M&E Is Investing More in Social Media — and It’s Paying Off

Adrian Pennington

TL;DR

Traditional media has officially stepped into the world of socially integrated media. Social-first content creators are emerging within Hollywood — and it’s working to capture the attention of social audiences and reach new viewers.

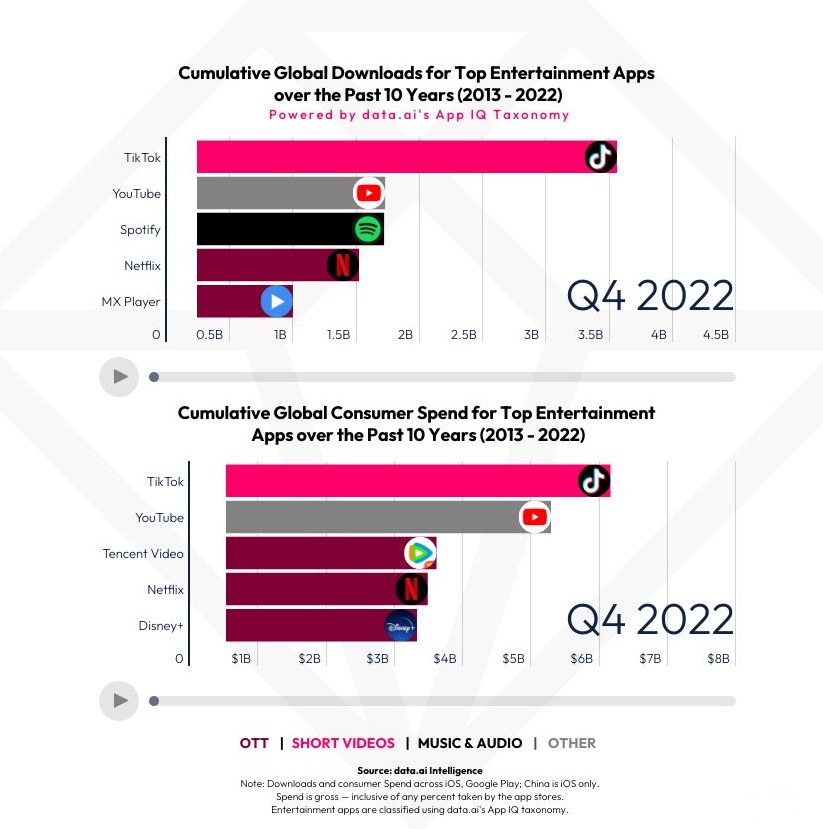

The “2024 State of Video” report from research specialist Tubular Labs found that long-form content is on the rise even on platforms like TikTok andInstagram, where M&E publishers are seeing greater engagement.

Broadcast, cable, and radio channels have generally used short-form platforms to drive viewers to long-form content platforms, but in 2024 traditionally short-form video platforms are now incorporating long-form content.

It hasn’t happened overnight, but media publishers have recognized the viewer and consumer power of social audiences — and resources are following. In an overview of media growth on social video, research specialist Tubular Labs finds mainstream media exhibiting “unprecedented growth on social video proving that investing in platforms leads to measurable ROI.”

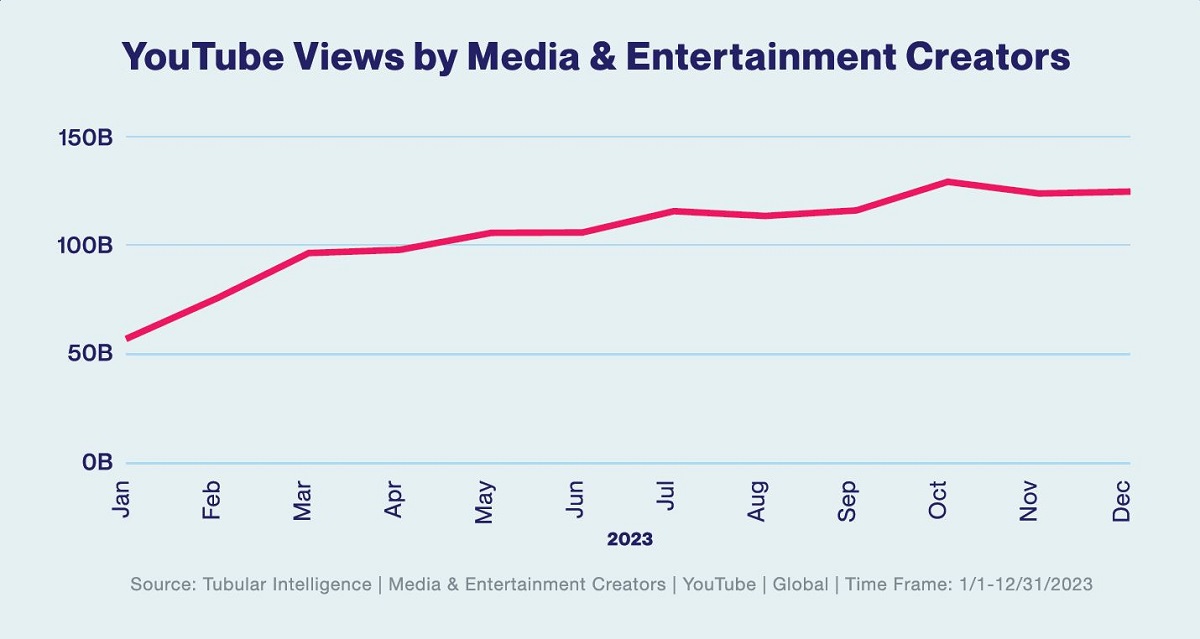

YouTube has been Media & Entertainment’s bread and butter platform for many years due to its long-form, landscape content format, which is easily adapted from televised content. In 2023, YouTube uploads by M&E channels increased by only 5%, which is consistent with previous years; however, this long-term effort has paid off. With just 5% more uploads in the same time period, views organically grew +118% from 59 billion in January to 124 billion globally in December.

Cr: Tubular Labs

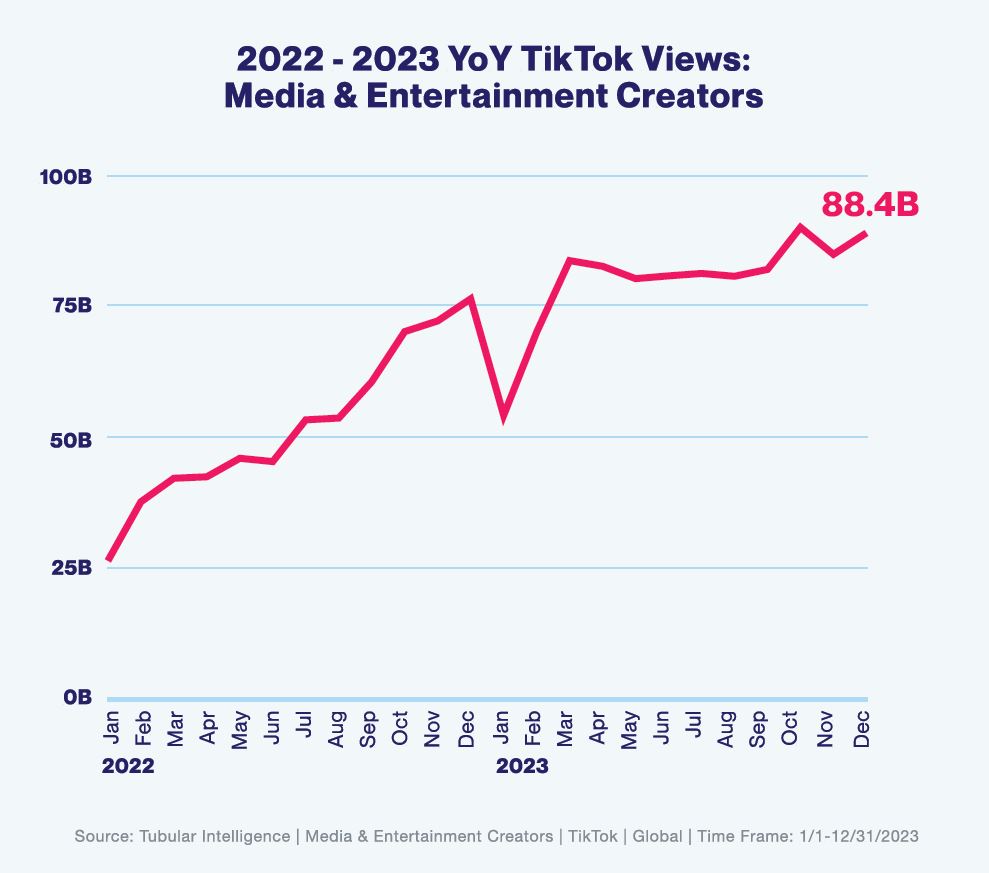

The “2024 State of Video” report also found that from 2022 to 2023, global M&E creators on TikTok posted 57% more videos and won 53% more views, receiving 36% more engagements.

While the US leads countries surveyed with 972 billion views of M&E-related posts on TikTok in 2023, Latin America is a fast-growing region. From 2022 to 2023, Brazil grew viewership by 32% (which is not far from the USA’s 39% year-over-year growth).

Cr: Tubular Labs

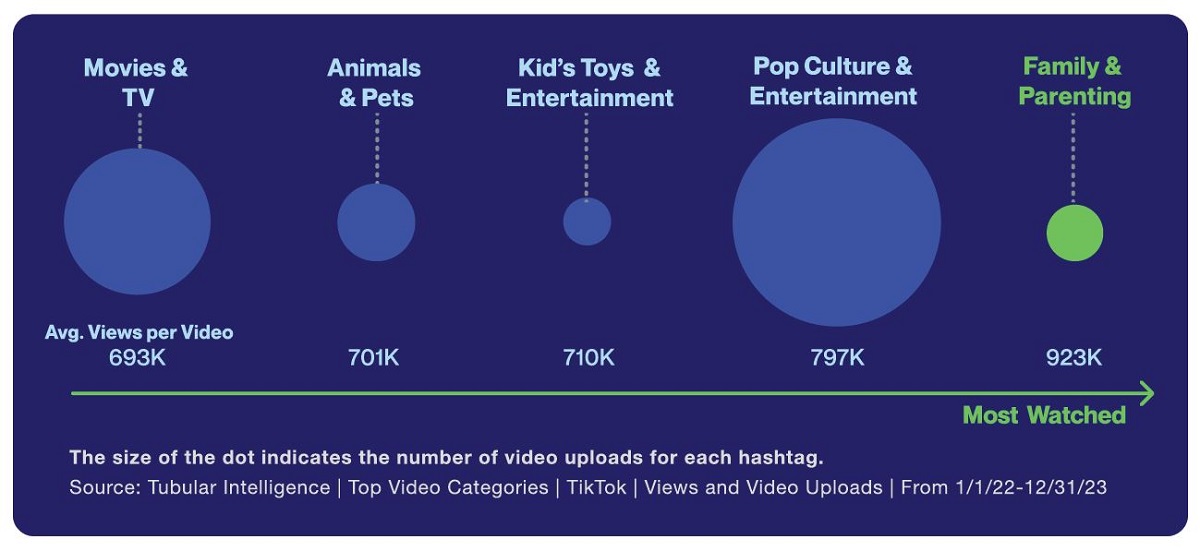

Movie and TV-related content on social media scored nearly 700 views on average per post last year, Tubular reports, although the leading growth category was related to Family & Parenting.

Sports viewership increased by 72% last year to a total of 71 billion views. Tubular expect this number to “skyrocket” in 2024 on the back of global sporting events, like the Paris Olympic Games.

Long-form Content IsMaking a Comeback

Since the rise of newer, short-form platforms like TikTok and Instagram, many publishers have refrained from posting long-form videos on those platforms. But in 2024 — that all changes.

“In the past, broadcast, cable, and radio channels used short-form platforms to drive viewers to long-form content platforms. However, in 2024, traditionally short-form video platforms are now incorporating long-form content, making it easier for creators to adapt content for different social platforms.

Cr: Tubular Labs

“Broadcast, cable, radio, and film channels who post long-form content have stuck to the status quo — uploading the majority of their content to YouTube and Facebook, but the latest data reveals a missed opportunity on short-form platforms.”

On TikTok, Tubular data reveals that of top publisher’s videos below the 30-second mark had the most uploads in 2023, but longer videos actually won the highest average views per video.

Tubular’s key takeaway: Experiment with longer videos on traditionally short-form platforms to earn more views and engagements.

Influencers & Commercial Media Align

In 2024, we see Hollywood stars and broadcasters integrating with rising social media influencers. These influencers have been used to fuel movie buzz, conduct red carpet interviews, and pave the way to show media companies how to connect with social audiences.

Rather than having to produce televised, digital, and social content, they can leave the latter to influencers, who arguably do it better.

Cr: Tubular Labs

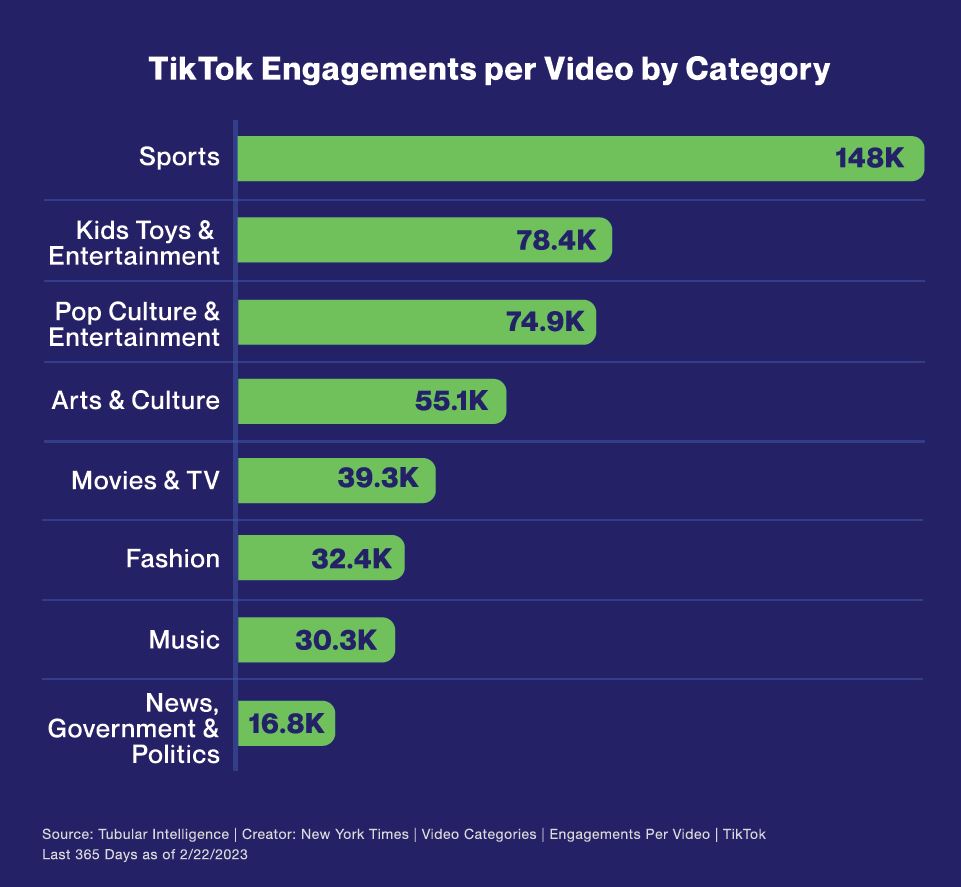

One example: Recess Therapy is a social media series hosted by an NYC comedian who interviews kids on the playground. The host and two of his famous young interviewees debuted their skills on the red carpet during the 2024 Golden Globes interviewing actors like Margot Robbie and Jennifer Lopez.

The result: Facebook videos about Recess Therapy and #GoldenGlobes won 121% more average engagements per video than Golden Globes content posted by a leading US Entertainment News channel.

Exclusive Insights: Get editorial roundups of the cutting-edge content that matters most.

Behind-the-Scenes Access: Peek behind the curtain with in-depth Q&As featuring industry experts and thought leaders.

Unparalleled Access: NAB Amplify is your digital hub for technology, trends, and insights unavailable anywhere else.

Join a community of professionals who are as passionate about the future of film, television, and digital storytelling as you are. Subscribe to The Angle today!

