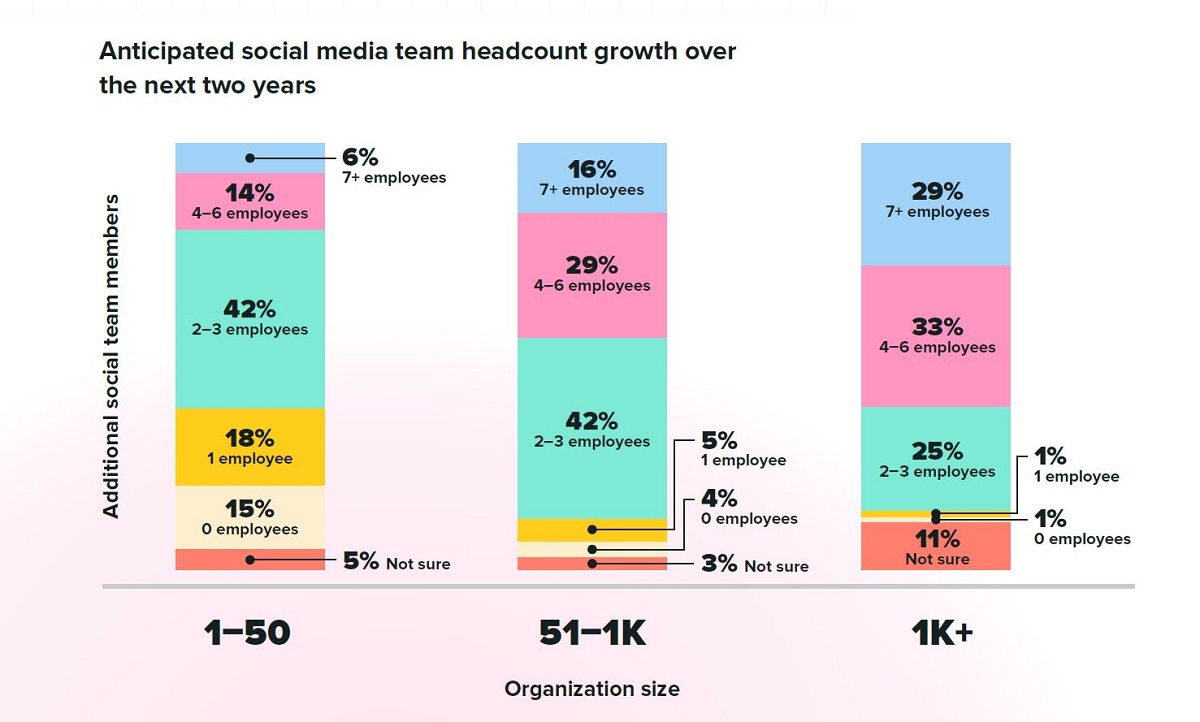

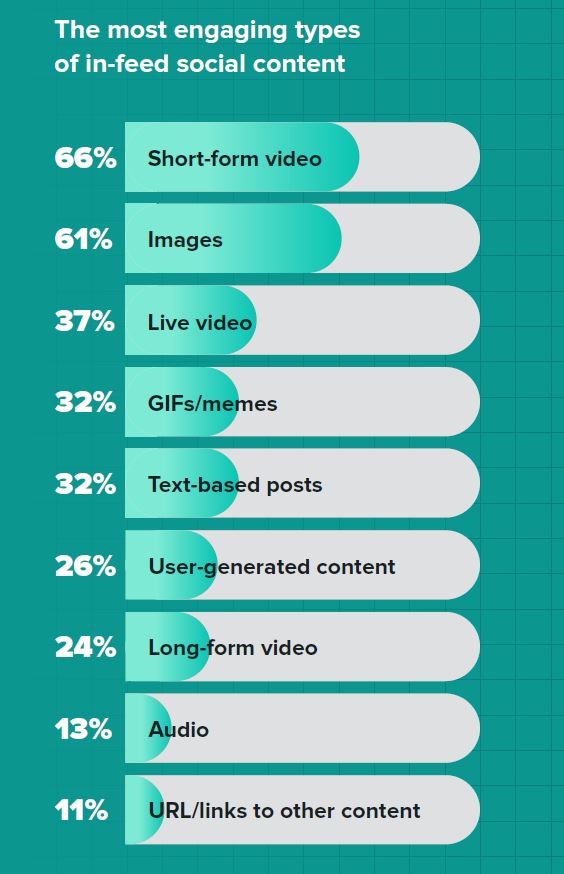

The value of social media across functions is clearer than ever, but finding experienced talent is the top challenge businesses face.

January 25, 2023

Posted

January 20, 2023

What’s Next for Streaming? (It’s All About the ARPU, Baby)

Penn Badgley in season four of “You,” courtesy of Netflix

TL;DR

After a tough 2022, premium subscription streamers are in the middle of reorienting their business model from content commissions to distribution.

The days of multi-million dollar paychecks for show creators seem to be over as content must now wash its face in metrics for ARPU (Average Revenue Per Unit).

A greater focus on franchise content — sequels and spinoffs — and linear TV-like schedule releases can help streamers counter high churn rates.

Netflix’s decision to cancel high profile drama 1899 after just one season came as a shock to fans and a reality check to content producers that streaming shows will be cut to a different cloth from now on.

Just as consumers don’t have an endless budget to subscribe to streaming services, so content providers are no longer willing to open the checkbook if the numbers don’t add up.

And those numbers have changed along with the way success is measured.

“The enthusiasm for streaming among consumers is still there, but I think the assumption that all these platforms are going to continue to grow and add subscribers every quarter is gone,” Hub Entertainment Research founder Jon Giegengack told Lucas Manfredi at The Wrap. “I’m not entirely sure why people thought it would go on forever, but we’ve reached the point where that’s not guaranteed.”

Netflix’s first subscriber loss in over a decade last April caused a shock wave that sent streamers back to the drawing board. Revised strategies include a shift of focus from pure subscriber growth to profitability and average revenue per user.

“Ultimately, companies need to generate cash so that they can pay the bills and not go bankrupt,” David Offenberg, an associate professor of finance at Loyola Marymount University, told The Wrap. “I think the focus will be on ARPU [Average Revenue Per Unit] for the rest of eternity at this point. We’re done with focusing on subscribers. And if you’re not at scale yet, your chances of getting there are pretty slim.”

Netflix was the first to alter course and has succeeded in leading the competition on ARPU. Figures in the article show Netflix has an ARPU of $16.37 in the US and Canada, followed by Hulu’s ARPU of $12.23 and Warner Bros. Discovery of $10.66. Disney+ has lagged behind its rivals with a domestic ARPU of just $6.10.

Another universal tactic is to adopt different pricing tiers with many streamers introducing a free or lower cost ad-supported option.

Additionally, many streamers are increasingly leveraging bundled services. The average household has 12.5 different entertainment sources that they consume, according to a Hub Entertainment survey of TV consumers. These sources include streaming TV, social media, gaming, music, sports, podcasts, audiobooks and reading.

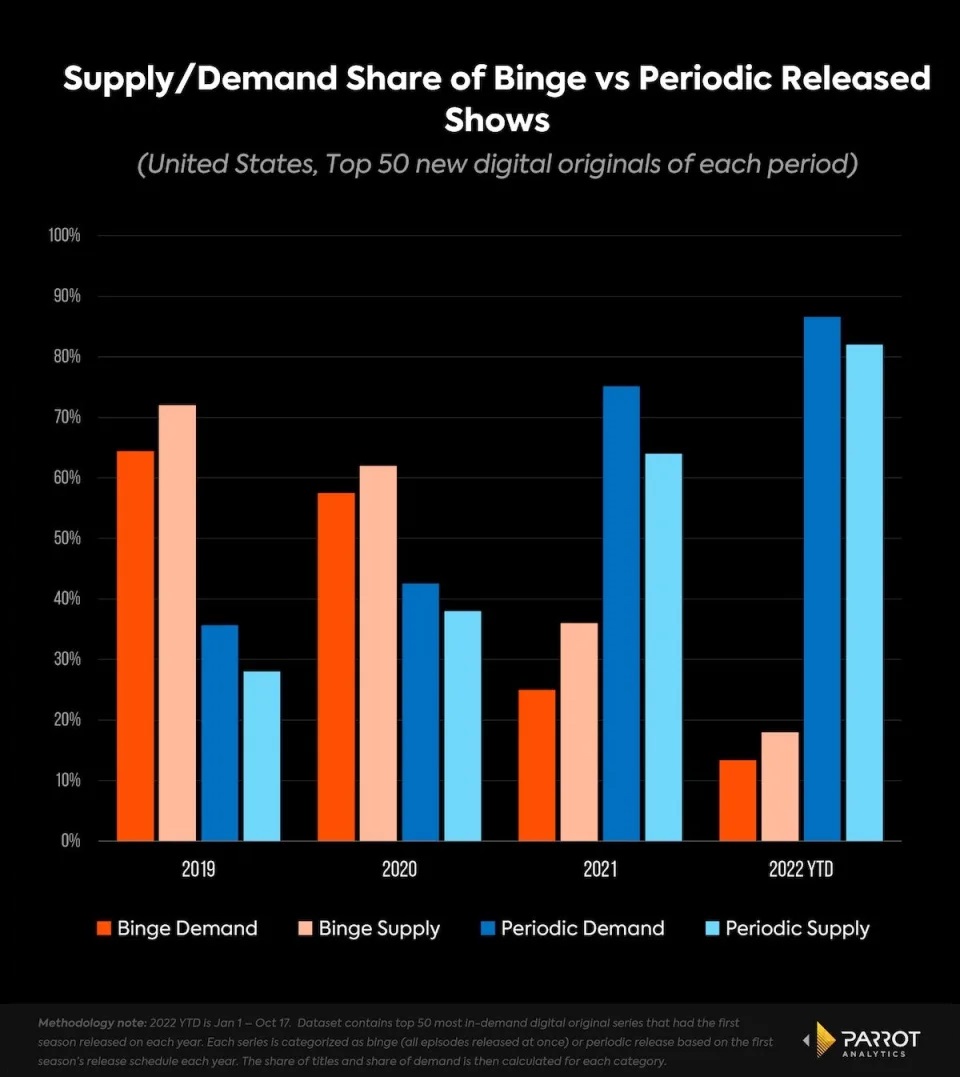

Cr: Parrot Analytics

Cr: Parrot Analytics

Companies that are able to super-aggregate these services into bundles will have an edge, Manfredi maintains. Notable examples of super bundles include Amazon Prime, which offers benefits like access to Prime Video content and free delivery on Amazon purchases, and Apple One, which includes AppleTV+, iCloud storage, Apple News, Apple Music, Apple Arcade and AppleFitness+.