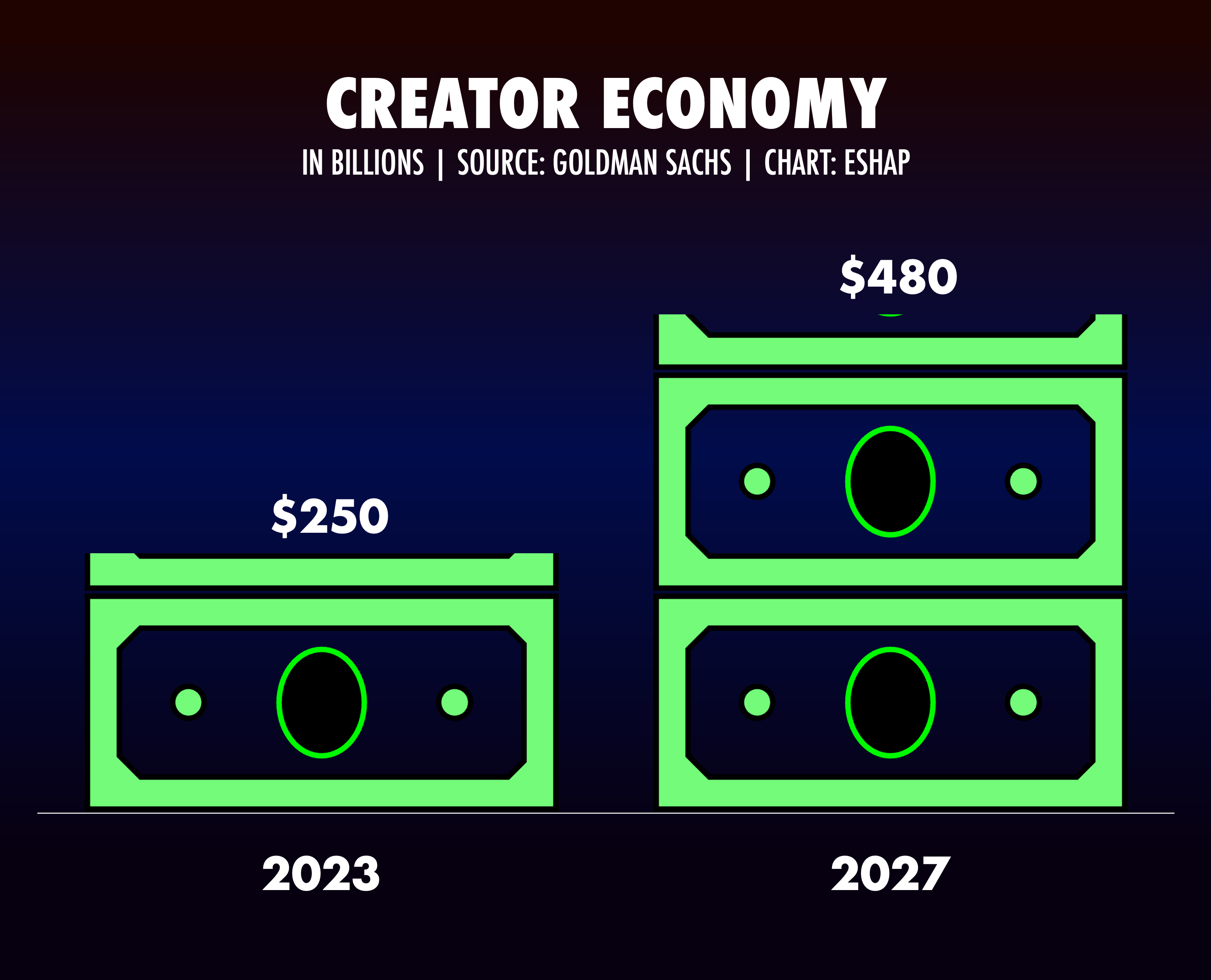

This year, the creator economy will generate a quarter of a trillion dollars in revenue, per Goldman Sachs. By the end of this decade, the creator economy will produce a half a trillion dollars in revenue. Industry commentator Evan Shapiro believes that the future of the media industry is being driven by the creator economy and that there will be far more opportunities to make money there than in the traditional gatekeeper ecosystem.

Evan Shapiro at NAB Show New York

That’s because of the industry-changing opportunity to go directly to fans and build communities of people who will pay for what an artist or creator produces.

Shapiro earns a living entirely from monetizing his work with online newsletters published on platforms like Substack, and counts himself as a creator.

He says the rest of the media industry needs to stop thinking about creators as influencers purely engaged in marketing and that the Creator Economy is driven by clicks on social media alone.

Taylor Swift and her self-produced, self-distributed Eras Tour movie, which made more than $250 million at the theatrical box office, is the poster woman for the creator economy.

From Taylor Swift’s film “Taylor Swift | The Eras Tour”

Sure, these multi-millionaires represent less than one percent of creators working in the creator economy but Shapiro points to the hundreds of thousands “making middle class livings.”

The secret, Shapiro says, is that “creator-led enterprises do not need to be massive enterprises, with tens of millions of followers to make money. Creators from an array of disciplines are able to build their own small businesses based not on impressions but cemented by their ability to monetize the love of their work from their small, passionate communities.”

YouTube series Snake Discovery, for example, is produced by the owners of a pet shop in Minneapolis. It will generate more than $125,000 from its 3,500 Patreon members alone, on top of merch (which they sell a lot of) and various other sources of income.

Shapiro argues that most creator economy gigs are not dependent on billions of clicks or tens of millions of followers. Most of the best opportunities will come from businesses like Snake Discovery, that build small but mighty, highly engaged, super passionate and loyal communities around their work.

This leads Shapiro to state, “We are at the precipice of an explosion of consumption and spending in what I call the Community Economy — a segment of media focused not on pure reach, but rather built entirely around monetizing the passions of specific audiences.”

The economic power of the media universe is shifting to the creator-led “Community Economy,” he suggests. Anyone in media who wants to make money (so, everyone…) — “even those who do not run their own creator-led businesses,” says Shapiro, “will need to learn how to ply their trades in the creator economy. Those who do will find opportunities as great or greater than those of the past gatekeeper Media era. Those who do not, will not.”

Is the industry, as Shapiro suggests, on the verge of an explosion in consumption and spending in the creator-led community economy?

Exclusive Insights: Get editorial roundups of the cutting-edge content that matters most.

Behind-the-Scenes Access: Peek behind the curtain with in-depth Q&As featuring industry experts and thought leaders.

Unparalleled Access: NAB Amplify is your digital hub for technology, trends, and insights unavailable anywhere else.

Join a community of professionals who are as passionate about the future of film, television, and digital storytelling as you are. Subscribe to The Angle today!

Casey Neistat is most famous as a YouTuber, but that wasn’t his goal… his career “wasn’t an option” when he started creating videos.

April 8, 2024

Posted

April 7, 2024

International Content Hits the Inflection Point

Jeon So-nee in “Parasyte: The Grey.” Cr: Cho Wonjin/Netflix

TL;DR

Ampere Analysis founder Guy Bisson says the global TV and streaming industry is shifting away from Hollywood toward a global rise in demand for non-English content.

The shift, says Bisson, is part of a wider and more fundamental story about changes in the content business over the past 18-24 months in which the studios refocused on streaming.

This change in direction is the result of a general slowdown in growth opportunities and cost pressures, he says, that were partly driven by investors who increasingly turned against the studio direct model.

The major streamers now produce more than half of their content internationally, an inflection point from traditional US-centric production to a more diversified and growing global approach.

Guy Bisson, Founder, Ampere Analysis.

In an essential Town Hall presentation at the 2024 NAB Show, Guy Bisson, executive director and co-founder of Ampere Analysis, will illustrate how the global TV and streaming industry is shifting away from Hollywood toward a global rise in demand for non-English content.

The shift, says Bisson, needs to be seen in context as part of a wider and more fundamental story about changes in the content business over the past 18-24 months in which the studios refocused on streaming.

That change in direction is the result of a general slowdown in growth opportunities and cost pressures that were partly driven by investors who increasingly turned against the studio direct model.

In addition, wealthy western markets were saturated for streamers. Simply put there were no new customers to find. One way of finding new customers is to look at demographic expansion. Streamers have traditionally skewed to a younger audience but there is still headroom among an old audience.

The bigger opportunity lies in international expansion which is why streamers have trained their focus on markets with room to grow.

From French limited series “Anthracite.” Cr: Christine Tamalet/Netflix

“Clearly the best way to target them is to provide content that will engage the audience in those regions and you do that by making content that appeals. That has been the big driver for the internationalization of content.”

The fact that it is expensive to produce content in the US as well as other countries like the UK is another driver.

“These three interrelated factors have all led to the internationalization of content. What it means is that the US is no longer the be all and end all of production, an issue highlighted during the 2023 strikes,” says Bisson.

“The changes in the business models that the streamers had planted created the environment in which those strikes took place.”

The Global Growth Opportunity

The Ampere boss is very clear that the US market remains “orders of magnitude bigger than anyone else in value terms,” but equally that the growth opportunity lies elsewhere.

There is still growth to be had in Western Europe markets, he says, including the UK, also Italy, France, Germany and Spain. Eastern Europe is showing growth too.

In Asia, South Korea has led the way with K-dramas like Squid Game; Japan is not far behind, being particularly strong in feature films (like Oscar winner Drive My Car).

In terms of where we’re going next, Bisson points to sub-Saharan Africa (in countries like Nigeria) and the Middle East.

He draws a parallel between trends now and that of multichannel growth when digital TV was introduced into the cable market.

“Over time thematic channels that were entirely programmed with US content evolved to become more and more local in terms of content, and continuity and presenters. We are seeing the same thing.”

Cr: Ampere

Streamers are funding content that has to work locally and for global distribution. Local content means local language, local actors and locations but with a production value and certain aspect of story and narrative that is global in appeal.

“Drama is generally used as a spearhead just as it was in the early days of streaming but beginning before the pandemic streamers have moved heavily into unscripted to the point today where over half of first run of original commissions — across the board from Netflix, Amazon, Disney, Warner Bros. Discovery, Apple and more — are now unscripted.”

Check the Numbers

Full year comparison of the number of scripted shows produced in the US for 2023 against the average of the previous two years shows a 38% decline. Netflix and Amazon now generate more than half of their content outside the US, underscoring a decreasing reliance on American production ecosystems. This global pivot is not merely a shift in geography but may signal a broadening of narrative scopes and audience engagement strategies.

“The majority of content on their platforms are scripted today but the majority of first run commissions going forward are unscripted with formatted content favored because of its adaptability to international markets.”

Ampere forecasts global investment change to grow upwards by 30% across 2023-2028. Central and South America will see increased investment, along with Asia and MENA & SSA, whereas a leveling off and slight decline is expected in Europe and the US.

Markets like India have proven hard for international streamers to crack despite its attractive scale, in part because of the relative low value per customer but premium advertising tiers may help grow subscriptions.

“Ads serve a dual function in both the US and international markets which is churn protection, giving customers who would otherwise leave an opportunity to downgrade and stay onboard,” says Bisson. “Ads also bring in a new market opportunity around people who might not have subscribed at all due to cost pressure.”

Exclusive Insights: Get editorial roundups of the cutting-edge content that matters most.

Behind-the-Scenes Access: Peek behind the curtain with in-depth Q&As featuring industry experts and thought leaders.

Unparalleled Access: NAB Amplify is your digital hub for technology, trends, and insights unavailable anywhere else.

Join a community of professionals who are as passionate about the future of film, television, and digital storytelling as you are. Subscribe to The Angle today!

Post-Peak TV streamers will lean more heavily on international content, take fewer risks, and return to network TV format and scheduling.

April 4, 2024

Posted

April 1, 2024

Doors of Perception: How Consumers View the Possibilities for AR/MR

TL;DR

Amdocs’ “The Era of Mixed Reality Report” offers insights into user behaviors shaping spatial computing technology.

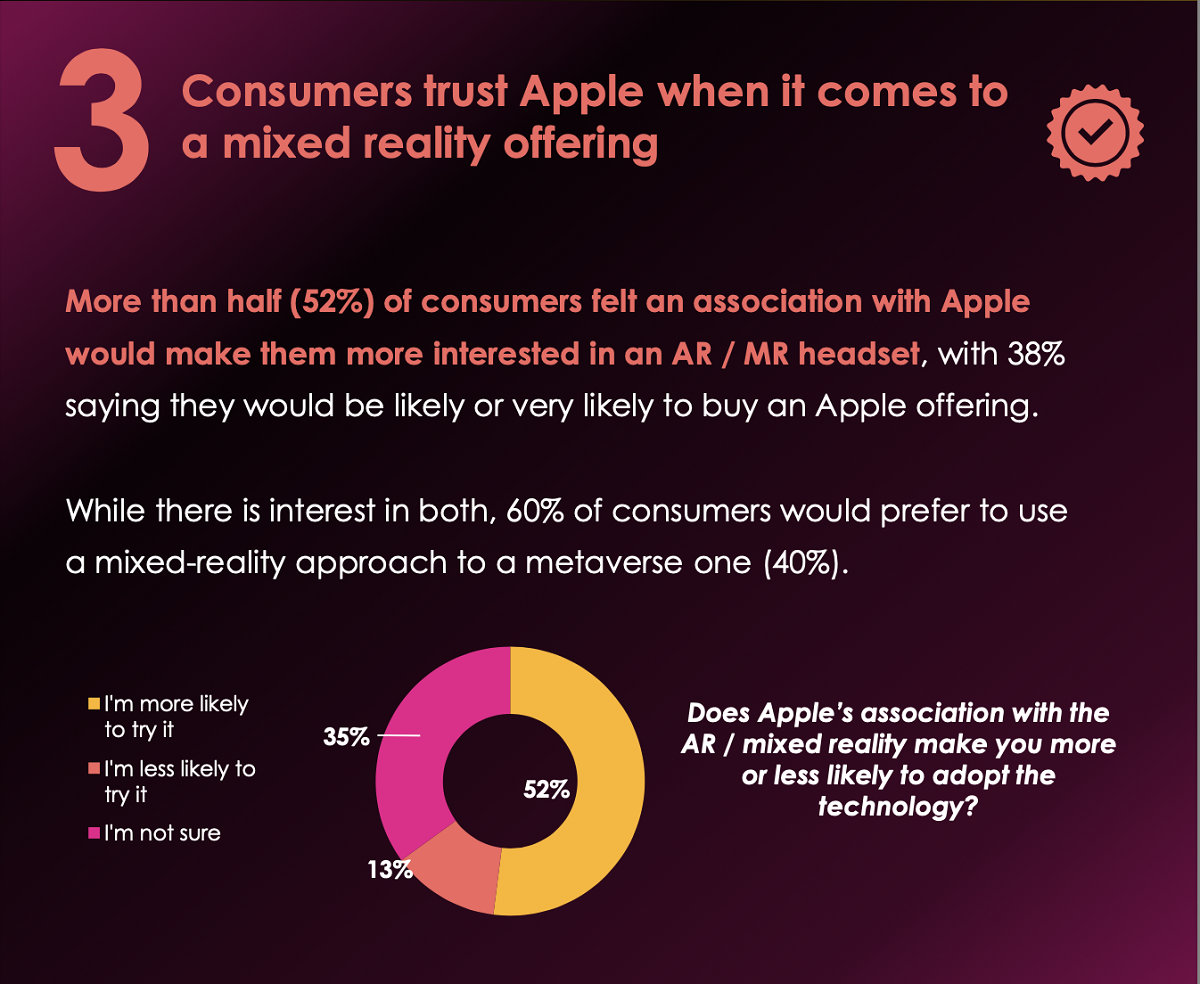

Consumers trust Apple when it comes to mixed reality. More than half of consumers feeling an association with Apple would make them more interested in an AR/MR headset.

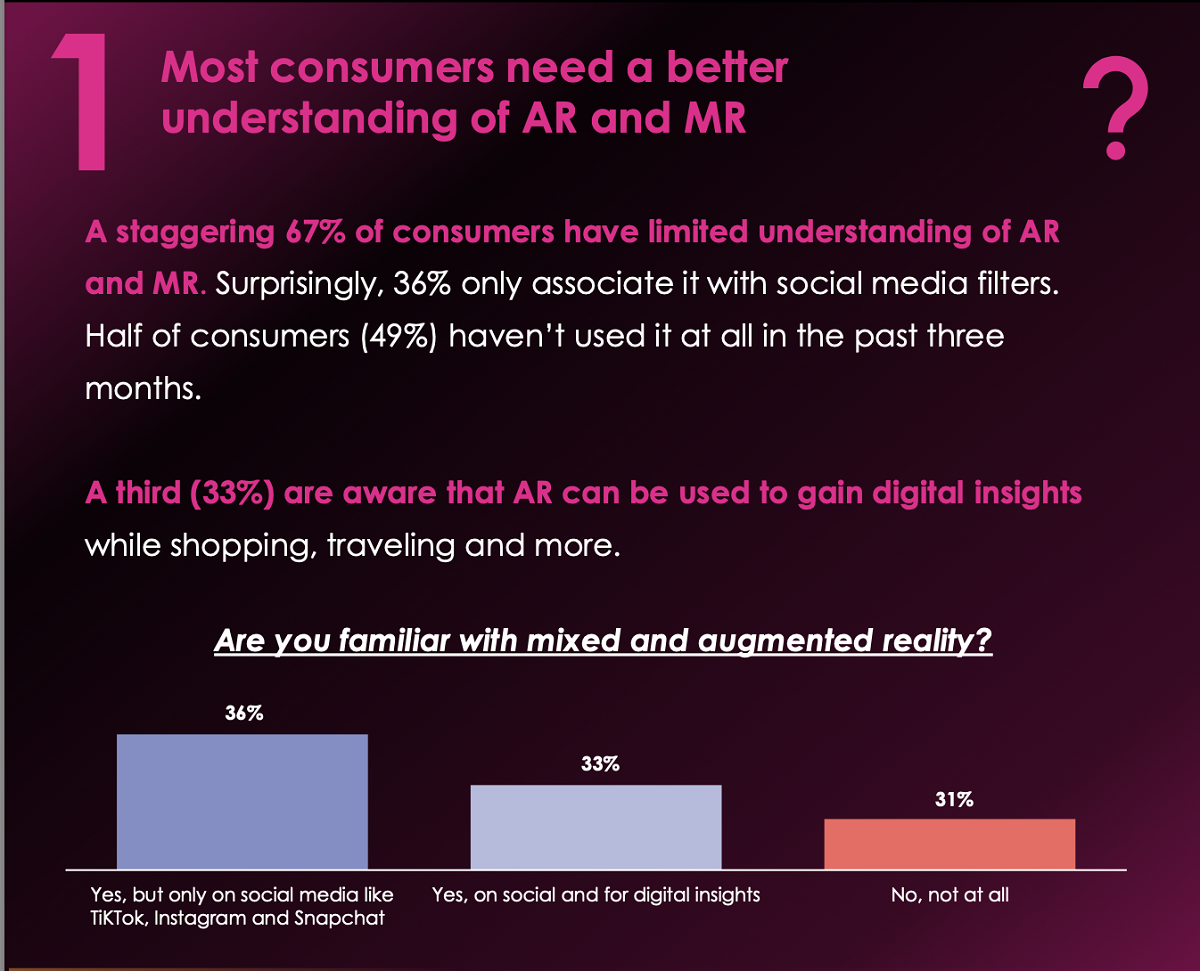

Nearly 70% of consumers have limited understanding of AR and MR, and nearly a third don’t have a clue what it is.

New research by Amdocs reveals that consumers are eager for more advanced augmented reality (AR) and mixed reality (MR) experiences, particularly if Apple is involved.