The cancellation of major shows like 1899 is far from unique and speaks to the fact that streamers can no longer afford to have an endless library of shows and movies

“As profitability and ARPU take center stage moving forward, streamers have learned that they will need to be more mindful about their content spend and what that investment is going towards,” says Manfredi.

1899 was an expensive show to produce and required an entirely new and unique virtual production volume to be built in Berlin. Likewise, the multimillion-dollar deals that have been awarded to show creators like Ryan Murphy, Shonda Rhimes and Rian Johnson, “are a thing of the past,” according to Morning Consult entertainment and media analyst Kevin Tran.

“Streamers need to make better use of the intellectual property they already own while also keeping in mind moving forward that sheer quantity of content is now far from a compelling differentiation factor,” he says.

On the flip side, Tran warns that pulling content could make showrunners and actors “more hesitant to work with a company that they view as too eager to axe pricey or declining shows from their streaming platforms” and potentially anger fans of those shows.

Manfredi also thinks that the days of binge viewing are largely over. It makes more sense for streamers to drop episodes, especially of its most popular content, over a period of months to eke out subscriber engagement. Netflix’s two-part release of Stranger Things S4 last year was a case in point.

“If people can binge watch a whole show and then drop their subscription until the next season comes out, that’s a pretty tough calculation if you have to come up with a brand new, super expensive show to reengage them every time,” Giegengack said. “If you parse those shows out and the episodes come out once a week, or maybe starting with two like they do on Paramount+ to get people hooked, and then parse them out further apart after that, each piece of content that you’re investing with can keep people engaged for a longer period of time.”

Churn is still a huge issue for all streamers. In the third quarter of 2022, cancellations across Netflix, Hulu, AppleTV+, Disney+, Discovery+, HBO Max, Paramount+, Peacock, Showtime and Starz grew to 32 million, according to Antenna. The figure represents a “significant expansion” from 28 million cancellations in the previous quarter and 25.2 million cancellations in the same quarter a year ago.

In a bid to counter churn, Manfredi detects a new urgency around commissioning franchises. One poll suggests 75% of people are likely to cycle subscriptions in the next six months with the main stated reason being that there was only one title on a given streamer that they were interested in viewing.

“A reliable way to retain subscribers is to keep them connected to things that they know and love,” Lionsgate Television Group vice chairman Sandra Stern told The Wrap. “I think for streamers particularly that is a really major objective.”

Disney+ has mastered this strategy with regular output of new Marvel Studios shows such as Loki and She-Hulk: Attorney at Law and new Star Wars series like Andor. Netflix has scored success with Wednesday and Paramount+ continues to earn mileage from Yellowstone spinoffs. Look out for Peacock’s John Wick universe spinoff later this year.

“Andor” creator and showrunner Tony Gilroy and editor John Gilroy recount the complexities of bringing the Star Wars episodic to the screen.

January 17, 2023

Virtual Production Is Going Great, But… We Have Some Talent and Tech Challenges

TL;DR

Altman Solon’s 2022 Global Film & Video Production Report finds virtual production is on the rise, but the industry faces challenges over sourcing talent and harnessing the power of data.

Productions are shifting towards a data-driven approach to improve production forecasting and measure VP success.

Virtual production is still in its early days, with widespread adoption limited to specific projects where it’s easily applicable. However, there are emerging trends around how VP is used, the impact it has on projects, and criteria used for deciding when to use it.

Virtual production continues to gain traction across the film and TV industries, but the cost of using it remains high and talent with VP experience and training is limited, according to a new Altman Solon report.

Creatives are still be skeptical about incorporating the technologies — and the research finds there’s also a lack of sophisticated data analysis necessary to make the case for virtual production.

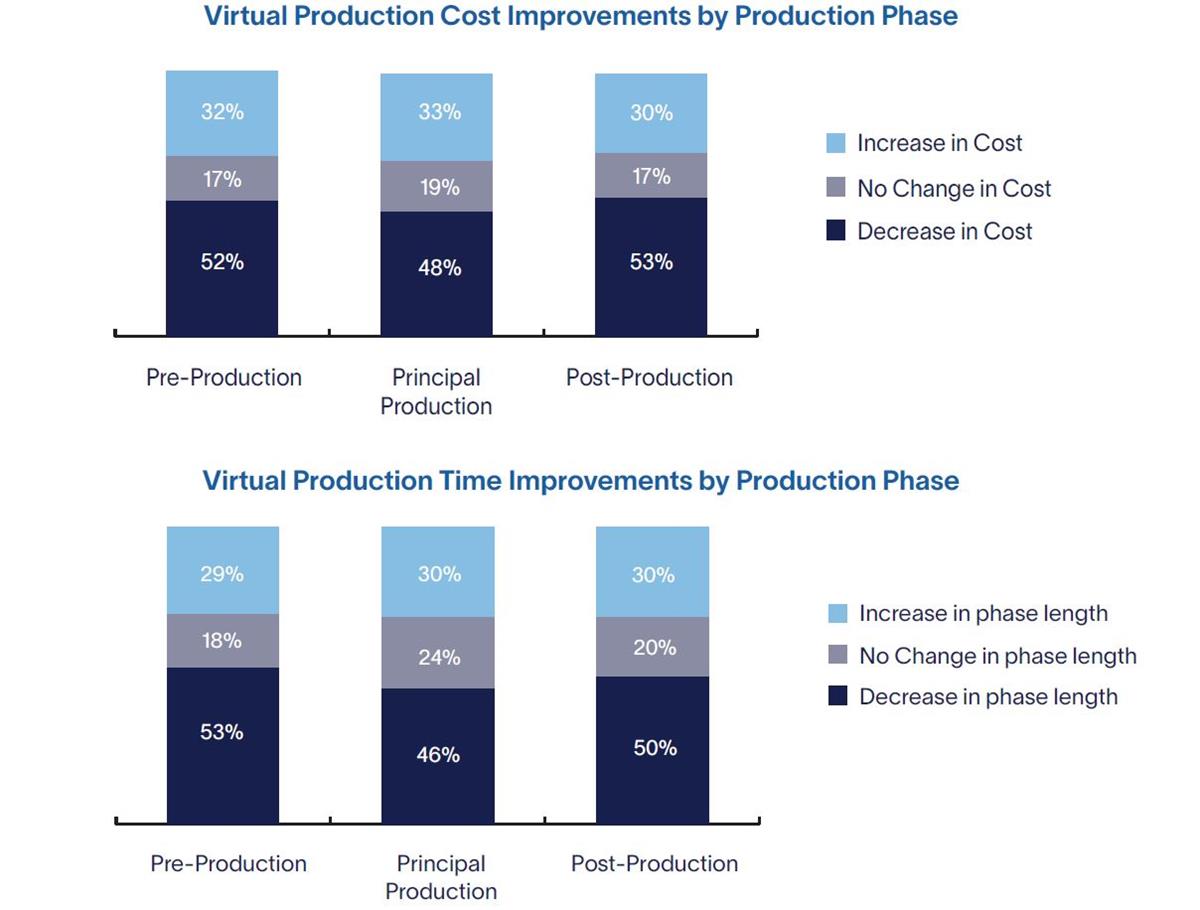

The consultancy’s 2022 Global Film & Video Production Report highlights VP as a growing trend in the industry, driven by the need for virtual and collaborative tools to lower production costs, improve timelines, and overcome the limitations of physical production sets.

It surveyed over 100 industry experts with more than three years of experience in virtual production and found that motion capture was the most popular VP technology, with 50% reporting they or their team have used it over the past 12 months.

The second most popular tool, cloud-based editing (48%), has gained favor among production staff because it enables remote collaboration. Three-quarters of respondents identified virtual scouting as a tool that saves money and shortens timelines. Newer technologies like in-camera VFX (42%) and virtual scouting (39%) have lower adoption rates.

Despite the popularity and effectiveness of certain tools, widespread adoption is limited to specific projects where VP is easily applicable — often projects that require many filming locations or sci-fi/fantasy productions.

For small productions, the survey found that travel budget savings can make a virtual production project more economically viable.

“While medium and small stages exist, producers of mid-tier content often lack the readiness and experience to shoot on a Tier 2 or medium stage, and one-off shoots don’t reap the benefits of shooting multiple episodes or seasons on a stage,” the report says.

There are some 84 virtual production stages in the US and another 40 in the UK, however this number also includes smaller “xR stages” used mainly for music videos or commercials, not shows or films.

The report suggests that smaller production studios with limited resources won’t be able to afford a larger stage and may opt for traditional shooting methods or green screens, rendering LED volumes less relevant for the mid- to low-budget markets.

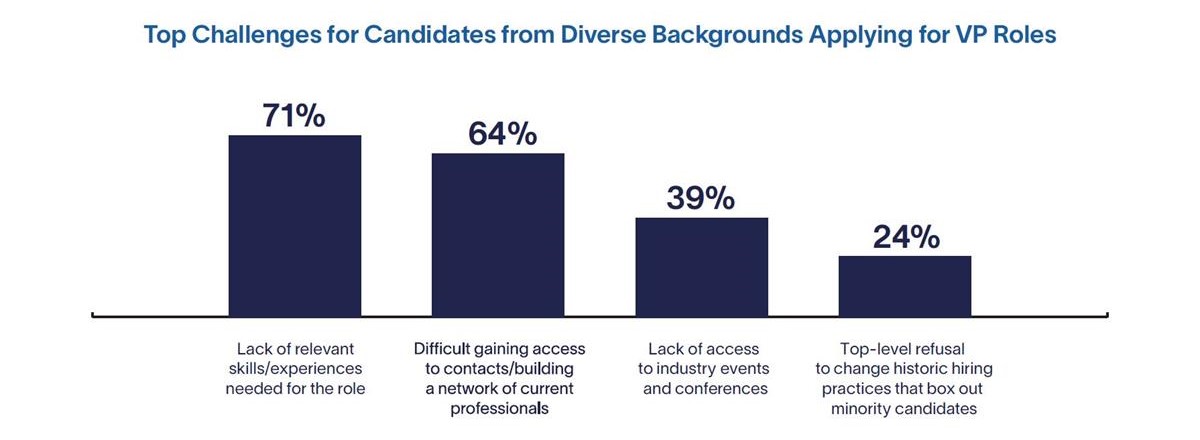

Because virtual production is still an emerging technology, there is a shortage of talent with “hands-on” experience in the industry, creating staffing challenges for production studios. Additionally, the broader industry has historically lacked diversity in terms of race and gender, creating a talent funnel issue when trying to hire candidates of diverse backgrounds for VP-specific roles.

Instead, most respondents are now looking for candidates in adjacent industries like gaming, AR/VR, animation, automotive and transport, and architecture, among others, and through on-campus recruitment to find candidates with the necessary technical skills. Candidates from industries that use real-time gaming technology and are familiar with the workflows are desirable for VP roles.