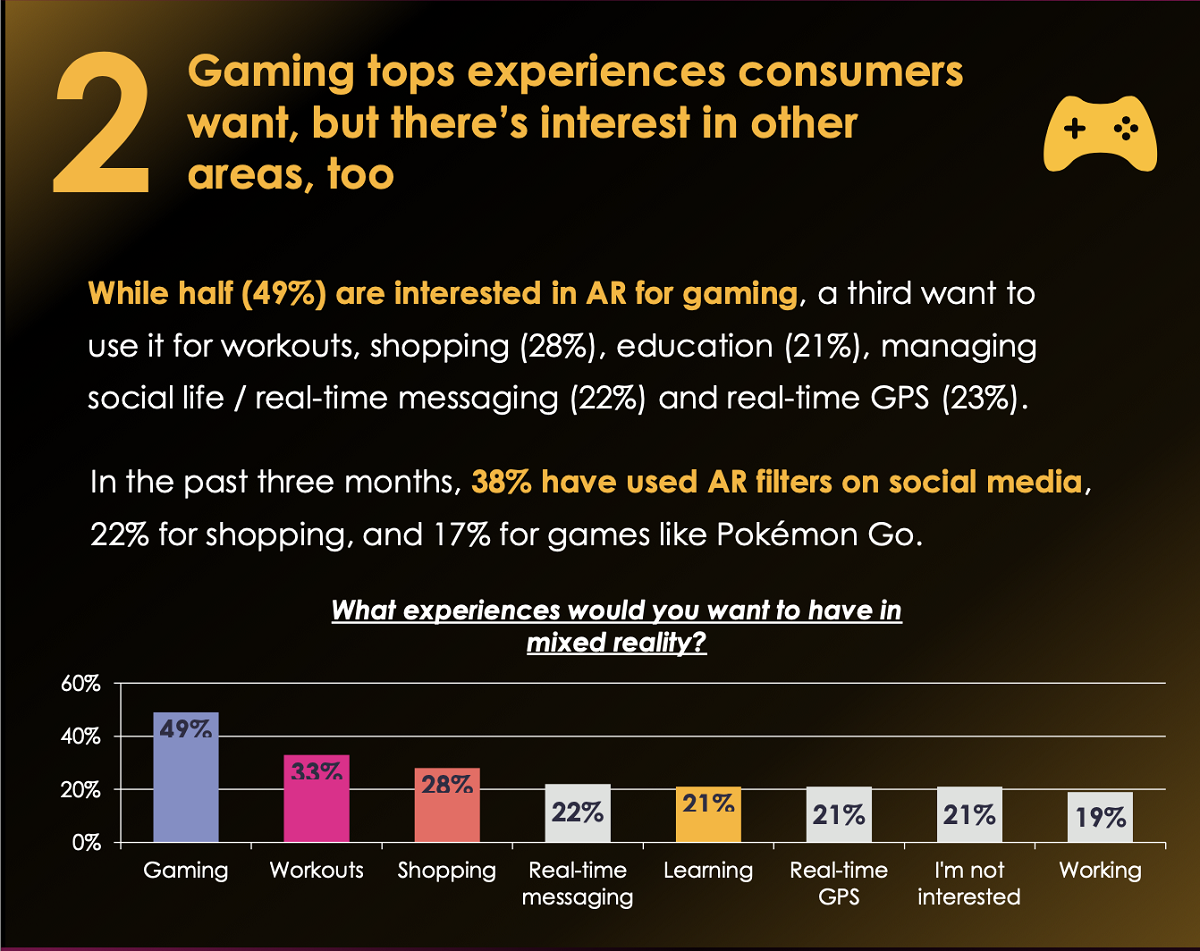

“The Era of Mixed Reality” report from Amdocs found that users are looking for these immersive technologies to enjoy gaming experiences first and foremost, with shopping and exercise not far behind. However, there is also a significant knowledge gap when it comes to AR and MR.

Cr: Amdocs

“Just like the iPhone turned the internet into mobile, mixed reality will disrupt how we interact with our surroundings and immerse ourselves in new experiences,” said Gil Rosen, CMO of Amdocs.

“But first, we’ll need to ensure networks, connected devices and the content that runs on top work together seamlessly. With immersive experiences, there is zero tolerance for lag or quality degradation, and to make it amazing, the entire ecosystem needs to evolve as one.”

A staggering 67% of consumers have limited understanding of AR and MR. Half of consumers (49%) haven’t used it at all in the past three months. While a third (33%) are aware that AR can be used to gain digital insights while shopping or traveling, nearly a third of consumers haven’t a clue what AR or MR is.

Cr: Amdocs

Those that do are keen to use Apple product or associate Apple with AR/MR experiences, Amdocs reports. More than half (52%) of consumers felt an association with Apple on AR and MR would make them more interested in it, with 38% saying they would be likely to buy an Apple product.

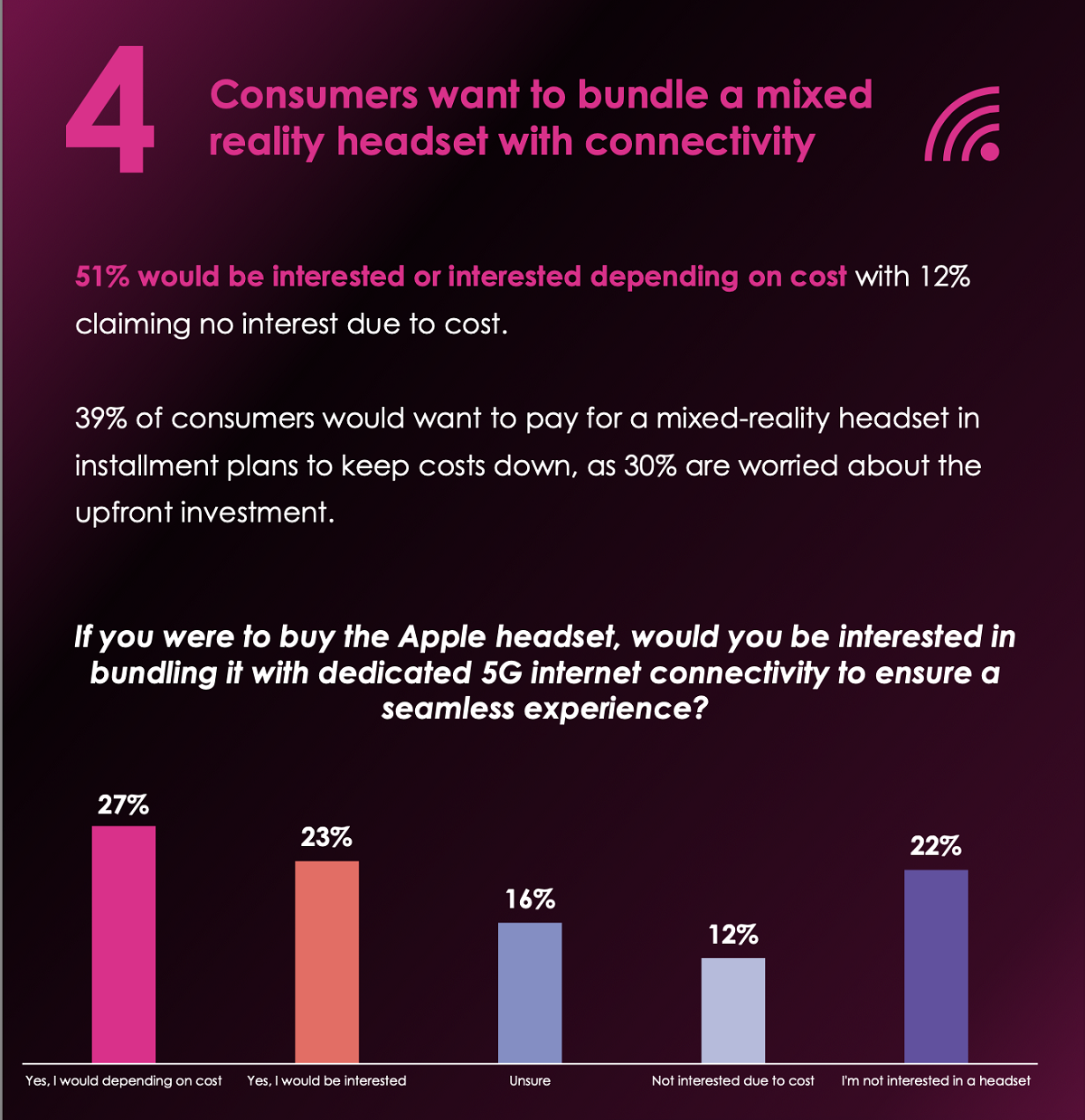

Sixty percent of consumers, according to this report, would prefer to use a mixed reality approach in favor of a full VR metaverse (40%). More than half of users would be interested in trying the new technology, depending on how much it cost.

Cr: Amdocs

Anthony Goonetilleke, group president of technology and head of strategy at Amdocs, added, “These findings uncover several essential factors, first and foremost being the need for better education around what’s possible from AR and MR experiences, as well as preparing networks that can better support in-demand, intensive and seamless experiences. As AR and MR experiences become more widespread, we’ll see the rise of new-found ‘experience bundles’ that capitalize on specific personas, coupling connectivity with entertainment, education, enterprise and more.”

Spatial computing has been adopted by Apple to describe its latest “wearable,” Vision Pro. But there are those wondering if this isn’t the metaverse by another name.

March 28, 2024

Posted

March 28, 2024

Navigating the New Era of Social Commerce: Creator, Organic and Paid Content Strategies

TL;DR

The social commerce landscape has evolved from prioritizing follower counts to valuing the intrinsic quality of content, necessitating a strategic overhaul in social media approaches.

Dash Hudson’s 2024 social media trends report, “The Next Phase of Creator, Organic and Paid,” categorizes content into Creator, Organic, and Paid, each excelling in specific areas — Creator for engagement, Organic for community building, and Paid for extending reach.

Strategically boosting content, especially Reels for impressions and static posts for engagement, significantly enhances brand visibility and audience engagement.

The integration of generative AI across platforms like TikTok, Meta, and YouTube is transforming brand engagement strategies, offering personalized and interactive user experiences.

TikTok Shop is redefining social commerce, combining sales potential with social engagement in a democratized marketplace, underscored by its rapid growth as a major e-commerce player.

A seismic shift has occurred in the ever-evolving landscape of social media, moving us from a world where follower counts reign supreme to one where the content’s intrinsic value dictates its success. This transformation is a complete overhaul of how brands, creators, and marketers approach social media strategy.

Social media management platform Dash Hudson examines this shift in its 2024 social media trends report, “The Next Phase of Creator, Organic and Paid.” The report dissects current trends and offers a roadmap for leveraging the unique strengths of Creator, Organic and Paid content to forge a path to increased engagement and brand growth.

Cr: Dash Hudson

“In recent years, a new set of rules have emerged,” the report notes. “Short-form video has taken over, and there’s been a significant shift from socially-driven to content-driven feeds, as platforms deemphasize follower counts in favor of the popularity of posts.”

At the same time, audiences are becoming increasingly niche in the pursuit of their personal interests. This means that the traditional one-size-fits-all approach content creation is fading into obsolescence, replaced by content that speaks directly to highly specific demographics, maximizing engagement and ROI in the process.

Cr: Dash Hudson

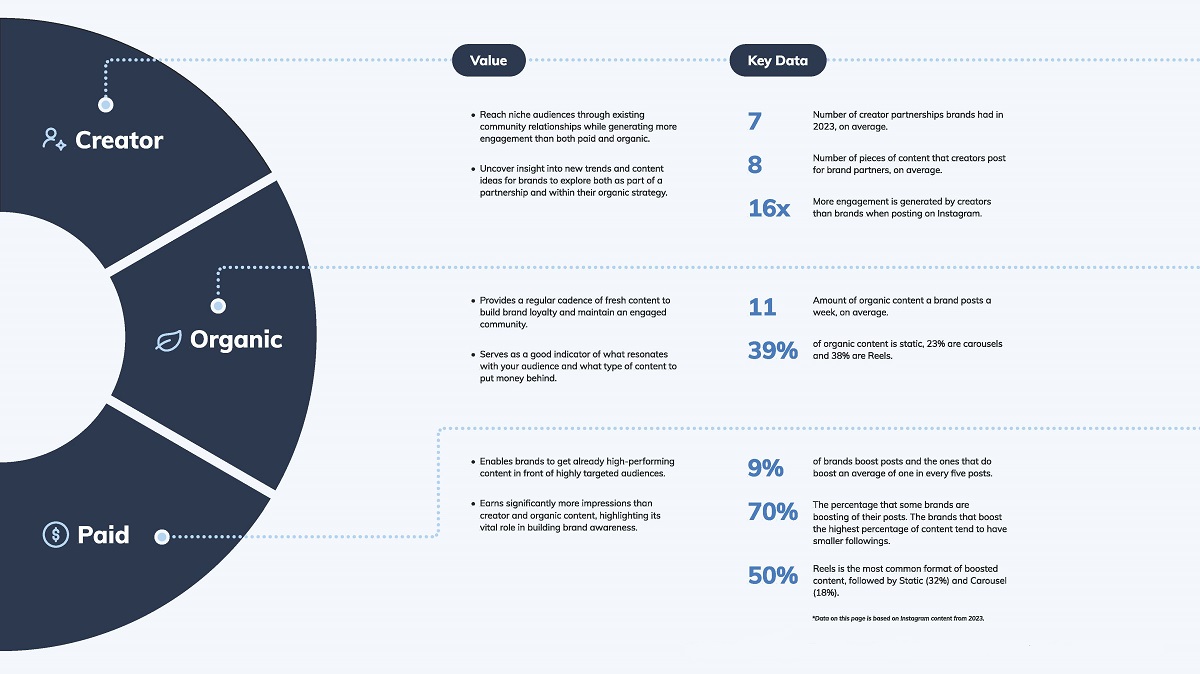

Creator, Organic and Paid Each Excel

The report divides content into three distinct pillars — Creator, Organic, and Paid — and explains how each pillar excels in its domain. Creator content, with its authentic voice, drives engagement; Organic content builds community through genuine interaction; and Paid, or boosted, content extends reach beyond traditional boundaries, ensuring that messages penetrate the noise of crowded feeds.

Creators reach niche audiences through existing community relationships while generating more engagement than both paid and organic. On average, brands had seven creators partnerships in 2023, with most creators posting roughly eight pieces of content for each brand partner, the report found. But, most importantly, content posted by creators generated 16 times more engagement than content posted by brands themselves.

Cr: Dash Hudson

Organic content provides a regular cadence of fresh content to build brand loyalty and maintain an engaged community, serving as a good indicator of what resonates with a given audience. Nearly 40% of organic content is static, while 23% are carousels and 38% are Reels, and brands tend to post an average number of 11 pieces of organic content each week.

Paid, or boosted, content enables brands to get already high-performing content in front of highly targeted audiences. Boosted posts earn significantly more impressions than creator and organic content, highlighting its vital role in building brand awareness. Reels are the most common format of boosted content, at 50%, followed by Static (32%) and Carousel (18%). Around 9% of brands boost an average of one in every five posts, the report found. Some brands are even boosting up to 70% of their posts, but the brands that boost the highest percentage of content tend to have smaller followings.

Each of these pillars, Dash Hudson argues, “is even more impactful when working in concert with the others as part of a holistic social media strategy.”

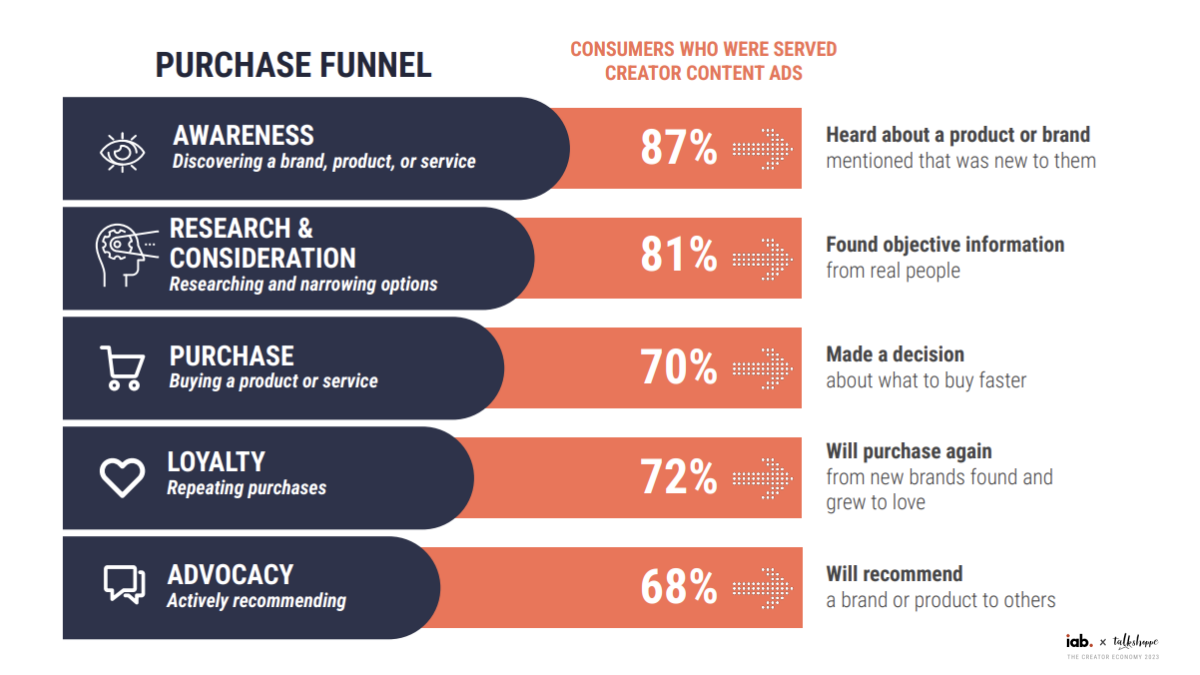

This cross-pollination, the report finds, can drive meaningful results. “IAB tracked over 1,000 consumer purchase journeys, finding that advertising alongside creator content can accelerate the purchase funnel, showing a greater impact on building brand loyalty and a 1.3x greater impact on inspiring brand advocacy.”

A Synergistic Approach

More than ever, a siloed approach to content strategy is a recipe for mediocrity. The Dash Hudson report advocates for a synergistic model where “the interplay between Creator, Organic, and Paid content is not just encouraged but essential.” This holistic strategy amplifies brand presence, weaving a narrative that resonates across all platforms and demographics.

Dash Hudson conducted an analysis on the performance of creator, organic, and paid content across a variety of metrics to discern each content type’s strengths and their most effective roles within the content lifecycle.

Creator content shines in engaging niche audiences and boosting interaction rates, achieving a +34% higher engagement rate than organic content and a staggering +316% higher rate than paid content. This underscores its potency in fostering deep connections and stimulating audience participation.

Organic content, on the other hand, is pivotal in cultivating brand loyalty and nurturing a vibrant community. It outperforms paid content with +358% more comments and +104% more likes, and also surpasses creator content with +53% more comments and +18% more likes, highlighting its value in sustaining active and engaged user interactions.

Paid content is instrumental in expanding brand visibility, delivering three times more impressions and six times more video views than organic content, irrespective of the investment size. When compared to creator content, paid content generates seven times more impressions and video views, showcasing its unparalleled capacity to broaden reach and attract new audiences.

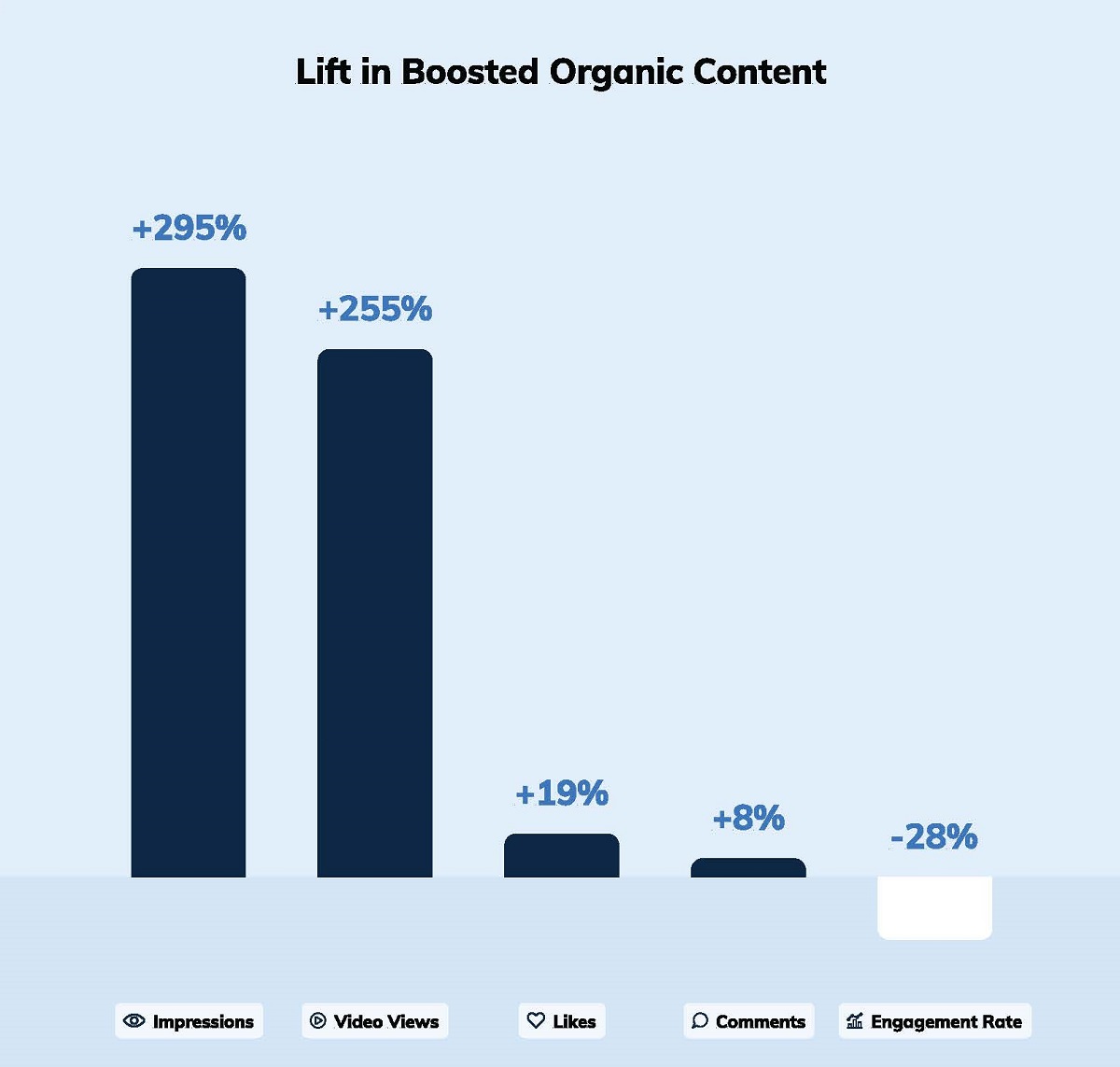

The power of paid content cannot be overstated. The report highlights how “strategically boosting content — particularly Reels for impressions and static posts for engagement — can significantly elevate a brand’s visibility.” Moreover, “entertaining content, when boosted, sees exponential gains,” underscoring the importance of not just what you share, but how it captivates your audience.

Cr: Dash Hudson

Overall, boosting content builds brand awareness, “breaking through the algorithms to place your brand directly in front of the eyes that matter most.”

Boosting Reels grows impressions, and boosting static content grows engagement rate — “the metrics each format craves, tailored to maximize the inherent strengths of each content type.”

Boosting entertaining content drives much higher performance across the board, proving that “entertainment is not just king but the ace in the deck for social media strategy.”

Leveraging AI for Content Optimization

Dash Hudson outlines significant trends and developments in social media platforms themselves driven by new technologies and changing user behaviors. The report highlights three key shifts: the integration of generative AI into platform experiences, the resurgence of social commerce with a focus on TikTok, and the growth of direct messaging as a crucial engagement tool. It notes that 64% of marketers currently utilize AI, recognizing its value and planning continued investment.

Specific AI enhancements across platforms are transforming how brands engage with audiences, Dash Hudson finds. TikTok has introduced an AI-powered “Creative Assistant” designed to aid in campaign creation, complemented by custom AI Chatbot Creation tools developed by its owner, Bytedance.

Meanwhile, Meta is unveiling generative AI tools that facilitate video and photo creation/editing from text prompts, alongside expanding AI chat personas to include celebrities like Kendall Jenner and Tom Brady, and is exploring new chatbot creation tools. This is part of Meta’s broader strategy to integrate AI across its advertising products.

Instagram is in the process of testing generative AI features, including custom sticker creation and visual editing tools for uploaded content. YouTube has launched “Dream Track,” an experimental generative AI tool that enables users to create music in the style of various famous artists.

These advancements underscore a significant shift towards more interactive and personalized user experiences, offering brands novel ways to capture attention and stay ahead in the ever-evolving social media landscape.

TikTok Shop: Winner Takes Alland Anyone Can Win

In the dynamic realm of social commerce, TikTok Shop emerges as a groundbreaking platform, blending the immense potential for sales with the power of social engagement. The Dash Hudson report illuminates this platform as “a democratized marketplace where authenticity and entertainment are paramount for direct sales success.”

A standout revelation from the report is TikTok Shop’s meteoric rise in the e-commerce domain, “ranking as the 12th largest e-commerce retailer in the US market and the 5th largest in the UK market in 2023.” This rapid ascent highlights TikTok Shop’s substantial impact and its capability to captivate both users and brands, solidifying its position as a formidable force in e-commerce.

Insights into consumer behavior reveal how TikTok Shop’s unique integration of shoppable videos and livestreams significantly influences purchasing decisions. The platform’s innovative approach to social commerce sales, supported by detailed audience buying behaviors and sales metrics, offers brands a clear blueprint for engaging potential customers effectively.

Technological innovations within TikTok Shop, such as AI-driven personalization and AR features for virtual try-ons, are enhancing the shopping experience, making it more interactive and personalized. These advancements are pivotal in attracting and retaining users, offering them a seamless and engaging shopping journey.

Looking ahead, the report provides a glimpse into the future of TikTok Shop and the broader landscape of social commerce. As we navigate this new era of social media, the fusion of creativity, strategy, and technology becomes increasingly crucial. This report not only sheds light on the current trends and strategies but also offers a glimpse into the future of social media marketing — a future where engaging content, powered by sophisticated AI tools and platforms like TikTok, leads the way.

Exclusive Insights: Get editorial roundups of the cutting-edge content that matters most.

Behind-the-Scenes Access: Peek behind the curtain with in-depth Q&As featuring industry experts and thought leaders.

Unparalleled Access: NAB Amplify is your digital hub for technology, trends, and insights unavailable anywhere else.

Join a community of professionals who are as passionate about the future of film, television, and digital storytelling as you are. Subscribe to The Angle today!

Driven by creator-led content, social commerce stands out as one of the most significant trends for marketers to watch out for in 2024.

March 26, 2024

The Fragmentation Situation: What Do Today’s Streaming Audiences Want?

TL;DR

SVOD price hikes may be approaching their peak: Consumers will likely balance costs and content with ad-supported tiers, contracts, and more bundles, but these may be short-term solutions to preserving profitability for streamers.

Social media and unbundling pay TV have trained consumers to expect more customized and personalized content and advertising. Deloitte suggest these are levers to build greater consumer engagement and value.

Thebiggest challenge for SVOD providers and studios is that they are no longer addressing a mass culture, but a fragmented landscape of competing digital entertainment options.

More evidence if it were needed that the video streaming model is shape-shifting under its own weight forcing players to adapt a much more sophisticated approach to market.