“Virtual production is the future of global filmmaking but how and when it maximizes its potential will be determined by the industry’s ability to attract talent to this new field,” said Altman Solon director Derek Powell.

“It’s clear that the networking-heavy approach used in Hollywood for generations will not deliver the VP workforce needed now and in the future. The good news is that studios are employing new and creative recruiting techniques, including better outreach to candidates with diverse backgrounds.”

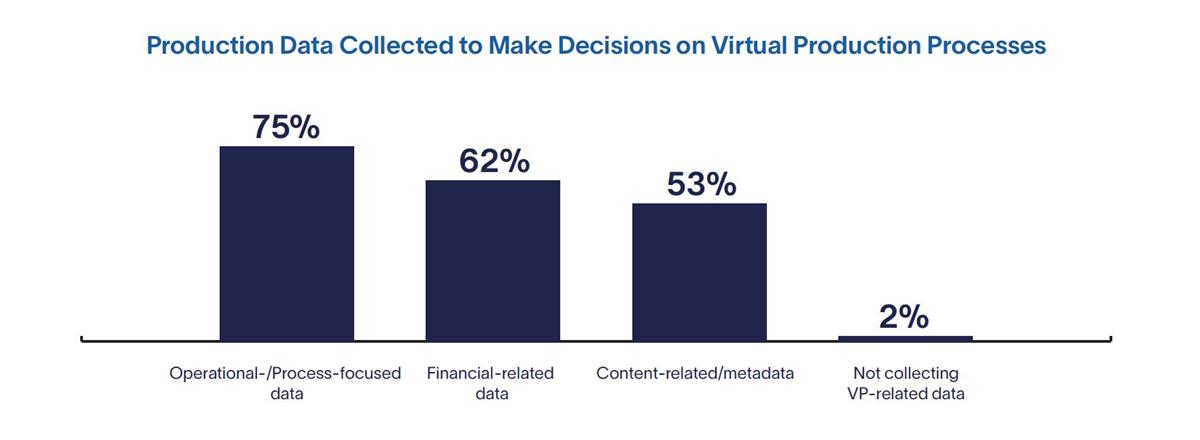

Virtual Production as Part of a Data-Driven Strategy

Because of virtual production, studios now have more access to data, opening the opportunity to gather data across the production process and run analytics to uncover insights for more informed decision-making.

That’s a change, since historically, production studios didn’t collect technical production data. VP can be used to collect and leverage production data that identifies possible efficiencies (for example, using lens metadata and lighting parameters defined in the gaming engine to make corrections in post-production). According to the report, there is potential for productions to use VP data to automate processes in post-production that in the past were done with creative teams, thus saving time and money.

However, while VP tools enable great collection of data versus traditional production methods, production teams hit roadblocks when collecting it. According to the survey, the top three limitations to collecting data are “lack of business intelligence strategy” (62%), “lack of business intelligence impact” (49%), and “lack of training and execution” (45%).

“All these inhibitors are characteristic of organizations with immature business intelligence and data strategies,” finds the consultancy — which would no doubt offer its services to assist in this regard. “This indicates that while production teams have the tools to gather and analyze data, they are still nascent in this area and slowly transitioning to be more data-driven.”

This matters most when budget forecasting, which was the top data-usage focus of VP executives surveyed. Altman Solon says: “In traditional productions, variables associated with set design, shooting, travel, and logistics can change greatly when a shooting location needs to change or if a scene needs to be reshot, which can include bringing talent and crews back to a location. For these reasons, using data to improve budget forecasting was the top-ranked selection in the survey.”

Other Issues Highlighted in the Report

Currently, there are no standard virtual production processes, and each production has its own unique process structure. Data security is also a concern for half the respondents, largely due to the use of cloud-based tools, which some users perceive as having weaker security controls than on-premises solutions. Similarly, just under 50% of respondents expressed concern over the potential for customizable workflow configurations since cloud-based tools have fewer customization capabilities.

Next, Listen to This

Epic Games’ Los Angeles Lab Director Connie Kennedy and American Cinematographer Virtual Production Editor Noah Kadner join us to talk about the confluence of practical and virtual production, and help shed some light on what virtual production actually is — and isn’t.

The use of LED walls and LED volumes — a major component of virtual production — can be traced directly back to the front- and rear-projection techniques common throughout much of the 20th century.

The creators of “1899” understand that virtual production requires designing the story, as well as the set, with rigor and detail.

January 9, 2023

Posted

January 9, 2023

How Diffusion Drives Generative AI

TL;DR

Diffusion models replaced GANs (generative adversarial networks) to drive the recent trend in generative AI tools.

Diffusion-based AI has also proved adept at composing music and video.

The tech has been around for a decade but it wasn’t until OpenAI developed CLIP (Contrastive Language-Image Pre-Training) that diffusion became practical in everyday applications.

Text-to-image AI exploded last year as technical advances greatly enhanced the fidelity of art that AI systems could create. At the heart of these systems is a technology called diffusion, which is already being used to auto-generate music and video.

So what is diffusion, exactly, and why is it such a massive leap over the previous state of the art? Kyle Wiggers has done the research at TechCrunch.

We learn that earlier forms of AI technology relied on generative adversarial networks, or GANs. These proved pretty good at creating the first deepfaking apps. For example, StyleGAN, an NVIDIA-developed system, can generate high-resolution head shots of fictional people by learning attributes like facial pose, freckles and hair.

In practice, though, GANs suffered from a number of shortcomings owing to their architecture, says Wiggers. The models were inherently unstable and also needed lots of data and compute power to run and train, which made them tough to scale.

Diffusion rode to the rescue. The tech has actually been around for a decade but it wasn’t until OpenAI developed CLIP (Contrastive Language-Image Pre-Training) that diffusion became practical in everyday applications.

CLIP classifies data — for example, images — to “score” each step of the diffusion process based on how likely it is to be classified under a given text prompt (e.g. “a sketch of a dog in a flowery lawn”).

Wiggers explains that, at the start, the data has a very low CLIP-given score, because it’s mostly noise. But as the diffusion system reconstructs data from the noise, it slowly comes closer to matching the prompt.

“A useful analogy is uncarved marble — like a master sculptor telling a novice where to carve, CLIP guides the diffusion system toward an image that gives a higher score.”

OpenAI introduced CLIP alongside the image-generating system DALL-E. Since then, it’s made its way into DALL-E’s successor, DALL-E 2, as well as open source alternatives like Stable Diffusion.

So what can CLIP-guided diffusion models do? They’re quite good at generating art — from photorealistic imagery to sketches, drawings and paintings in the style of practically any artist.

Researchers have also experimented with using guided diffusion models to compose new music. Harmonai, an organization with financial backing from Stability AI, the London-based startup behind Stable Diffusion, released a diffusion-based model that can output clips of music by training on hundreds of hours of existing songs. More recently, developers Seth Forsgren and Hayk Martiros created a hobby project dubbed Riffusion that uses a diffusion model cleverly trained on spectrograms — visual representations — of audio to generate tunes.

Even with AI-powered text-to-image tools like DALL-E 2, Midjourney and Craiyon still in their relative infancy, artificial intelligence and machine learning is already transforming the definition of art — including cinema — in ways no one could have ever predicted. Gain insights into AI’s potential impact on Media & Entertainment in NAB Amplify’s ongoing series of articles examining the latest trends and developments in AI art

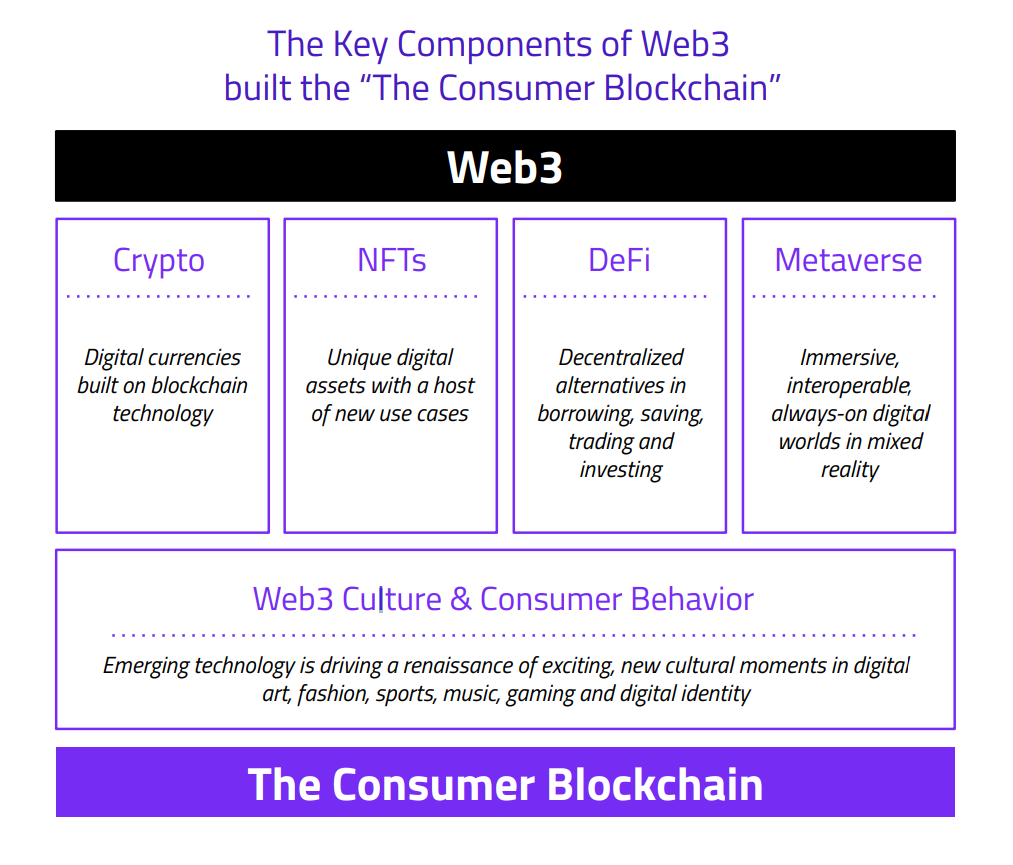

Crypto and NFTs have received negative publicity of late but the potential for Web3 to recode the rules of business engagement remains as potent as ever, according to consultancy Vayner3.

In its report it identifies what mattersmost to marketers and operators at large organizations. While acknowledging that macroeconomicforces and regulatory changes could play a major role in how 2023 unfolds, it remain convinced: Web3 is going increasinglymainstream in 2023.

Mobile device proliferation was a primary catalystfor Web2, with Web3 likely to follow a similarmass adoption curve.

Web3 and its constituent technologies like crypto currencies and NFTs have taken a knock this past year but boosters continue to promote its strengths, arguing that 2023 will be the year of mass adoption.

Vayner3, a Web3 consultancy, is one of them. While not dismissing the “bad actors” and “sobering lows” such as the recent collapse of FTX, Celsius, and Terra Luna, it largely puts Web3 woes down to negative press publicity.

On the other hand, basic knowledge of Web3 has gone mainstream helped by media attention. “The tenor of mainstream media continues to paint NFTs and crypto as a fringe movement rife with scams and scandals,” says Chris Liquin, SVP Strategy and one of the authors of a new report published by Vayner3. “Media sentiment and [falling] asset price are only the tip of the Web3 iceberg, and these narratives certainly broke through to mainstream consumer awareness in 2022.”

Liquin continues, “…but just under the surface, we see initial experimentation, enterprise investment, and technological developments that will continue to meaningfully advance Web3 culture, technology, and adoption.”

According to the consultancy we are past the “shiny new object” phase of gimmick and test, with major brands and big tech players all taking Web3 seriously.

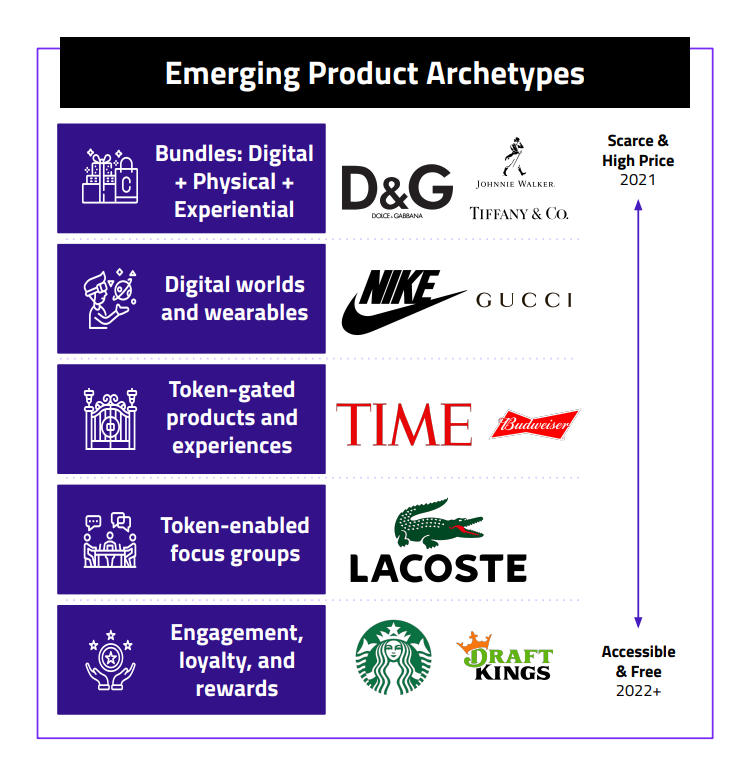

Next year, the “brands who onboard the masses” will offer clear Web3 products, pursue nuanced consumer targeting, and develop intentional go-to-market strategy.

“We expect product strategy to move from scarcity to scale in 2023 with a greater focus on new forms of engagement and consumer insights vs. consumer sales and revenue generation.”

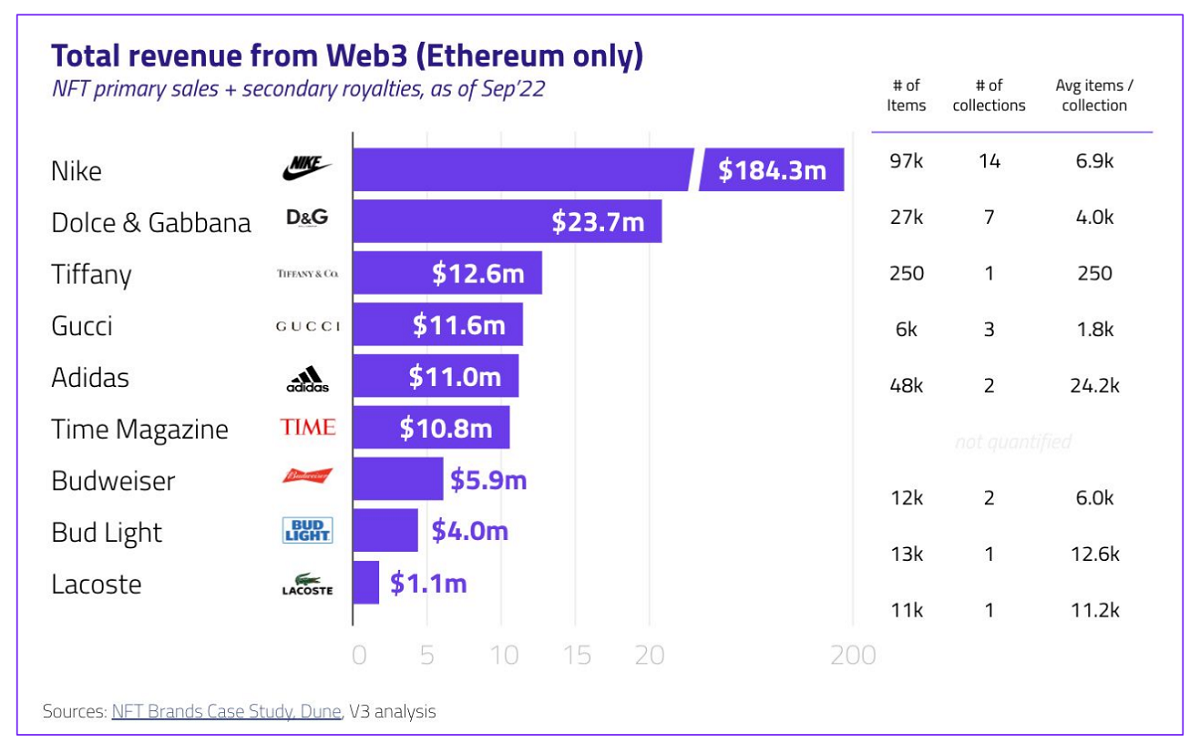

Cr: Vayner3

Cr: Vayner3

Cr: Vayner3

Cr: Vayner3

Cr: Vayner3

One tactic is to remove the mystifying jargon that clouds much Web3 speak. Choosing to talk of “digital collectibles” rather than NFTs, for example, is an increasingly common a simplification with new platform entrants like Reddit and Instagram using more “mainstream-friendly” terms as well.

Vayner3 expects winning brands to develop consumer strategies that incorporate a longer-term view of program design, product releases and community-building.

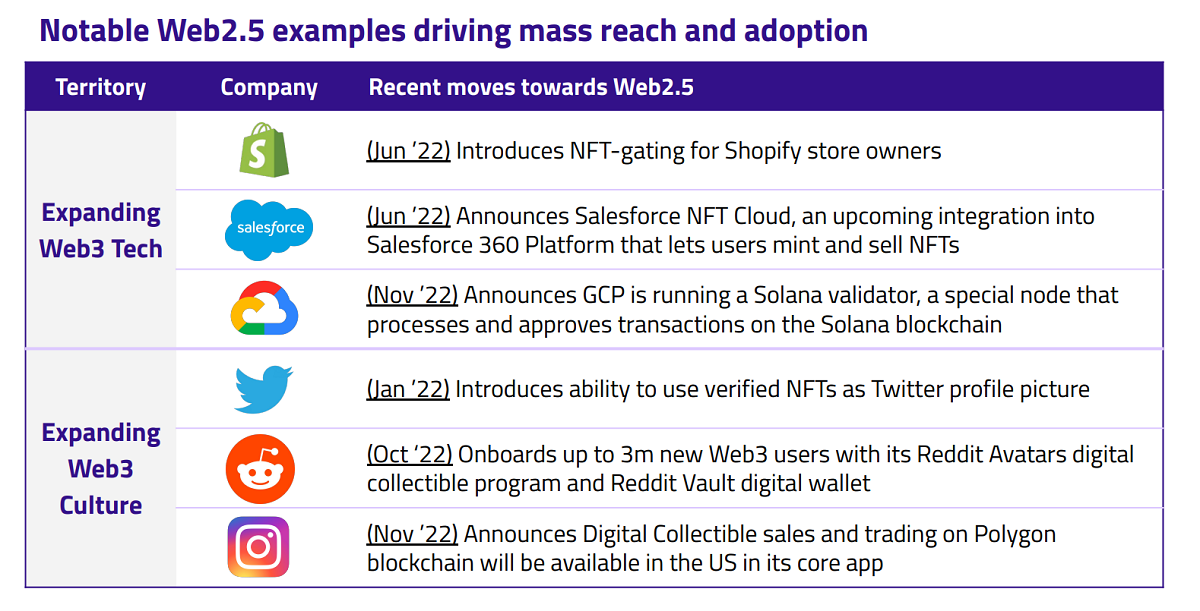

Another reason why Web3 is only going to get stronger is the role of Big Tech. Virtually all are integrating blockchain-based tokens into their core product offerings, which is resulting in a hybrid between Web2 and Web3 the consultancy calls Web2.5.

The report also notes that Meta, Shopify, Google, Instagram, Amazon, Microsoft and Reddit are experimenting with Web3: These massive Web2 organizations typically “experiment” with multi-million (if not multi-billion)-dollar amounts of attention, investment and scale.

For example, in its latest pilot program, Instagram recently announced NFT creation, sales and trading will be available to its 160 million US users.