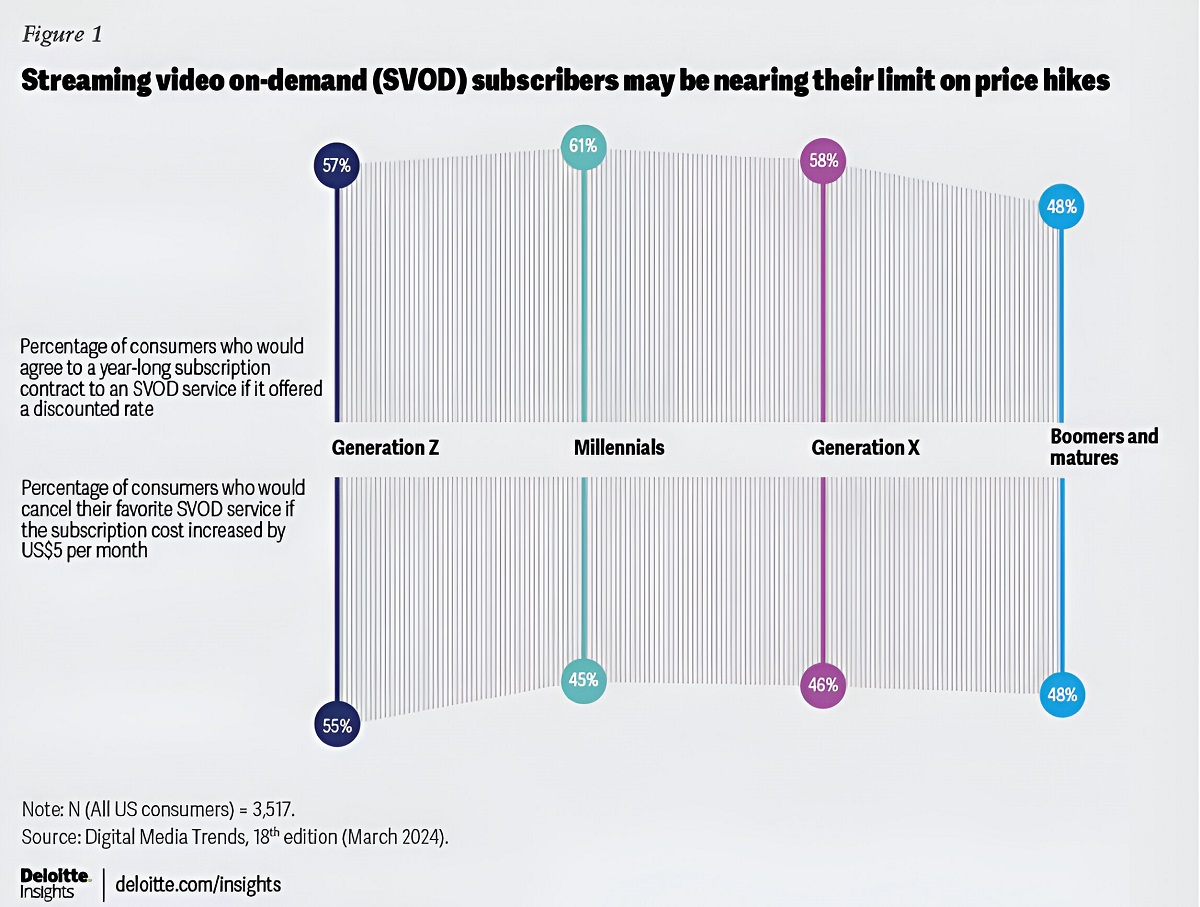

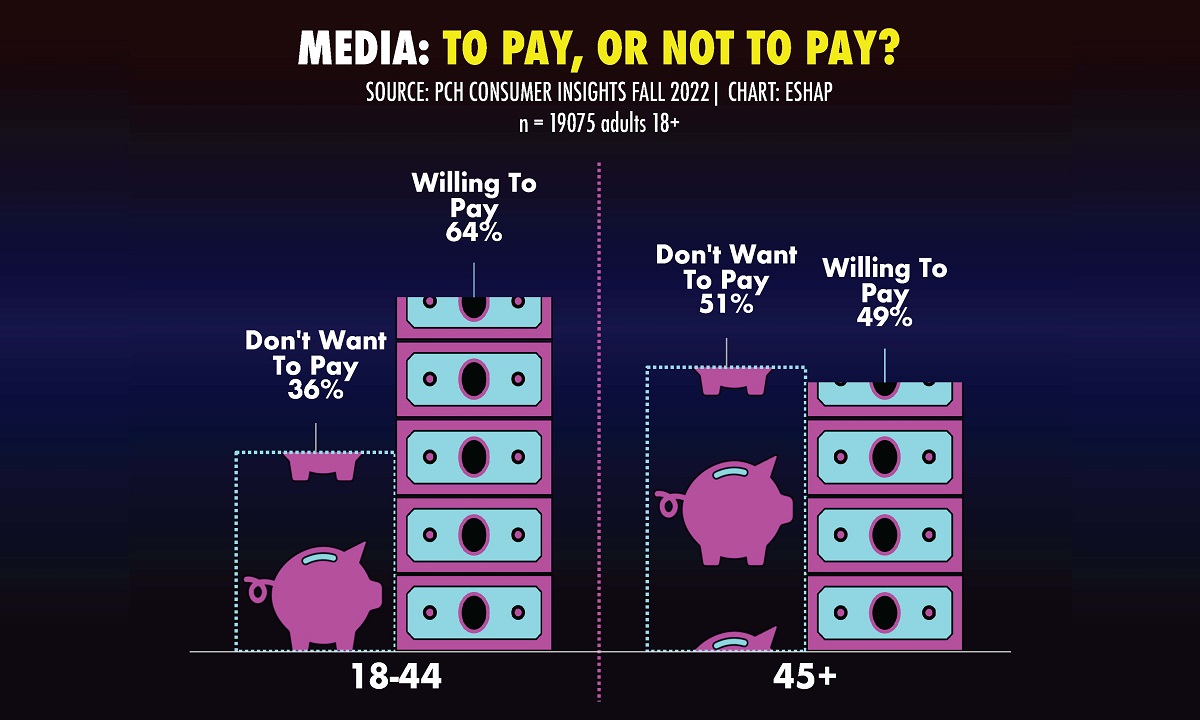

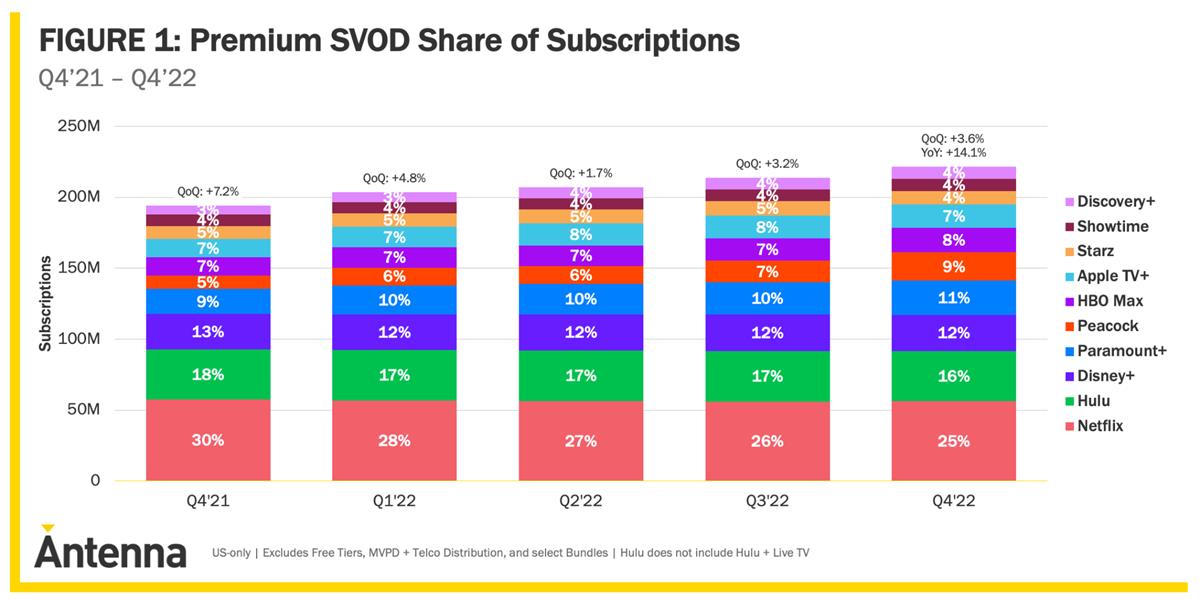

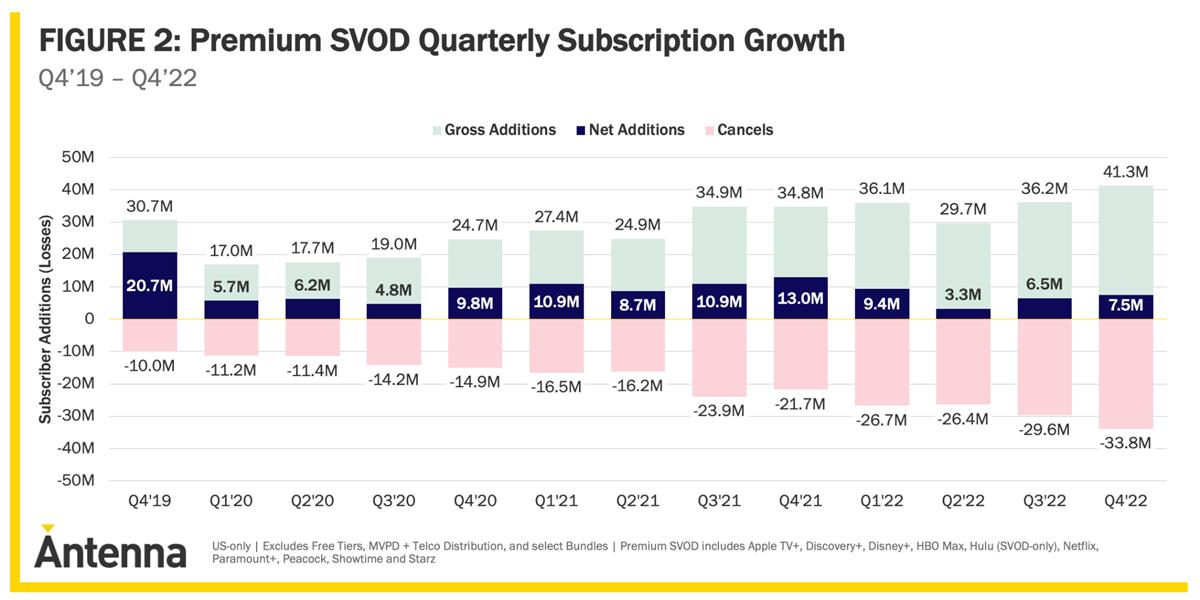

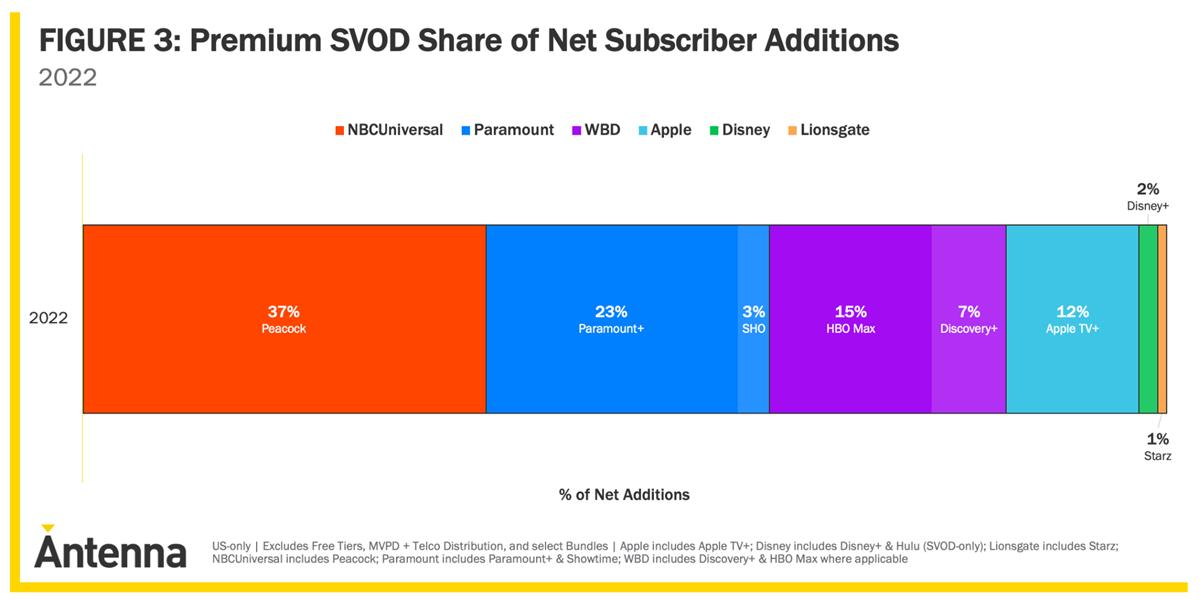

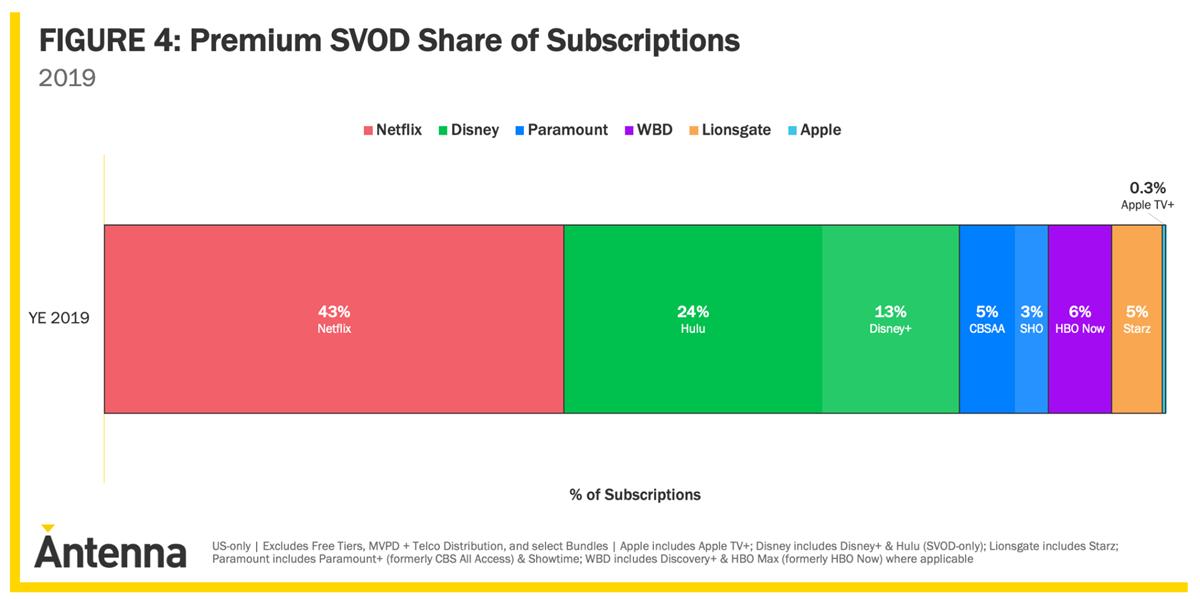

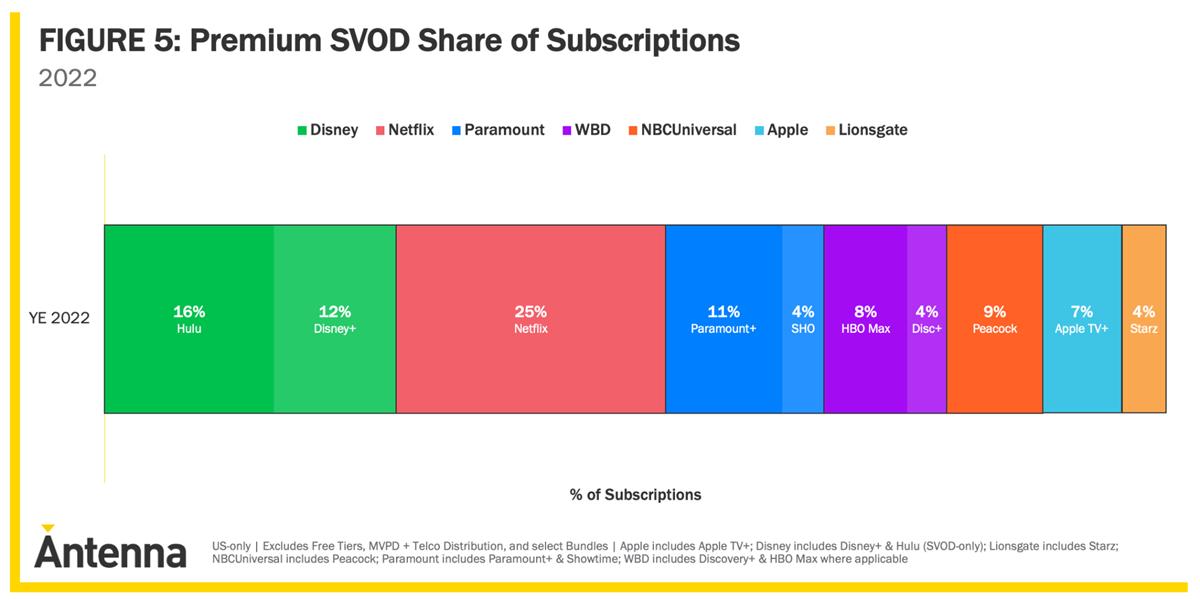

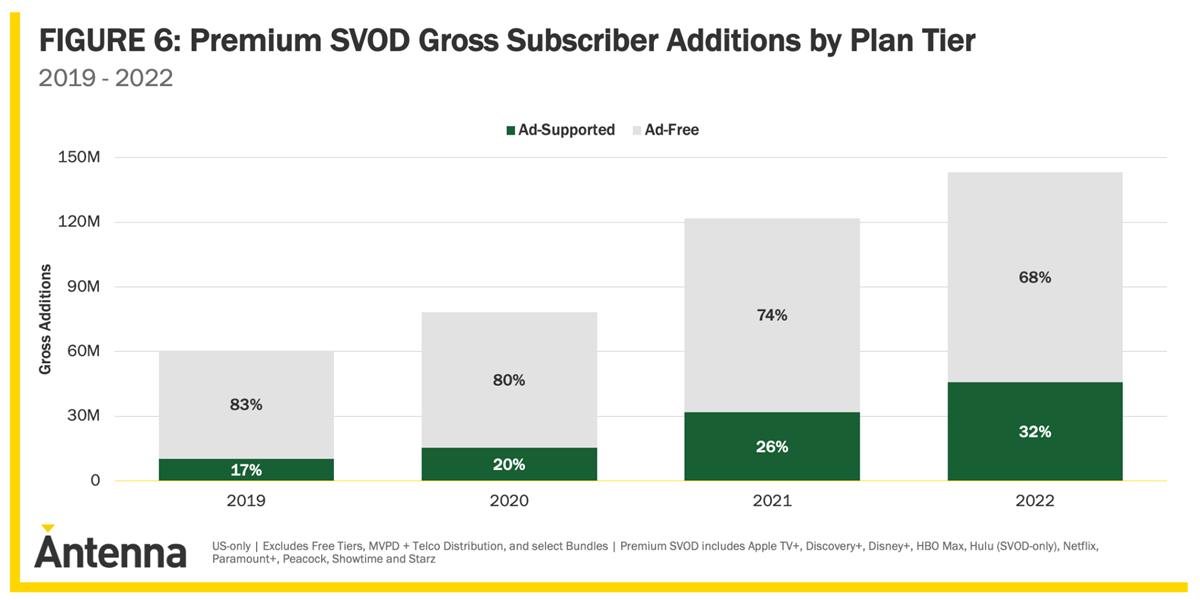

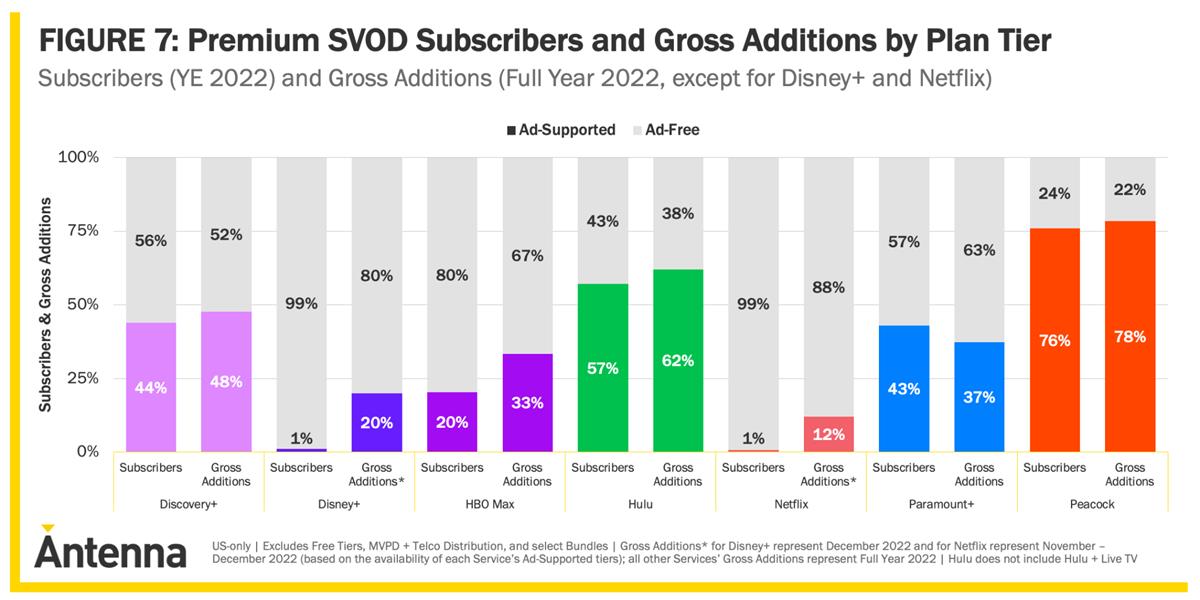

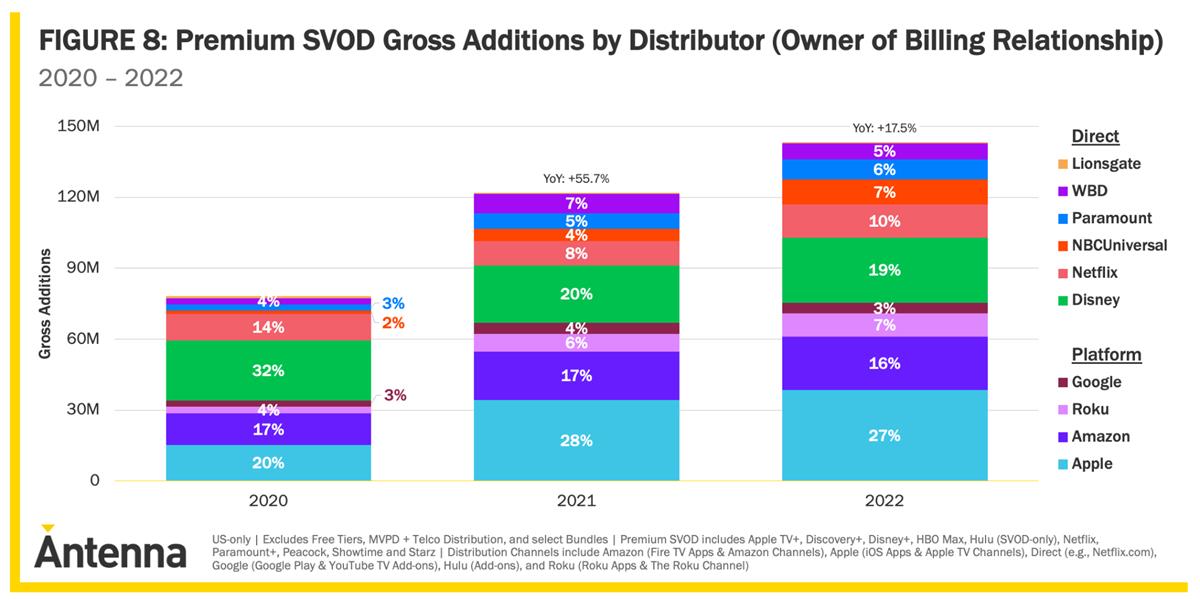

In its analysis from November 2023, Omdia found the number of SVOD services per home has declined in a number of markets for the first time. Market analyst Antenna in its latest “State of Subscriptions” report also finds that subscriber growth among Premium SVODs slowed last year to 10%. Deloitte in its “2024 Digital Media Trends” report found more than a third of Americans no longer think subscription VOD is worth the price they are paying.

On average, Deloitte says, US households spend $61 per month on streaming services. That’s a 27% increase over last year’s average of $48 per month. And streaming services might want to think twice before increasing prices further, as nearly half (48%) of the people Deloitte spoke with said they would cancel their streaming service — even their favorite one — if prices went up by $5 per month or more.

Cr: Deloitte

“With 36% of Americans surveyed believing content on SVOD isn’t worth the money, providers shouldn’t assume that advertising, bundles, and contracts are enough to help their business,” said Deloitte.

Its survey data shows that US consumers are questioning the value of streaming media while also declaring their unwillingness to ever pay for social media.

“This is a generational shift,” the report stated. With some eldest millennials in their 40s, “it’s no longer merely ‘younger generations’ who are giving their time equally to TV and movies, social media and user-generated content, and immersive and social gaming.”

Cancellations are already a problem for the industry, notes Chris Morris, analyzing the Deloitte report at Fast Company. Deloitte reports that 40% of consumers have cancelled a streaming service in the past six months.