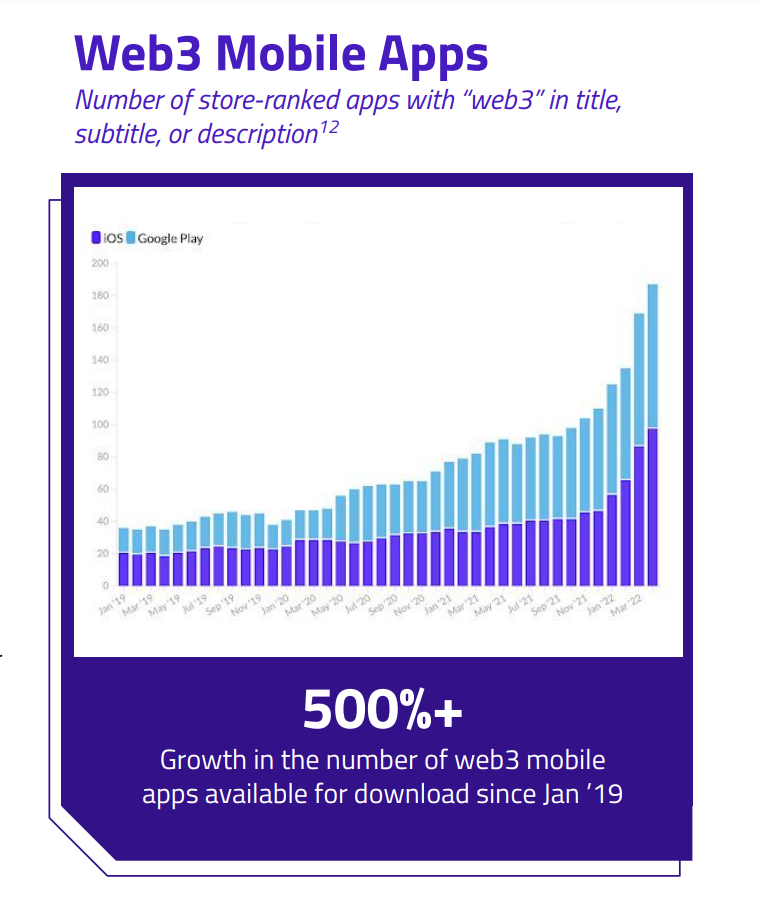

Mobile device proliferation was a primary catalyst for Web2, and Vayner3 expects Web3 to follow a similar mass adoption curve “to migrate from our laptops to our pockets.” The company claims there has been more than 500% growth in Web3 mobile apps available in the Google Play and iOS app stores over the last three years. Meanwhile, blockchains like Polygon and Solana have announced mobile partnerships and manufacturers like HTC have launched Web3-enabled devices.

“While it’s not yet clear what the ‘killer app’ of 2023 might look like, we expect there to be one — if not many — blockchain-based mobile apps on the leaderboard,” says Liquin.

That said, there’s a battle ahead as Web2 Big Tech seeks to retain control. Vayner3 picks on Apple’s “polarizing policy” on in-app purchases with which it seeks to maintain its control and fee structure. Liquin says this has implications for how Web3 app builders deploy and monetize Web3 apps in Apple’s App Store, “which will likely stifle Web3 innovation potential on Apple’s iOS.” The report adds: “the mobile world may be a Web3 battlefield in 2023.”

Other Predictions from the Report:

Web3 is not just for engineers and developers: Enterprises across Entertainment, Retail, Fashion and Tech are hiring dedicated Web3 teams as well. Vayner3 expects them to play a significant role in broad Web3 adoption “through internal education, evangelism, and community-building at many of the largest organizations in the world.”

Crypto payment is more than just a marketing stunt. In 2023, Vayner3 expect more opportunities for consumers to use crypto for everyday purchases. It backs this up citing a recent survey of 2,000 senior execs of US retailers, which found that 75% of them plan to accept cryptocurrency payments within the next two years.

The metaverse is still a long way away and is not poised to be a mainstream driver of Web3 tech or culture in 2023, according to the consultancy.

Mainstream adoption of blockchain-based ticketing may be further off than 2023. At the same time the company expects a wave of IRL activations, deeper engagement with consumers, and new channels for retargeting and post-event community building “to gain meaningful momentum in 2023, specifically during conference and festival season this summer.”

“The hype has died down, but the genie is out of the bottle,” the consultancy declares, advising businesses to build provisions for IP rights, digital asset consideration, and revenue share into agreements with talent, sponsors, venues, and other partners.”

Does Web3 offer the promise of a truly decentralized internet, or is it just another way for Big Tech to maintain its stranglehold on our personal data? Hand-picked from the NAB Amplify archives, here are the expert insights you need to understand Web3’s potential and stay ahead of the curve on the information superhighway:

In the Internet of You (IoU), smart tech will be connected into an intelligent network providing hyper-personalized services and assistance.

January 25, 2023

Posted

January 1, 2023

It’s All About the Video: 5G in 2023 (and 2028)

TL;DR

Ericsson predicts 91% of the North American market will have adopted 5G by 2028.

The company is betting that mobile subscriptions have started to level off, betting that the next six years will only add 800 million new subscriptions.

Advances in mobile technologies could quintuple data used by 2028.

If you consider your smartphone a multimedia/multipurpose technology device, then Ericsson’s mobile reports are for you. The latest edition is available here.

North America and northern east Asia (e.g. China, South Korea, Taiwan) lead the way in 5G adoption, for now. India is expected to be a big player as it continues efforts to launch its own high-tech future, one that embraces all of the country not just a few select well-educated metropolises. Similarly situated countries, such as Indonesia and Nigeria, are also showing strong early adoption numbers.

The report says, “In 2028, it is projected that North America will have the highest 5G penetration at 91%, followed by Western Europe at 88%.”

In terms of current usage, “North America and North East Asia are expected to have the highest 5G subscription penetration by the end of 2022 at around 35%, followed by the Gulf Cooperation Council countries at 20% and Western Europe at 11%.”

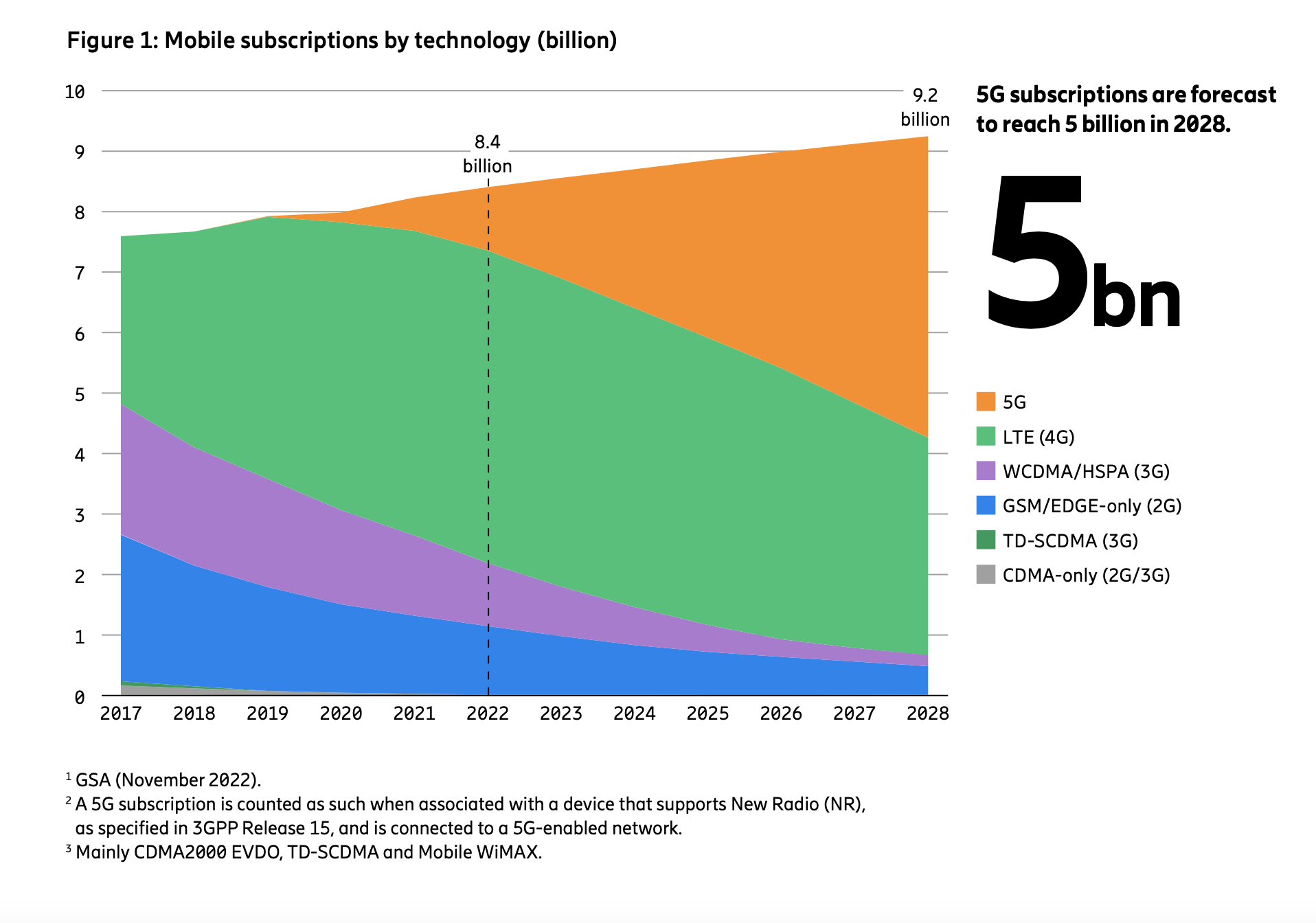

By 2028, Ericsson expects 5 billion 5G subscriptions worldwide.

There is also a prediction that mobile subscriptions (mostly smartphones) will reach 9.2 billion in 2028, up from 8.4 billion calculated for this year. That doesn’t sound like a lot of growth, indicating that nearly everyone who wants a mobile subscription probably has one; remember that there are more than 8 billion people on planet Earth as of 2022.

The report’s “5G in South East Asia and Oceania: A closer look” section looks into that region and the plans to move many, if not all, of those developing countries (referring to notably The Philippines, Malaysia, Thailand, Vietnam and Indonesia) into the first world on the wireless front over the next several years. Ericsson thinks that total mobile data traffic in that region will quintuple between now and 2028.

(BTW, that’s why Ericsson may have underestimated its 2028 figures. There are going to be a lot of new people hopping onto the wireless train in the next few years.)

5G Driving Mobile Data Growth

That’s the where. As to the why, perhaps the most interesting section is “5G to drive all mobile data growth.”

That assessment probably doesn’t surprise anyone, but the incline of the rise should open eyes. In other words, what we’ve seen in the explosion of mobile device data usage over the last five years is a ripple compared to a coming tsunami in the next five years. Much of that will be in video, accounting for as much of 80% of mobile network traffic.

4G continues to grow as well, but the report predicts it will peak soon with a gradual decline in its market as 5G is implemented in more locales, regions and countries, along with the usual gradual tech swap out takes over.

“Fixed Wireless Access” is also a growing sector, per Ericsson. These are broadband wireless access points, currently numbering around 100 million, at businesses or on towers for public and private use.

Besides human users, smart devices for the Internet of Things are continually developing. Ericsson expects that market to get hotter, possibly by five times by 2028, with over 300 million access points by then. Northern east Asia is a particular hot spot for them.

5G Roadblocks

Among the things slowing even faster deployment, depending on the country involved, includes making radio frequency spectrum available.

Lower, less RF-efficient bands, below 7 GHz, are the first auctioned off, but they realize the weakest, though cheapest, performance. These bands propelled 3G and 4G in most technologically capable countries and are the technology breeding grounds for developing countries.

Now it comes time to fill out the 7 GHz group and move to the 24 GHz band and above, where 5G can flex its muscles. Being able to operate in multiple bands allows for efficient service uses — low-bandwidth items, for instance IoT and voice-only traffic, can flow unimpeded while high-bandwidth-hungry video and gaming services can operate in the same network on a higher frequency band.

AR for Mobile

The report touches on augmented reality for mobile devices (think Pokémon everywhere 24/7!) and a slow acceptance of improved smart glasses and visors. Ericsson acknowledges the technology and its support ecosystem have yet to mature.

Looking forward, the report says: “As the AR ecosystem develops, traffic arising from AR usage could significantly impact the current forecast. The amount of traffic that will be generated over mobile networks, in addition to mobile broadband and fixed wireless traffic, will depend not only on the uptake and utilization rates of the applications, but also where the critical functions mentioned in the ‘AR devices’ section take place.”

That other processing location will be in a vast network of edge services and network-inhabiting hard and soft virtual processors — all utilizing 5G technology and networks.

On a less technical note, the report also describes a growing practice in flexible bundle packaging for services. These can include gaming, content aggregation, differing speed levels, shorter contracts, to appeal to consumers have more choices among service providers.

6G may already be on the horizon, but there’s still a lot to understand about the benefits — and limitations — of 5G, which is rolling out across the US but has yet to reach peak saturation. Dive into these selections from the NAB Amplify archives to learn what, exactly, 5G is, how it differs from 4G, and — most importantly — how 5G will bolster the Media & Entertainment industry on the road ahead:

Already progressing from early to mass adoption, 5G is enabling the transition from immersive services to metaverse experiences.

January 9, 2023

Posted

January 1, 2023

After Tests and Improvements, 5G Network Slicing Opens Up to Broadcasters

TL;DR

Network slicing is a capability of the 5G standard which is being tested and gradually rolled out. It enables operators to carve up their 5G network into slices that can be finely tuned to suit the needs of many customers.

5G Network slicing revenues will grow over 100 times by 2029 to reach more than $16 billion in revenue that that would otherwise not be generated.

Telstra, Ericsson and Qualcomm achieve new download speed benchmark of 7.3Gbps.

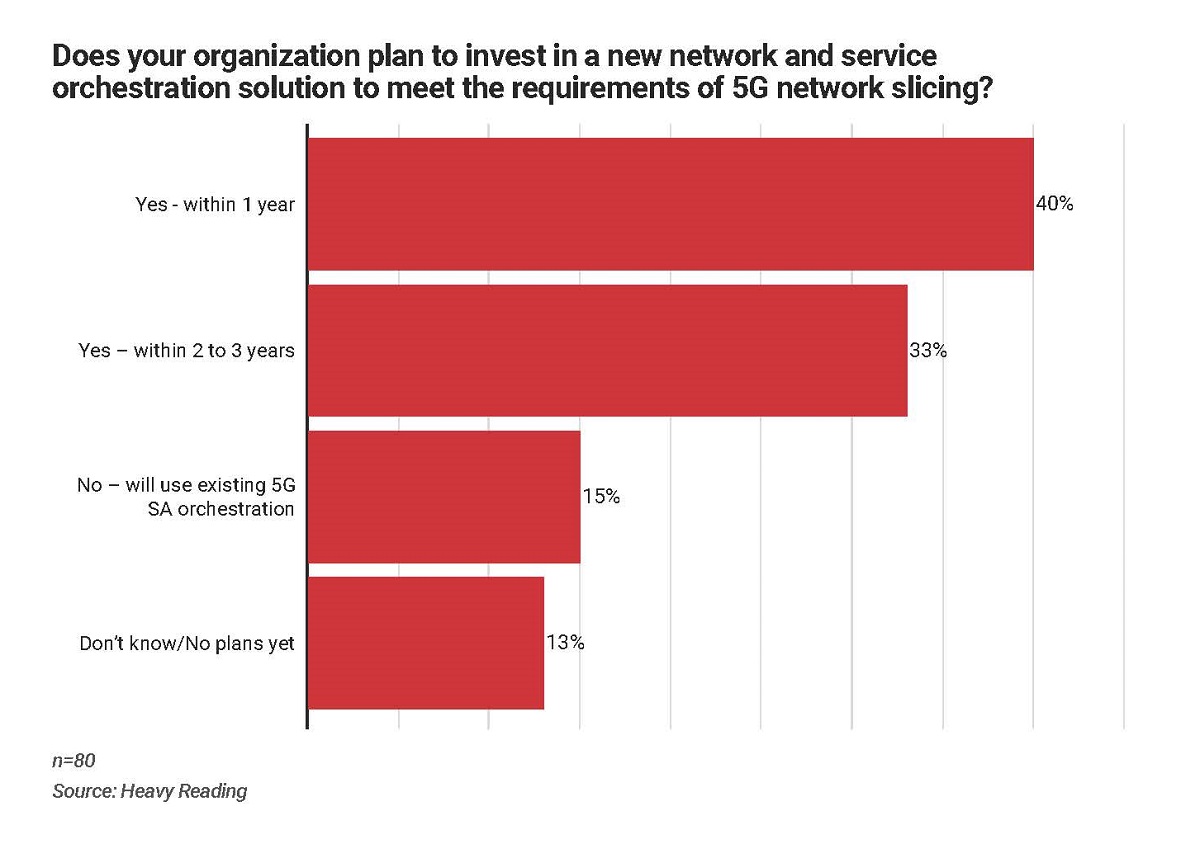

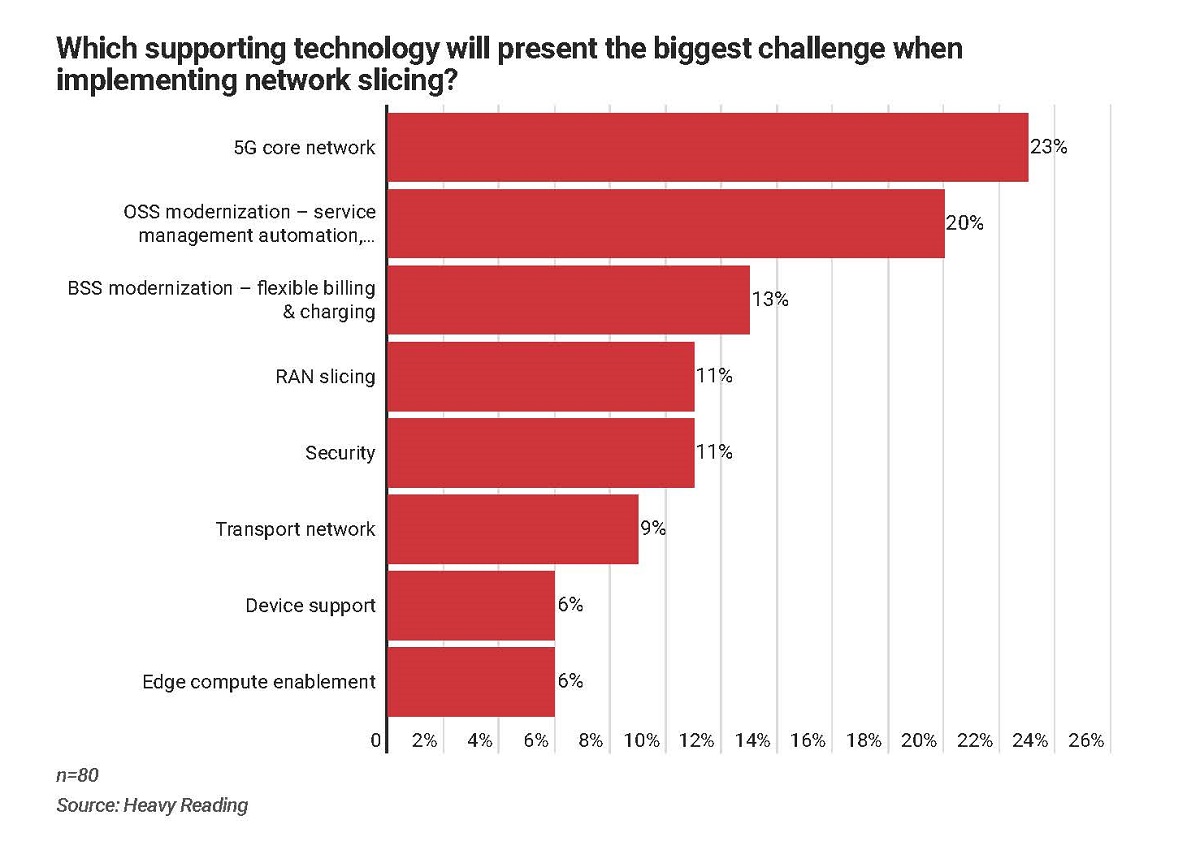

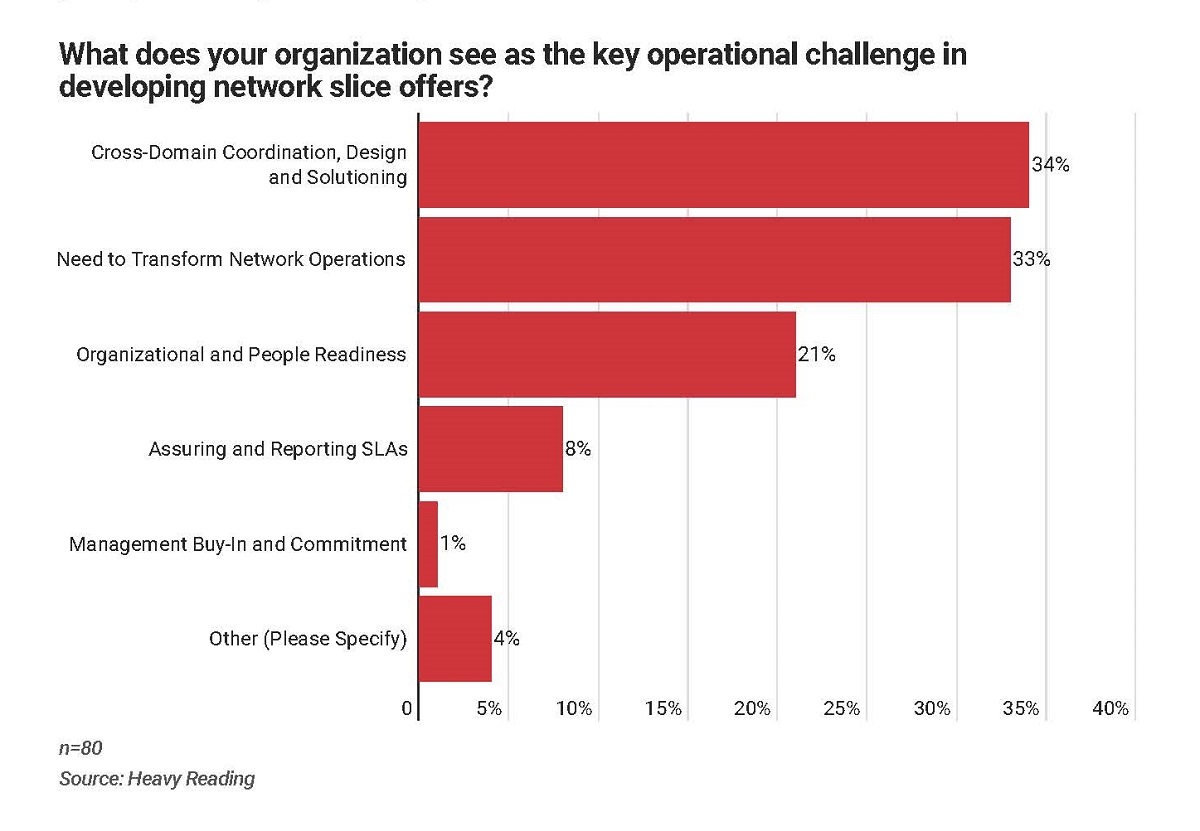

There are signs that operators will commercialize 5G network slicing over the next two years, finds the new 2022 “5G Network Slicing Operator Survey” from consultancy Heavy Reading. The emphasis initially will be on enterprise services, but broadcasters are also eager to use the technology to improve coverage of live events.