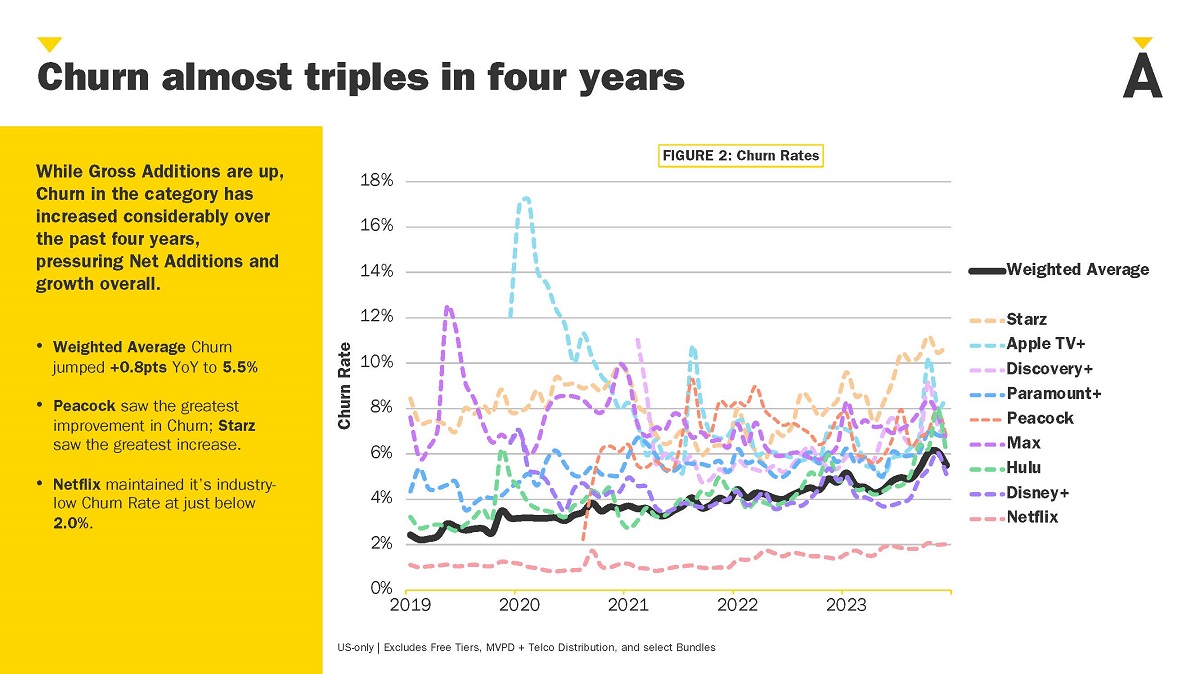

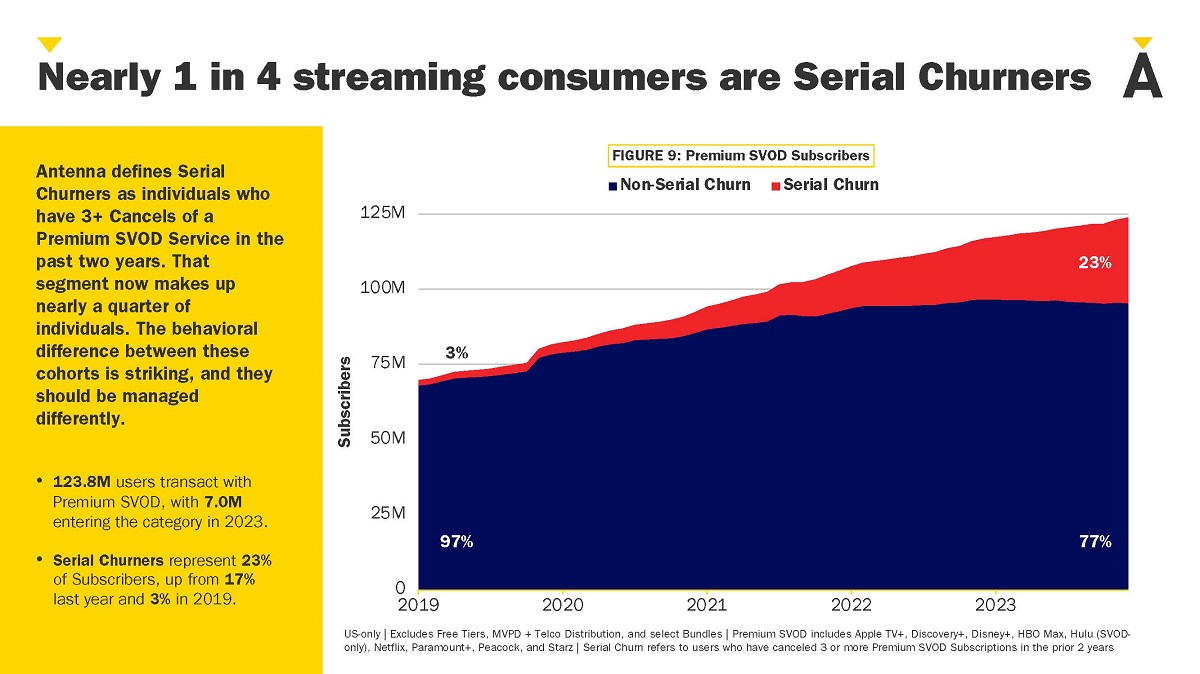

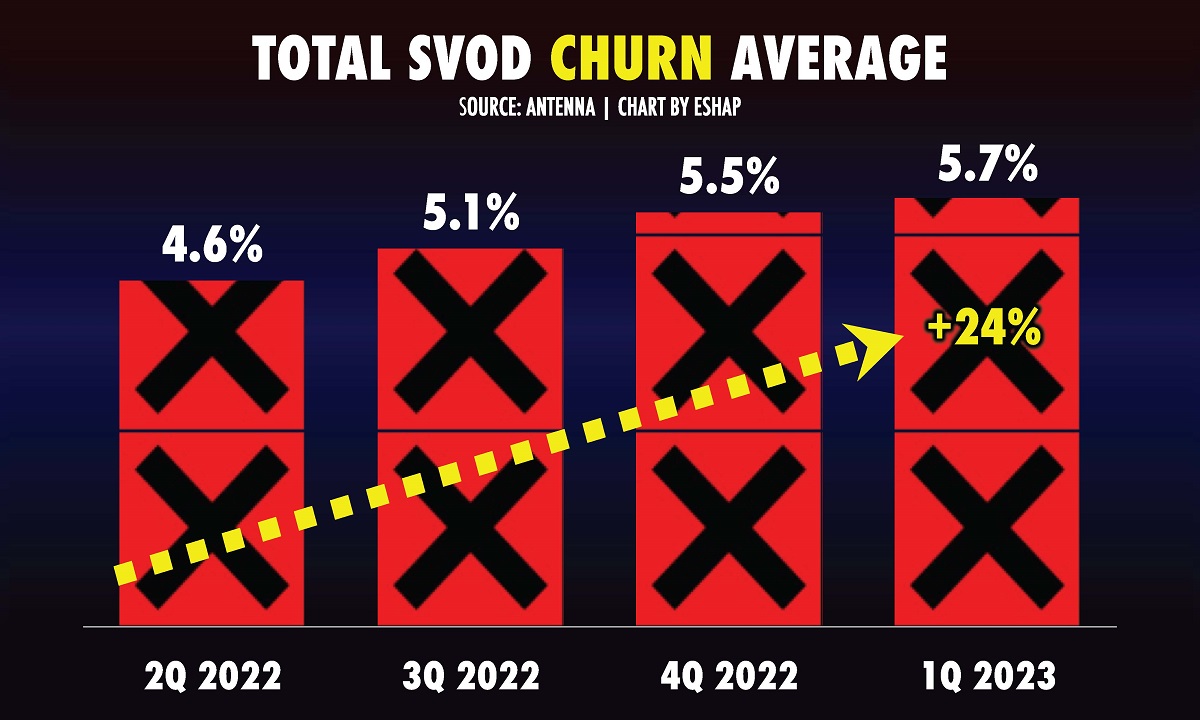

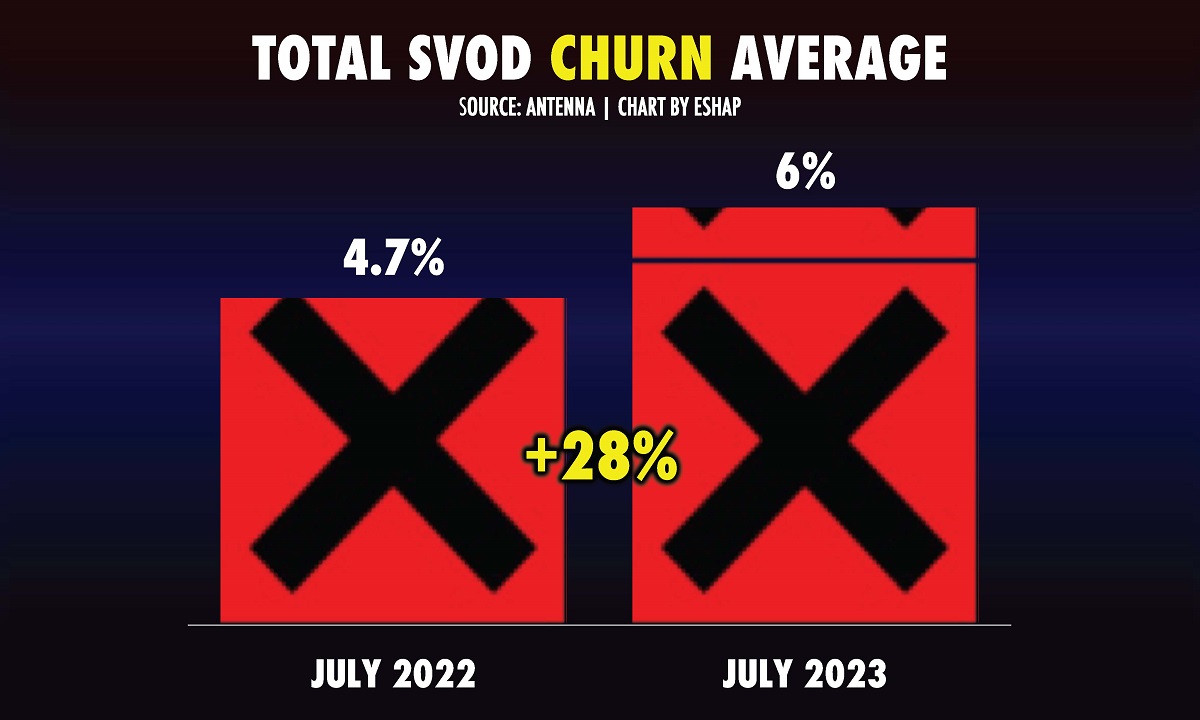

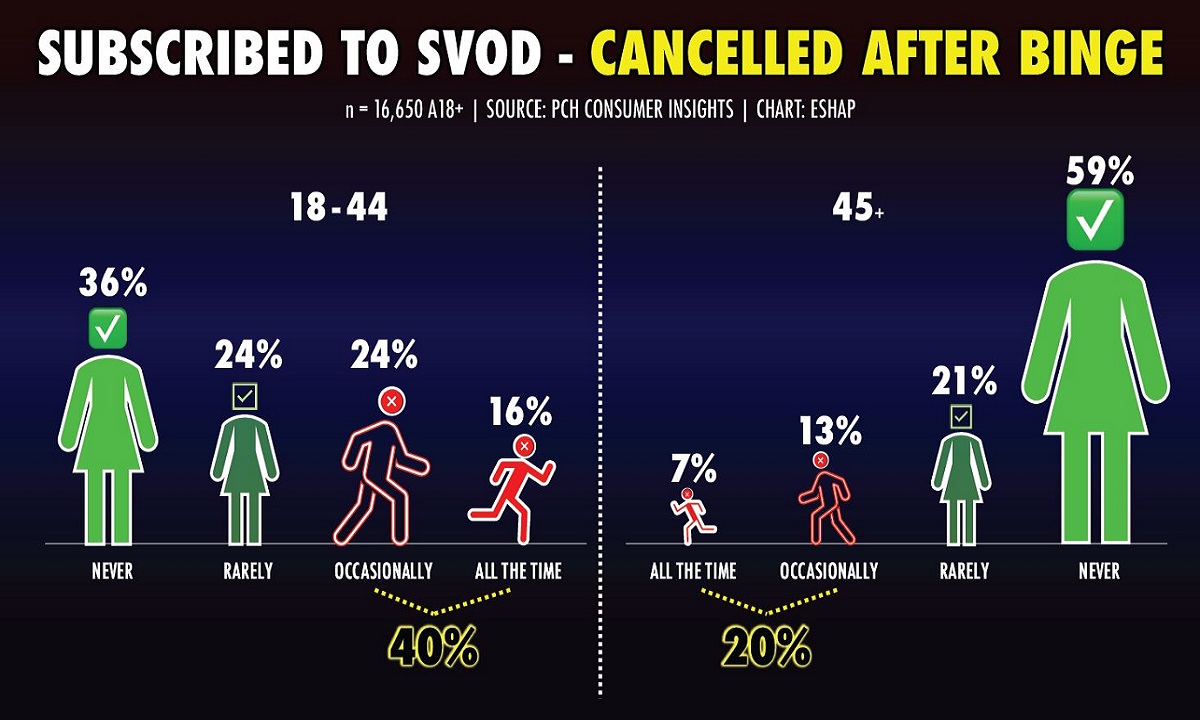

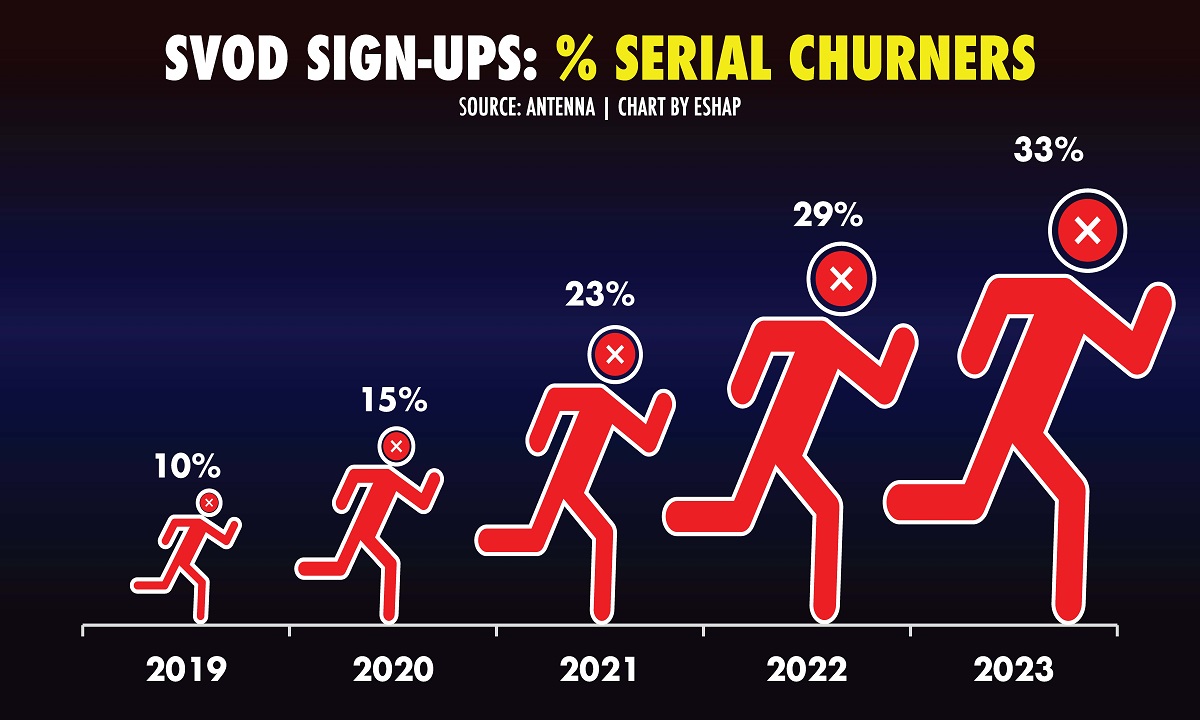

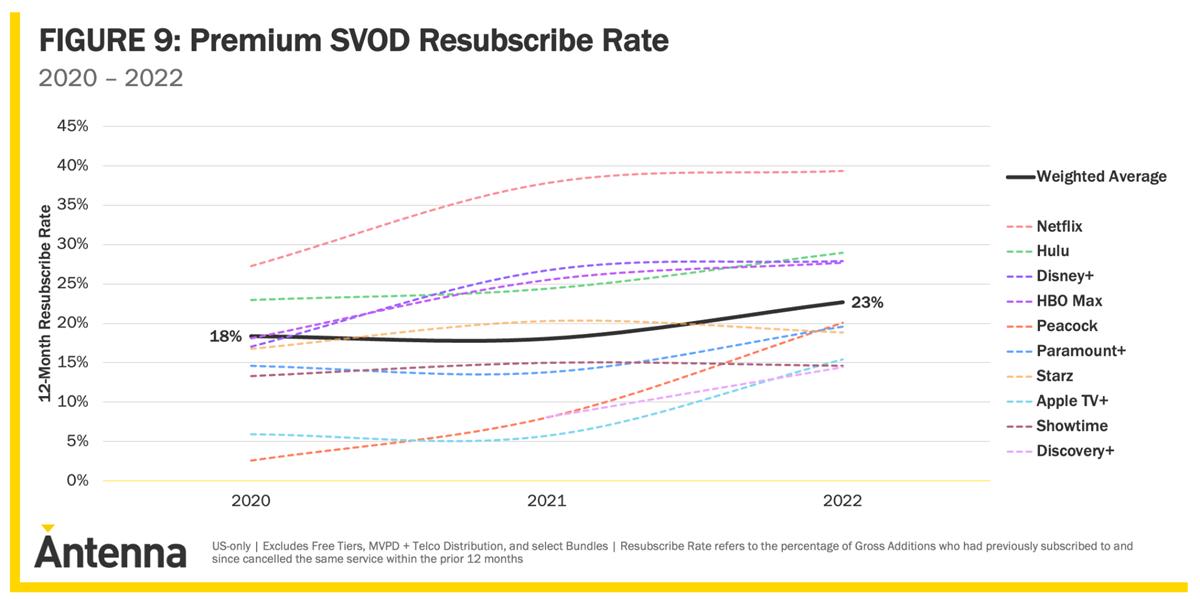

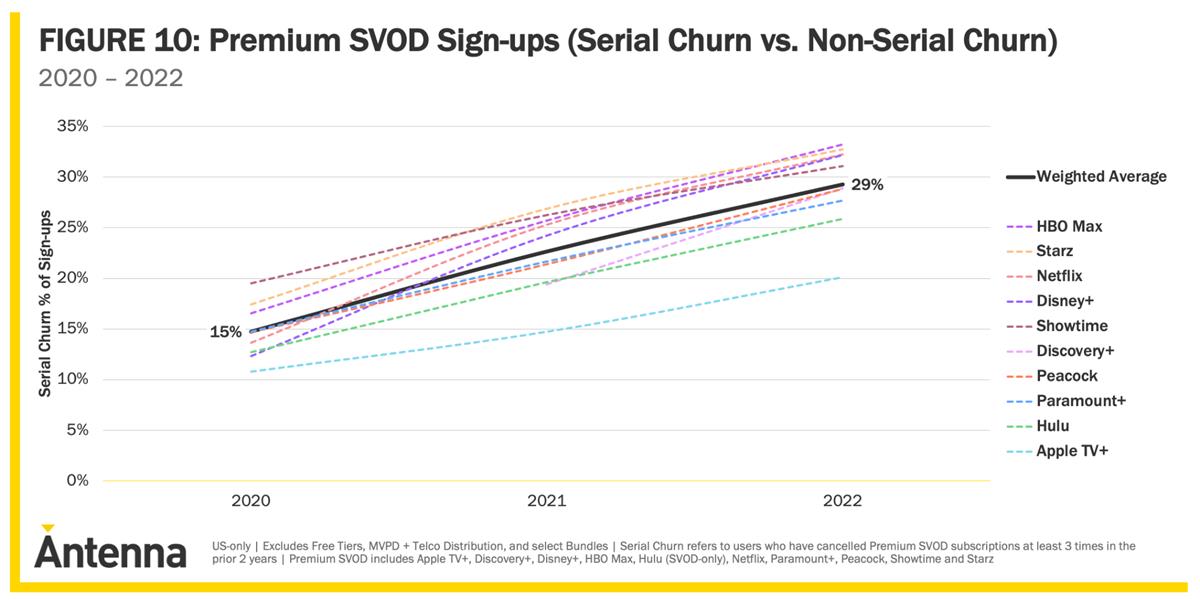

Antenna found that churn had tripled in the last four years, pressuring net additions and growth overall. It also identified a category of “Serial Churners” — individuals who have three or more cancellations of a premium SVOD service in the past two years. That segment now comprises nearly a quarter of users.