Network slicing is a mechanism to isolate a segment of the 5G network end to end in a local area for the specific requirements of a customer.

Rethink Technology Research predicts that network slicing will add revenues of $16.1 billion by 2029 over above what 5G infrastructures would have earned otherwise.

Its report further identified manufacturing as likely to generate the biggest slice of network slicing revenues by 2029 at 19% of the total, with energy/utilities and healthcare joint second on 15% each and M&E media/entertainment on 7%.

Yet “the surge” in revenues will not really begin until 2024 when there is substantial base of 5G Standalone infrastructure to build on.

Standalone (SA) represents the full 5G infrastructure including RAN (Radio Access Network) and Core, which is essential to unleash the full capability of network slices to enable differentiated services catering for multiple user groups and applications sharing the same physical network,” explains Rethink.

Broadcasters are keen to use 5G slicing to augment coverage and reduce the costs of outside broadcasts such as sports matches, mass public celebrations or news gathering. By their nature these are congested areas in which wireless bandwidth is in short supply and for which the only option until now has been expensive uplink by satellite.

Tests over the past couple of years among broadcasters and telco operators appear to confirm that the technology is on the verge of being viable for practical use.

TBS regional chief Karen Clark said the tests clearly demonstrated the effectiveness of 5G slicing for uplink of live, premium video feeds “to produce high bandwidth, low latency television from a congested venue, without the need for traditional wired infrastructure.”

Paramount (Australia and New Zealand) also partnered on the project. Its VP of technology, Dean Wadsworth, claimed the success of the trial “demonstrates that coverage of live events can be enriched with reliable links from roving crews, which can be more cost-effective.”

All parties point to exploring further opportunities in the near future.

Yet such event-based scenarios are deemed the lowest priority among telcos, as reflected in a Heavy Reading survey conducted last summer. Principal analyst Gabriel Brown suggests this may reflect the challenges with addressing demand that is short term/transient in nature with a relatively immature technology stack.

“Short term, network slice instances will have greater requirements on automation. Perhaps as slice management technology matures, this use case will rise higher on operator priority lists.”

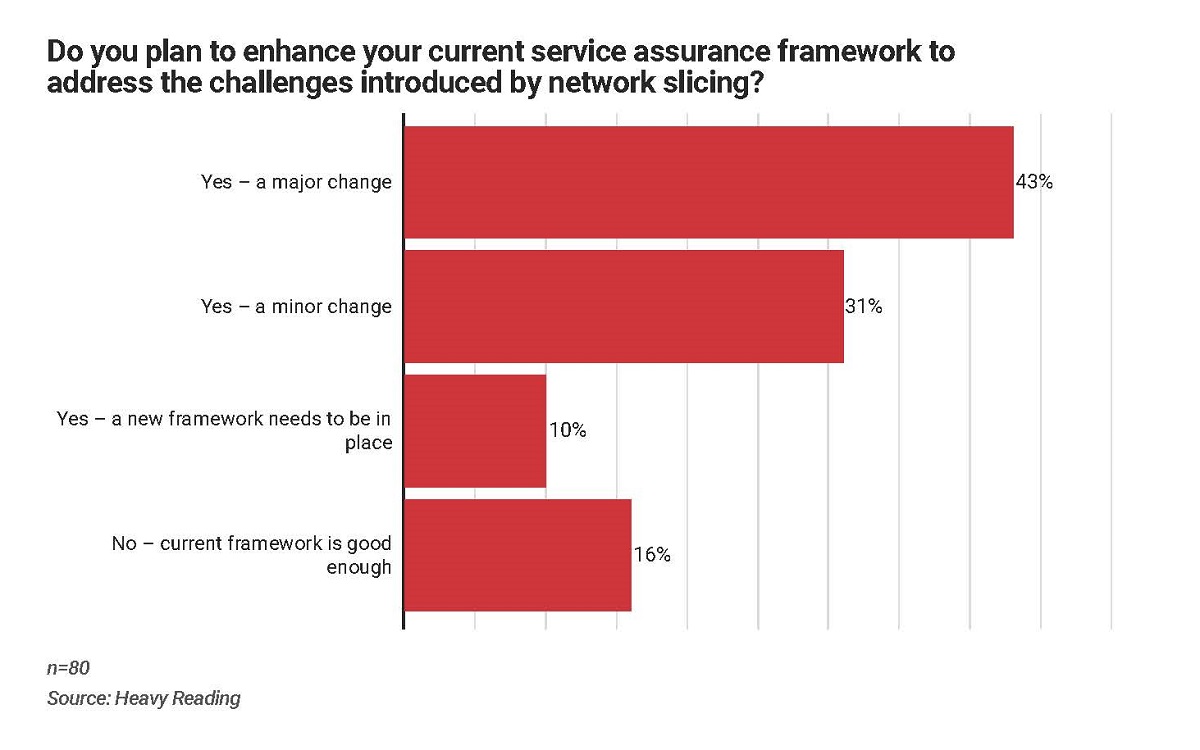

A survey of staffers at telcos (or communications service providers) by Heavy Reading earlier this year found that the industry had a job to do to educate potential customers about the benefits of the tech.

Less than a third of respondents said “most customers understand the concept and see value in it,” which implies that two-thirds did not.

“Operators, and their vendor partners, will need to invest in customer education to demonstrate the value of network slicing,” advised Brown.

As an aside, Telstra and Ericsson partnering with Qualcomm Technologies just recorded a new 5G download peak speed benchmark of 7.3Gbps achieved at a Telstra live mobile site located at the Gold Coast, Queensland Australia.

This improved peak speed capability further will help Telstra to deliver network slicing. By adding improved peak speeds and capacity, Telstra says it can deliver more capable network slices to more customers.

Network slicing could potentially be used to reduce, control and uplift the video performance of major streaming services like Netflix and Google.

As Heavy Reading’s Brown explains, most of the traffic on broadband networks is generated by customer demand for services from OTT. Approximately 56% of global network traffic is generated by six companies, according to Sandvine.

“In mobile networks, it is logical to consider how network slicing may be able to improve the performance, efficiency, and user experience of the most in-demand services or enable new service experiences offered by these types of providers (e.g., virtual reality gaming, metaverse meetings, or similar).

“This is, however, a thorny topic, given issues related to net neutrality and because, in some markets, some telecoms are actively lobbying regulators to levy charges on OTT internet companies to carry traffic.”

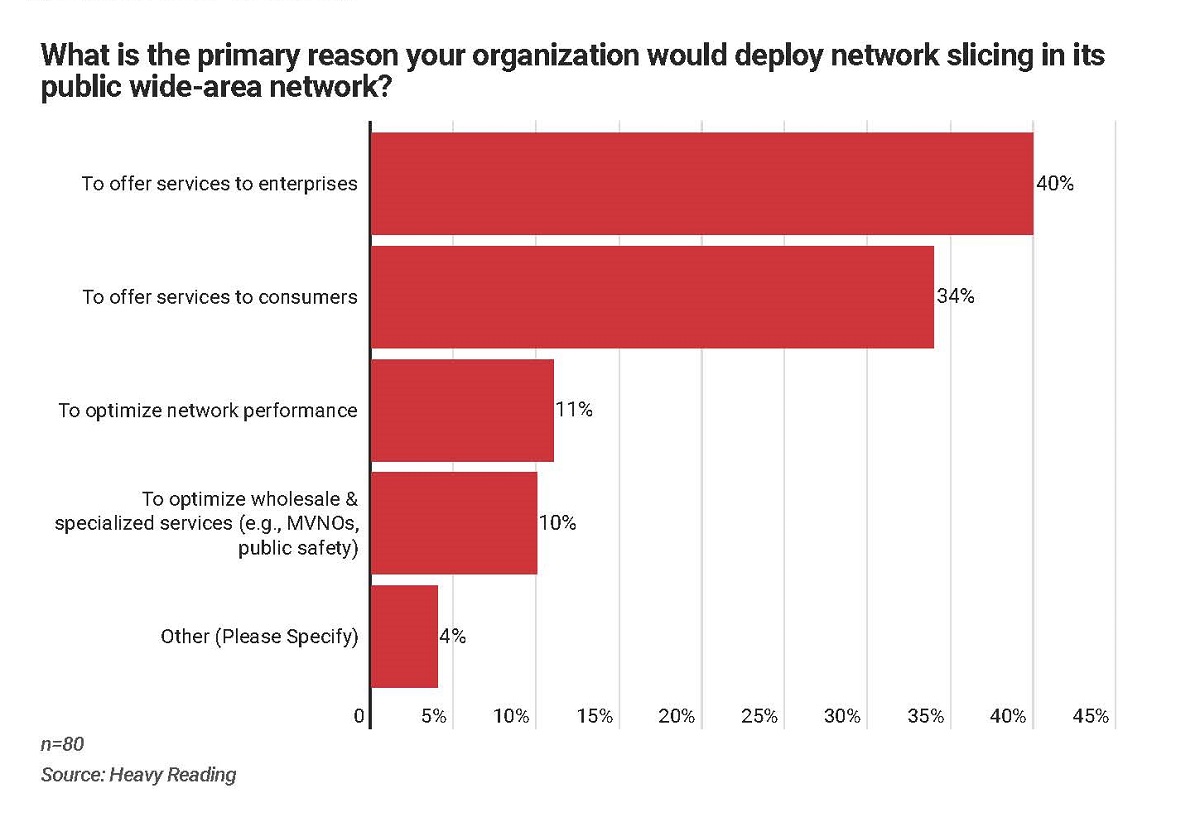

Asked if they anticipate working with internet companies “to use network slices to deliver and monetize high volume OTT services,” Heavy Reading’s survey revealed that 40% of respondents say their company plans to do this, ahead of a more equivocal 31% that may do so, depending on the business case.