Cr: Antenna

Cr: Antenna

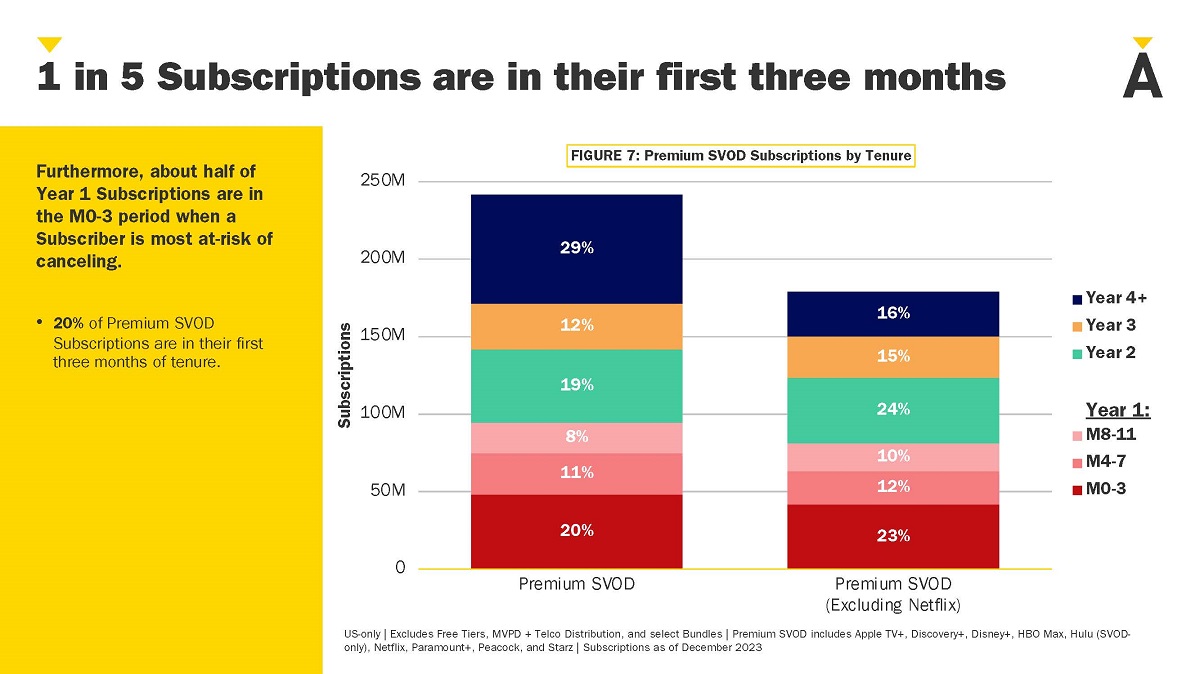

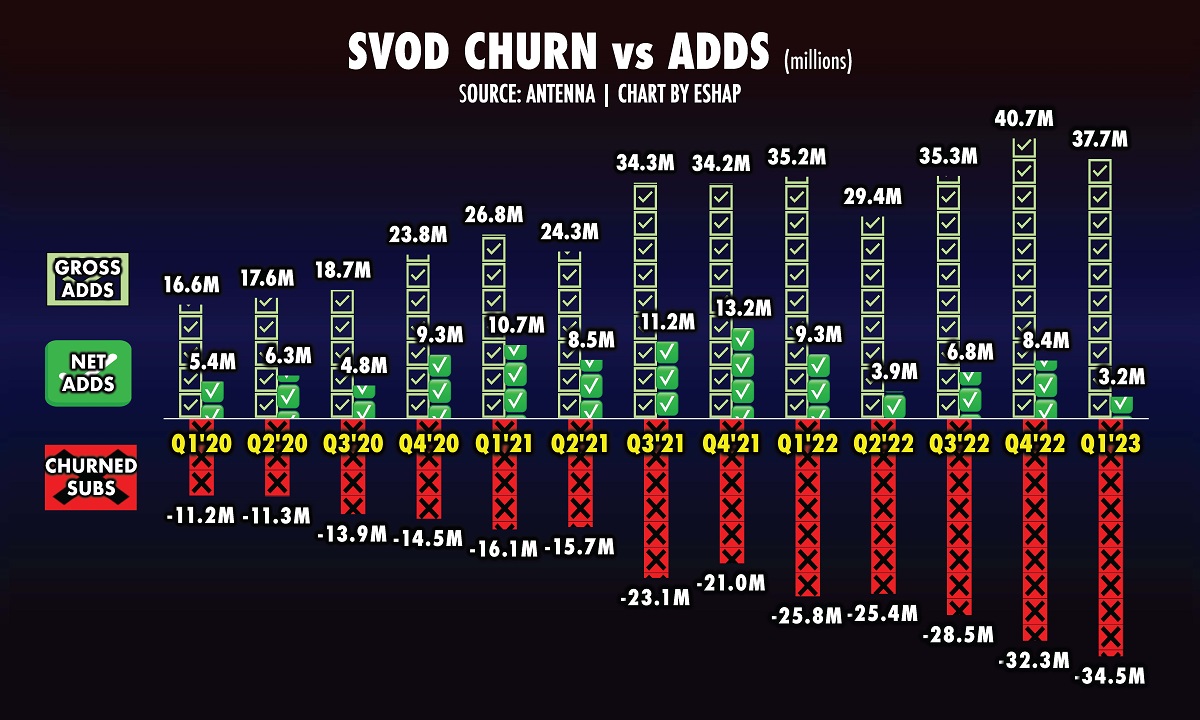

Antenna attributes the overall increase in churn to the surge in mergers and acquisitions among the major streamers since 2019. Almost half of Premium SVOD Subscriptions (excluding Netflix) are in their first year of tenure, it notes.

Cr: Antenna

Cr: Antenna

On the plus side, 10% of cancellations resubscribe the next month, and one in three are back by six months after cancelling.

Cr: Antenna

Antenna concludes that if the previous stage of the streamer business model was focused on acquisition to amass scale, the next stage necessitates a shift to managing their subscribers.

“This will translate to much more sophisticated marketing and product strategies, new success KPIs, and a whole lot more reliance on data,” says Antenna, which of course can deliver all of this.

Part of the problem is that viewer’s time is being more and more fragmented away from TV, away from streaming TV and onto social media sites and video games.

“The biggest challenge for SVOD providers and studios may be that they are no longer addressing a mass culture, but rather a fragmented landscape of competing digital entertainment options,” Deloitte execs state. “Trying to rebuild pay TV business models around streaming services could help reduce SVOD churn and slow attrition in the near term, but the long game for success will likely involve reinventing the medium to be more personalized, more shoppable, and more social.”

Providers will also likely need to widen their scope beyond TV and films to reach modern audiences, it suggests, and make their IP work across social and video games.

“The industry has had 20 years to understand the size and shape of the streaming disruption. Now they should come together to work to build something truly contemporary.”

This would include partnering with social media creators and influencers to facilitate “discovery, hype, and trust,” and using generative AI to improve the quality of content creation. However, Deloitte warns that this could also “lead to a flood of cheap and novel content that further dissolves the boundaries between ‘real’ and synthetic, commodity and premium.”

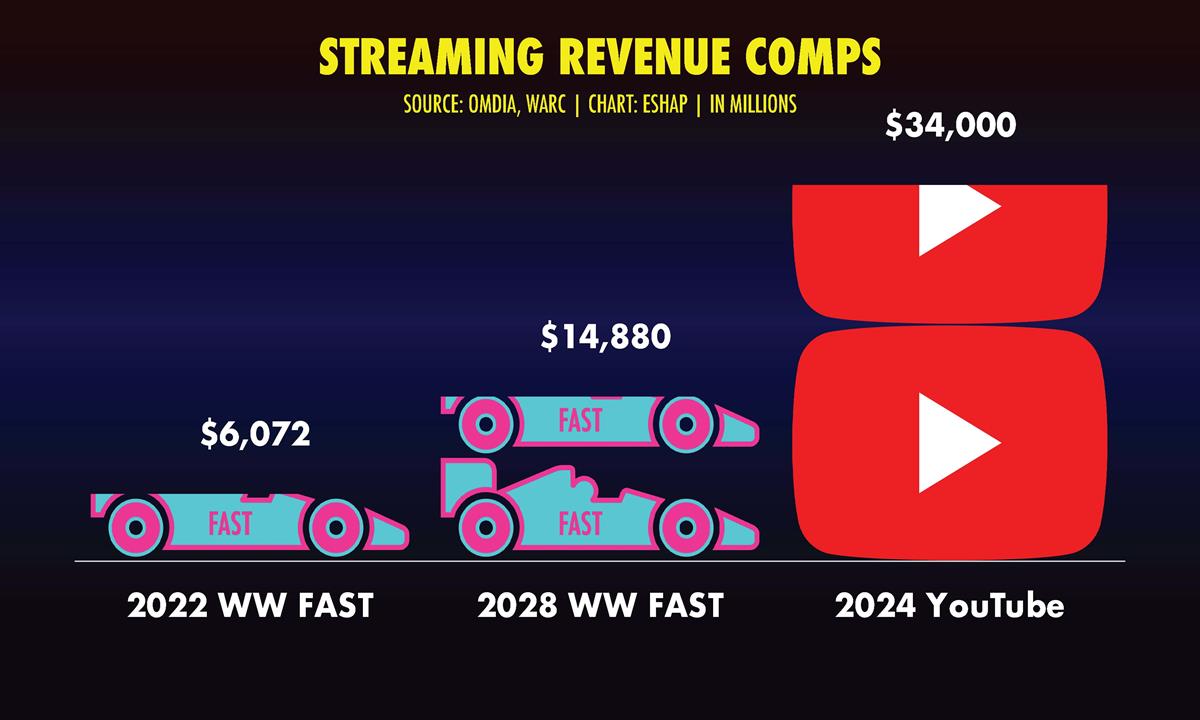

Simultaneously, free video stacking is still on the rise. YouTube’s continued growth as the top video service provider in key markets, is charted by Omdia. Strong growth in other social video platforms and Free ad-supported television (FAST) services sees free as the major streaming strategy that all major SVOD services are leaning into.

Also in Europe, the legacy of public service broadcasting remains strong, with traditional free TV and broadcaster video on demand (BVOD) services in high demand.

“The allure of social media platforms such as TikTok and Instagram Reels has reshaped how individuals consume video content,” says Omdia analyst Maria Rua Aguete. “The appetite for free content is ever-increasing and the major streamers are clearly leaning into this as a strategy. With engaging formats and vast user bases, social media services offer compelling alternatives to mainstream streaming services.”

Exclusive Insights: Get editorial roundups of the cutting-edge content that matters most.

Behind-the-Scenes Access: Peek behind the curtain with in-depth Q&As featuring industry experts and thought leaders.

Unparalleled Access: NAB Amplify is your digital hub for technology, trends, and insights unavailable anywhere else.

Join a community of professionals who are as passionate about the future of film, television, and digital storytelling as you are. Subscribe to The Angle today!

Available now to download, “A Beginner’s Guide to FAST” will be presented at NAB Show by GRG Global’s VP of Media Research, Gavin Bridge.

March 25, 2024

Posted

March 19, 2024

Research: Tracing the FAST Trajectory

TL;DR

FAST is still an emerging industry, but all signs point to it being one that will remain part of the entertainment diet for the future.

The number of FAST channels in the US has skyrocketed to nearly 2,000 with no signs of slowing down, finds a new report from researcher CRG Global.

Forty percent of US adults regularly watch FAST and that figure is rising, making it an important part of the country’s media mix.

Gavin Bridge, VP of Media Research at CRG Global, will reveal the latest research and all you need to know about planning a FAST future at NAB Show 2024.Register here with the code AMP05 to attend.

Media execs know that Free Ad-Supported Streaming TV is a revenue generator — until they don’t. There’s a lot going on under the hood of linearly-scheduled, advertising-funded streamed channels. If you want to understand how to make the most of the opportunity, then a new report from CRG Global, in partnership with NAB Amplify, is your ticket to the inside track.

The session will explore the current state and future trends of free ad-supported streaming TV (FAST), a rapidly growing segment of the OTT market, and joining Bridge will be: Bethany Atchison, Vice President of Distribution Partnerships at VEVO; Michael Hyon Johnson, Director of Operations for ElectricNOW; and Michael Senzon, President of Digital for Allen Media Group (AMG).

The speakers will examine how, In a rapidly evolving media landscape, traditional television is being overshadowed by innovative streaming solutions.

FAST is one of these innovations, and has surprised many with its rapid growth in the last few years. This session with leading executives from the FAST space will examine the opportunities and challenges of running a FAST channel, such as content curation, personalization, discovery, loyalty, optimization, localization, and monetization.

The panel will also discuss the role and responsibility of platforms and publishers in delivering value to viewers and advertisers, and in fostering a healthy and diverse FAST ecosystem.

By the Numbers

The end result for attendees will be a greater understanding of what FAST is and, if not yet a participant, provide insights as to why FAST could be part of your media strategy.

CRG’s research peels back the layers on FAST, revealing not just its current state but also its trajectory in the Media & Entertainment industry.

For a start, about 40% of US adults regularly watch FAST and that figure is rising, making FAST a very important part of the country’s media mix, the report finds.

Cr: CRG Global/NAB Show

Researcher CRG Global also reports that just under half of FAST viewers (48%) watch daily, with a further 39% watching a couple of times a week.

It’s for that reason that many non-traditional video operators include a FAST service within their portfolio. That includes the Disney, Fox and NBCU, as well as Dish, Charter and Comcast, Amazon and even Google TV and TV set manufacturers like Samsung. FAST is the reason Walmart acquired Vizio.

Taking a deep dive into FASTonomics, the report outlines what FAST both is and isn’t. There are competing predictions for growth in 2024, it finds. Omdia suggests the FAST market in the US will hit $7.4 billion this year, and S&P Global’s Kagan estimates it to be $6.2 billion, while CRG Global reckons it to be nearer to $5.1 billion due to the weaker ad market.

Yet FAST remains shrouded in secrecy, the report notes. Not one service publishes domestic users anymore — Paramount used to do so for Pluto TV, but ceased during the pandemic.

Cr: CRG Global/NAB Show

Instead the industry has to rely on external analysts to assess the market and put a value on it, which can be confusing given the blurred definition of the FAST business model.

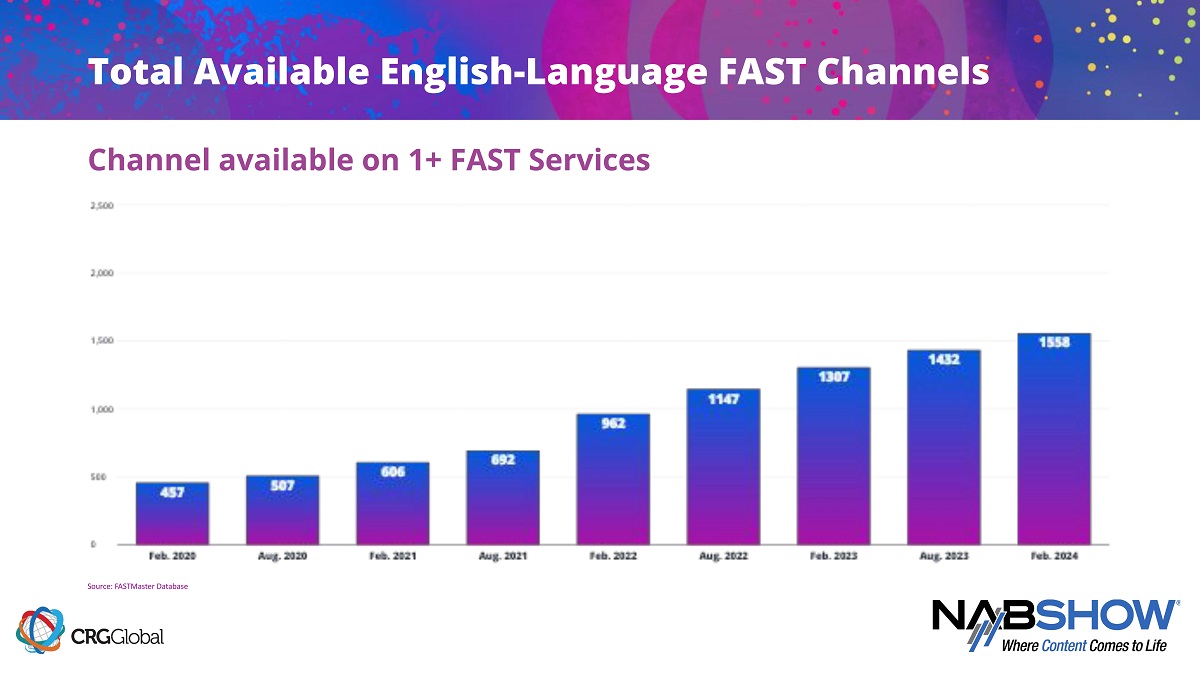

What is not in doubt is that the number of FAST channels has grown considerably since 2020 from 489 distinct channels available across major services to nearly 2,000 at February 2024.