“Presumably, the thinking is that network slicing will provide a capability that improves the service, and the operator can somehow charge the OTT provider for this or monetize the customer via a revenue share,” surmises Brown. “In this analysis, it is tempting to ascribe this 40% result to wishful thinking by telecom respondents.

“An alternative analysis, therefore, is to be aware that what is normal in terms of telco and OTT working relationships today will not necessarily stay that way.”

As application performance requirements become more stringent, and as customer expectations increase and new services emerge, there will be a need to rethink and re-architect how telcos and internet companies interact. In mobile networks, 5G network slicing will potentially allow a closer working relationship that benefits customers.

6G may already be on the horizon, but there’s still a lot to understand about the benefits — and limitations — of 5G, which is rolling out across the US but has yet to reach peak saturation. Dive into these selections from the NAB Amplify archives to learn what, exactly, 5G is, how it differs from 4G, and — most importantly — how 5G will bolster the Media & Entertainment industry on the road ahead:

5G is set to generate $7 trillion in economic value by 2030, InterDigital reports, as it fuels a proliferation of connected devices.

December 27, 2022

Just Think About the Metaverse Like a Media Channel

Image by Kohji Asakawa

TL;DR

Most Americans think the metaverse will be considered mainstream by 2028, according to a new survey from TELUS International.

Brands are expected to interact with consumers in virtual worlds — but there are limits and concerns.

Content moderation must be incorporated to ensure users experience a safe and inclusive environment. This will mean employing a mix of AI and human moderators to ensure a timely, accurate and inclusive review of online interactions.

The metaverse is already a media channel for brands. According to a new survey by TELUS International, around three-quarters of American consumers believe that brand interactions in the metaverse will one day replace those in the real world. In fact, 65% of respondents believe the metaverse will be considered mainstream in the next five years.

Half of those polled said they would choose one brand over another if it offered a superior experience in the metaverse. Additionally, more than a quarter (27%) indicated they would pay a 5% premium for a product or service that was supported by a quality metaverse experience, and 22% would pay up to 10% more.

“Just as the internet and mobile apps revolutionized the way we interact with brands and consume information, goods and services, the metaverse offers brands exciting opportunities to interact with consumers in entirely new ways,” Michael Ringman, chief information officer at TELUS, shares.

“Digital 3D worlds open up a window of opportunity for brands — it offers them a space that’s accessible, allowing them to connect with consumers globally in unique and interactive ways, providing consumers with an enriched customer experience.”

The pressure is on for brands that choose to engage with consumers in virtual worlds. The survey indicated they expect interactions with brands in the metaverse to be more engaging (53%) and better customized to their interests (49%).

When asked what would encourage respondents to interact with brands in the metaverse, the top response was the ability to realistically try out or try on products and services (41%).

Cr: TELLUS

There is, however, a limit to what surveyed consumers feel comfortable doing and purchasing in the metaverse, even with these enhanced experiences. For example, only 35% would buy a house or rent an apartment in the real world through the metaverse. This is in stark contrast to survey respondents saying they would feel comfortable gaming (79%) or engaging with a brand’s customer service (68%) in the metaverse.

There are concerns too. For example, 60% said they believe it will be easier for individuals to get away with inappropriate behavior in the metaverse and just 45% think brands are prepared to moderate content in order to keep users safe. Most people don’t consider AI alone to be enough of a safeguard against malicious content.

“Like we’ve seen with digital environments that have come before it, the metaverse is unfortunately not going to be immune to users who abuse these spaces, putting brand reputation and their customers at risk,” Ringman says. “As brands begin to explore this new platform, content moderation must be incorporated during the initial planning phase to ensure users experience a safe and inclusive environment. This will mean employing a mix of AI and human moderators to ensure a timely, accurate and inclusive review of content and behaviors.”

The metaverse may be a wild frontier, but here at NAB Amplify we’ve got you covered! Hand-selected from our archives, here are some of the essential insights you’ll need to expand your knowledge base and confidently explore the new horizons ahead:

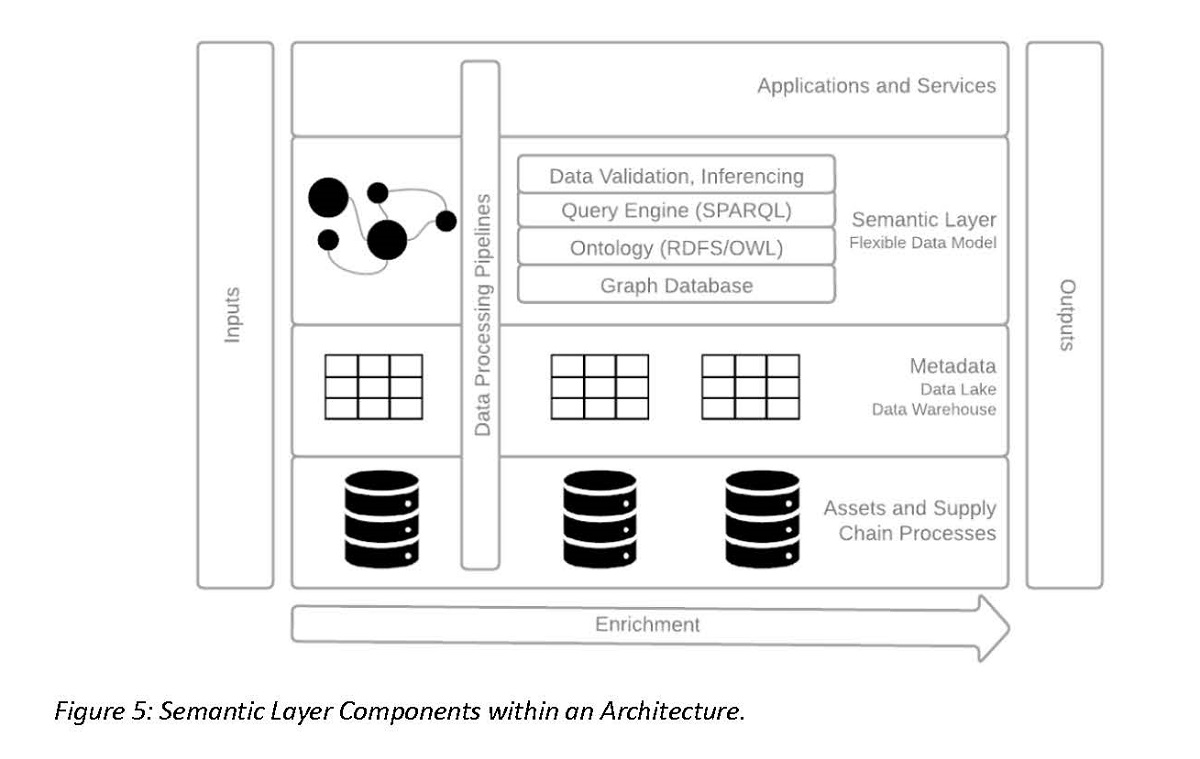

The guide explains media ontologies in simple terms, provides a useful discussion of mapping data across different information systems, and offers practical examples of how media organizations are using semantic web technologies to bring greater efficiency to real-world workflows.

Understanding and managing the complex relationships between all elements in the content life cycle — from scripts to assets to the tasks being performed across media workflows — requires richer metadata.

SMPTE, MovieLabs and the European Broadcasting Union have published a guide to working with cloud technology as part of the overall industry effort to standardize production and distribution in the cloud.

World Wide Web co-founder Tim Berners-Lee first proposed the semantic web in 2001. This was the concept of moving from the mere presentation of content on the web to actionable human and machine-readable data.

Movement towards such a web has been slow, SMPTE details in the guide, but may now be regarded as accelerating thanks to a convergence of mechanisms and specifications that make it more practical and more desirable. These include the cloud itself, which is not a requirement for the use of semantic web technologies but is certainly a catalyst; microservices and application programming interfaces (APIs); artificial intelligence (AI) and machine learning (ML); and media-specific ontology specifications.

As the guide outlines, the movement into the cloud comes with attendant expectations around automation, agility, and scalability and challenges in areas such as interoperability, portability, discovery, and orchestration.

“It is an ever more data-driven eco-system with an increased need for consistent, interoperable metadata and semantics to drive and manage distributed processes and workflows. Fortunately, semantic web technologies — which may be regarded as internet-native — have great potential to address some of these challenges, supporting the combination of standards-based machine-readability with the representation of human subject matter expertise.”

Unfortunately, there is a lack of awareness about what semantic technologies are, what ontologies are, where they are applicable, and how to deploy them.

“The shift of media workflows to the cloud — an ever more data-driven ecosystem — yields many benefits, including greater automation, agility, and scalability. But to realize these, organizations must successfully address challenges related to workflow interoperability, data portability, and the management of complex sets of assets,” said MovieLabs CTO Jim Helman. “Media ontologies provide the essential knowledge framework to address those challenges.”

(Click the image above to view a larger version.) Functional Stack: An illustrative, rather than prescriptive, representation of the components of a semantic layer within an architecture. The key characteristics of an eco-system employing a semantic layer or knowledge graph is the separation of the logical and physical layers and the use of predictable and standardized technologies in the logical representation. Cr: EBU/MovieLabs/SMPTE

What is an Ontology?

For the purposes of this paper, an ontology is a formal model that represents a given “knowledge domain” — meaning the entities that are meaningful within that space and the relationships between them — using a set of specifications developed by the World Wide Web Consortium (W3C): primarily RDF; RDFS; OWL; SKOS and SPARQL.

“In practical terms an ontology represents explicit business knowledge and provides the scaffolding for the core data infrastructure of an enterprise or a broader field,” says the Guide.

It goes on: Understanding and managing the complex relationships between all elements in the content life cycle — from scripts to assets to the tasks being performed across media workflows — requires richer metadata. An ontology provides a framework needed to support application and service integration, asset and content management, and search and discovery, among other functions.

The utilization of RDF in particular provides a mechanism for information exchange between applications without a loss of meaning and for creating linked data, meaning data that is interlinked with, and enriched by, data from heterogenous and distributed sources.

The paper warns that semantic technology is not a magic bullet. It does not necessarily replace other technologies and is not a good fit for every use case. It is not as mature as the relational database/SQL eco-system, which may be more appropriate for predictable and consistent data that is not characterized by many or complex relations, and for which there is a greater pool of expert human resources.

However, we learn that semantic technology can be smartly stacked with other tools and is in broad terms a good fit for cloud-based eco-systems, having its genesis as a web-based approach to knowledge management.