When NBCU announced last June that it would be making close to 50 FAST channels available for licensing, it marked a new point in FAST history. The scale of the launch was unprecedented and yet is just the tip of the content iceberg that many media firms have at their disposal.

What’s Seen on the Screens

The report also details the type of audience that watched FAST, showing that while pay TV still provides utility to many, FAST is filling a need for many that cable is not.

Cr: CRG Global/NAB Show

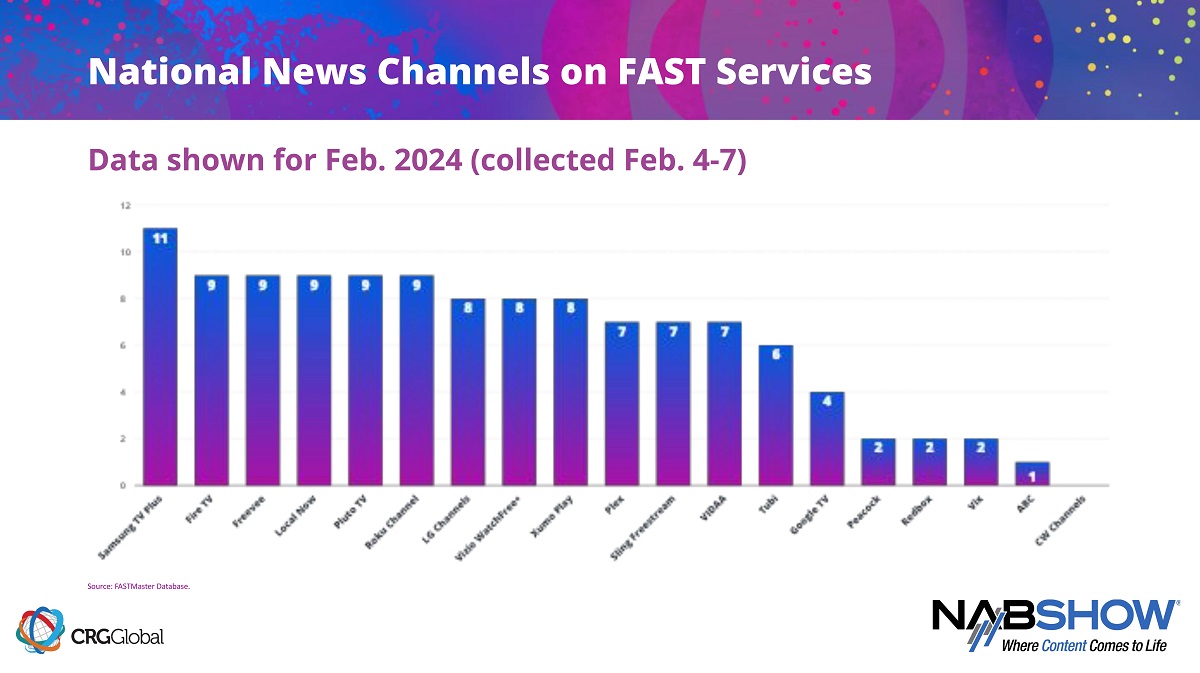

“If a time-traveling FAST executive from the start of 2020 suddenly found themselves in 2024, one of the chief elements that would shock them — aside from the total number of available channels — would be how news has embraced FAST,” says Bridges. “It is the explosion of local news that would attract the most attention.”

Four years ago, there were three local news stations available on key FAST services. That figure is now 231, with Scripps, Cox Media Group and Hearst embracing distribution across a number of major services.

“The extensive local offering helping cord-cutters stay in touch with their communities and allow for local stations to reach the greatest possible audience,” the report finds.

FAST is still an emerging industry. But all signs point to it being one that will remain part of the entertainment diet for the future.

Exclusive Insights: Get editorial roundups of the cutting-edge content that matters most.

Behind-the-Scenes Access: Peek behind the curtain with in-depth Q&As featuring industry experts and thought leaders.

Unparalleled Access: NAB Amplify is your digital hub for technology, trends, and insights unavailable anywhere else.

Join a community of professionals who are as passionate about the future of film, television, and digital storytelling as you are. Subscribe to The Angle today!

Alan Wolk, Co-Founder/Lead Analyst at TVREV, will be moderating the NAB Show session “The Future of FAST: Lessons Learned and What’s Next,” Tuesday, April 16 at 3 p.m.

March 17, 2024

Posted

March 16, 2024

NAB Show Amplified: How Audio Entertainment Is Evolving, Expanding, Immersing

TL;DR

Jackie Levine, head of Television and Film at Audible shares her thoughts on evolving trends in audio entertainment.

Jackie Levine, head of Television and Film at Audible, will appear on the The Great Reset: Future of Podcasting from Hollywood and Beyond session on Monday, April 15, at 1:30 p.m. Moderated by eMarketer’s Jasmine Enberg, this panel will also feature Paramount Global EVP of Podcasting and Audio Steve Raizes and SiriusXM SVP of Comedy & Entertainment Radio and Podcasts Adam Sachs.

Jackie Levine, Head of Television and Film, Audible

What excites you about your position at Audible as it relates to the future of this industry?

Jackie Levine: With the explosion of audio in the entertainment world, I’m excited about the exchange of ideas between audio, TV and film.

My initiatives at Audible give fans the opportunity not just to listen to, but also see original and classic stories come to life in new ways. We’ve become a destination for creators to expand their stories in so many ways and create franchises that start in audio.

What are the biggest trends impacting the community/industry right now Finding and originating breakthrough content with the vast number of great shows, movies, and podcasts at our consumer’s fingertips. Socially relevant, high-concept (and/or based on IP) content is currently trending.

What challenges does the community need to overcome because of these trends? We need to continue to strive to find high-concept projects and ideas to embrace the needs/desires of the consumer and make the highest quality material possible. How can we entertain AND make it meaningful? Some of what is performing well right now in-marketplace is a way to escape, for hopeful outcomes, and wins.

What’s one thing you wish more media pros knew about? I wish more media professionals would prioritize quality writers to trust they will deliver. There are so many steps and assurances needed as the media business becomes more and more condensed, which can result in selection decisions to be more fear-based.

Encouraging experienced writers and producers to do what they are great at without second guessing them could help all of us to successfully create more commercial and quality material.

As we approach NAB Show, OTT advertising is on the industry’s mind like never before. Nearly all the major broadcasters and streaming providers have embraced some form of advertising to increase ARPU and move to business models that are sustainable over the long term.

Server-side ad insertion (SSAI) is the central cog in OTT advertising because it joins streaming technology with adtech. Any issues with the SSAI and valuable advertising revenue is lost. On the other hand, SSAI has the ability to transform advertising revenues and empower providers to compete on the digital stage.

The key to maximising SSAI revenues is to allow broadcasters/customers to create an ad product that boosts the traditional benefits of TV by adding the modern benefits of digital advertising.

TV’s traditional benefits

Mass reach: Nothing offers mass reach in a short period of time like TV. It also has the ability to drive discussion and get in the public psyche – it creates “water cooler” moments that are increasingly hard for advertisers to find elsewhere.

Quality of delivery: Nowhere else can advertisers get a broadcast-quality 15-30-second ad with such high engagement and view-through rates.

Digital advertising benefits

Addressability: In the digital realm, advertisers expect addressability. Broadcasters and streaming providers must convince brands to increase spend on TV rather than YouTube or TikTok – which both offer fantastic targeting.

Programmatic: There is great potential to increase fill-rates by adopting programmatic. It helps secure the highest possible CPM for each available ad spot.

Measurement: Real-time measurement of ad views is essential for advertisers to tweak and improve their campaigns. It’s what they do across other digital channels so they want to do the same with OTT.

SSAI has the power to deliver an appealing blend of both worlds: the mass reach and viewer experience of TV and the advanced advertising benefits of digital.

Implementing SSAI to unlock the full value of OTT advertising can be complex. Here are the key considerations for broadcasters and streaming providers to enhance their advertising offerings and grow revenues:

Scale and Reliability

TV’s mass reach creates valuable water-cooler moments that advertisers are increasingly struggling to find elsewhere.

Live streaming and major sports have mass appeal and are therefore highly valuable. But applying addressability and one-to-one measurement at scale is impossible without a dynamic prefetch extension to your SSAI. Otherwise it is highly likely that ad-decisioning servers will time out and fail to return a response.

It’s important to be real about concurrency. Concurrency means the number of viewers watching at the same time. It’s not an average over a day, or a period of play, it’s minute-by-minute.

Mass reach is not only the domain of live streaming. VOD creates water-cooler fortnights. Some shows are a must-watch. Remember how Tiger King made Joe Exotic a household name in the space of a fortnight? Even though viewers are not pressing “play” at the same time, they are doing so in a short timeframe and putting extra demand on the streaming and advertising tech.

Maximizing inventory

In live sports, many advertising opportunities are missed because they’re so challenging to access. A half-time ad break in a soccer match can be planned for. The timing is dependent on the referee’s whistle, but the duration of the ad break and session ID is known in advance.

But what makes sport so compelling are the twists and turns, in other words: the unexpected. If a World Cup soccer match goes to penalties then all of a sudden an unplanned, but incredibly valuable ad break, is created immediately before the first penalty kick. We’ve seen audiences double between the end of extra time and the start of penalties.

Dynamic prefetch with contingency ad pods is essential to capitalise on these highly engaging and valuable moments.

Campaign management

SSAI is not simply a case of switching on a tap and letting the ads flow in. It must be integrated closely with the adtech ecosystem to deliver ad operations teams the right data to manage their campaigns. In order to consistently deliver the highest fill-rates, real-time measurement of ads viewed must be surfaced within a live 24/7 campaign dashboard.

In OTT, too much advertising is measured by ads stitched. That method is not sufficient for ad ops to make informed decisions about their campaigns.

UX and complexity

SSAI delivers a consistent, seamless viewer experience across all content types and devices. It effectively replicates the experience of traditional TV. It also goes some way beyond that.

SSAI must support all kinds of UX features, from clickable ads to scrubbing. Increasingly, viewers are expecting longer DVR windows, meaning the SSAI must be able to support whatever business logic is required to maximise the potential of advertising in live-rewind mode.

As you can see, SSAI is capable of delivering a huge amount of added value to OTT advertising propositions. As the industry’s reliance on advertising revenue grows, it is increasingly important that broadcasters and streaming providers offer the best possible ad product to the market in order to deliver better value and appeal to more advertisers.

Generative “Eno” Documentary Reshapes the Film for Every Viewing

From “Eno” by Gary Hustwit, a generative cinematic documentary

TL;DR

“Eno,” about the career of famed musician and visual artist Brian Eno, was created as a generative, cinematic documentary.

Instead of a standard bio-doc, filmmaker Gary Hustwit and his collaborators have assembled a “modular” film that shuffles unpredictably between time periods and mediums to offer a composite portrait of its subject.

The technology is developed by Hustwit’s own startup Anamorph, which they call a “generative system” rather than generative AI.

A randomized documentary of the career of legendary techno-music pioneer Brian Eno, in which every screening is potentially and infinitely different, is the latest project to be served up by generative AI.

Enois a generative cinematic documentary: “Like a musical performance that’s different every night, the film creates a unique viewing experience for each audience that takes it in,” explains Matt Grobar at Deadline.

The 75-year old British music producer and visual artist who has worked with David Bowie, U2, Grace Jones and Talking Heads, and who birthed the ambient music genre and frequently mixes technology with art, is ripe for a video retrospective.

“I usually can’t stand docu-bios of artists because they are so hagiographic,” Eno told Variety’s Todd Gilchrist.

So, rather than charting a chronological path through Eno’s career, documentarian Gary Hustwit proposed using a generative system to create a film that would literally be different for every audience that screened it.

“The use of randomness to pattern the layout of the film seemed likely to override any hagiographic impulses,” Eno said.

If that was enough to pique Eno’s interest in the project, for Hustwit the approach was about provoking new ways of creating and experiencing a film.

“I like movies where you learn different things about the subject, but you, as the viewer, make the connections… I always think that’s a lot more rewarding, as a viewer. It’s a different kind of filmmaking, but it’s also a different kind of film watching.”

It helps that the first and last scenes of the 85-minute doc are always the same. Plus, there are certain scenes pinned to the same timeslot in each version, including a scene where Eno discusses generative art.

Everything else, however, can be different, depending on the material the generative program decides to insert.

A still from “Eno” by Gary Hustwit, a generative cinematic documentary. Cr: Sundance Institute

“It’s kind of a modular approach,” Hustwit explained to Forbes’ David Bloom. “You can learn different facts about that person at different times in the film. In the end, you make the connections as a viewer.”

Like one of media artist Refik Anadol’s AI creations, Eno is going to be different each time it is screened. That poses a problem for film critics, Bloom points out.

To Deadline, Hustwit explained, “There are billions of different combinations that could possibly exist of this movie, and every time you watch it, you’ll never see that version again. So, it’s an interesting experiment. We can change the way that the form of film works [so] let’s talk about the possibilities.’”

Hustwit had another reason for making the film this way too. It’s a showcase for the generative tool (cutely dubbed Brian One) that he has built along with digital artist Brendan Dawes by their startup company Anamorph.

The tech was trained to select scenes from over 500 hours of archival footage and new interviews of Eno as well as animated visuals and music to produce the unique iterations of the doc.

Anamorph spent five years building the software, combining patent-pending techniques with the team’s own knowledge of storytelling. The company says it’s not trained on anyone else’s data, IP or other films.

“Eno” director Gary Hustwit. Cr: Ebru Yildiz/Sundance Institute

“The main challenge was creating a system that could process potentially hundreds of 4K video files, each with its own 5.1 audio tracks, in real time,” Dawes tells TechCrunch. “The platform selects and sequences edited scene files, but it also builds its own pure generative scenes and transitions, creating video and original 5.1 audio elements dynamically. The platform also needed to be robust in a live situation, it wasn’t an option to have it crash. So, we did a crazy amount of testing. We can create a unique version of a film live in a theater, or we can render out a ProRes file with its own 5.1 audio mix and make a DCP from that.”

He also stresses, “This is a generative system, not generative AI. I just need to make that clear, because pretty much everything that’s been said about Eno uses the word AI.”

Advertising agencies have apparently expressed their interest, Hustwit reveals to TechCrunch, with one company wanting to make 10,000 versions of a one-minute commercial.

Rather than make its tools publicly accessible, the company wants to collaborate on projects so it can “consider the source material and the overall story goals,” says Hustwit.

“Our main goal is to get the idea out about this new kind of cinema and hook up with great collaborators to help explore this idea.”

Hustwit ponders what an experimental form-pushing director like Jonathan Glazer (TheZone of Interest) could do with something like this.

“You could make a movie that’s always on, always evolving, always changing,” Hustwit told Forbes. “I feel like Eno, it’s really kind of an opening conversation. What’s next? What can we do with this?

A streaming service such as Netflix — which has played with interactive forms of video — could easily generate a different version of the documentary every day, Hustwit added.

However, to TechCrunch he poured cold water on the idea, saying that streaming networks aren’t equipped to dynamically generate unique video files and stream them to thousands of viewers so that each viewer is getting their own version of a movie.

“When we premiered Eno at Sundance, all the big streaming companies loved it, but they also admitted that their systems can’t handle the tech involved… These streamers need to differentiate, and I think enabling the films and shows they’re releasing with generative technology is a way to do that,” says Hustwit.

It’ll likely take years before streaming services adapt to the technology. Until that happens, Anamorph is sticking to live events and theatrical releases.

“Something that the theater industry badly needs right now is a reason to get people to come in, and if there is a uniqueness about the live cinema experience, that’s one way that can be achieved,” he adds.

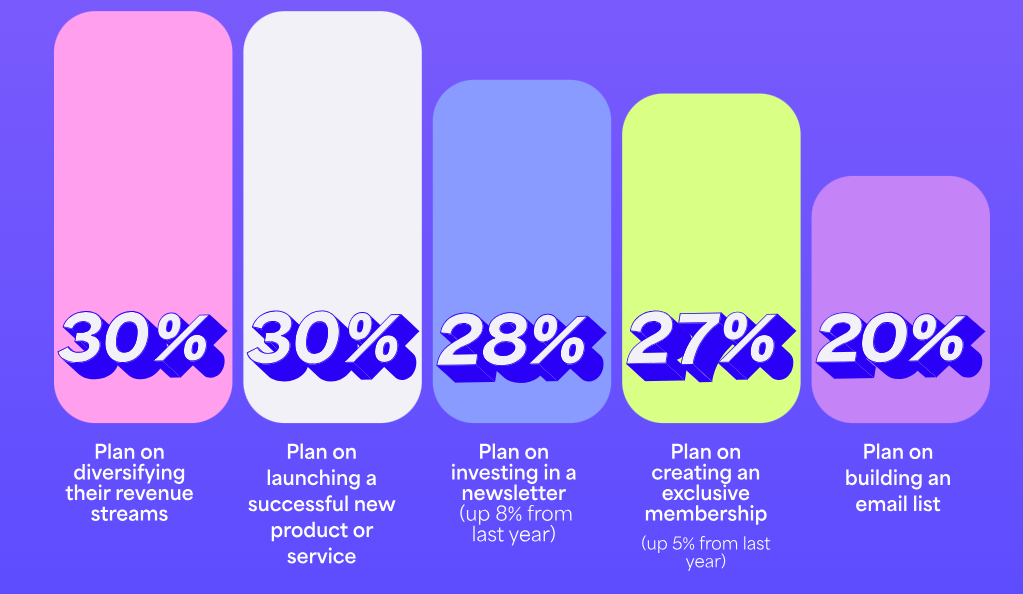

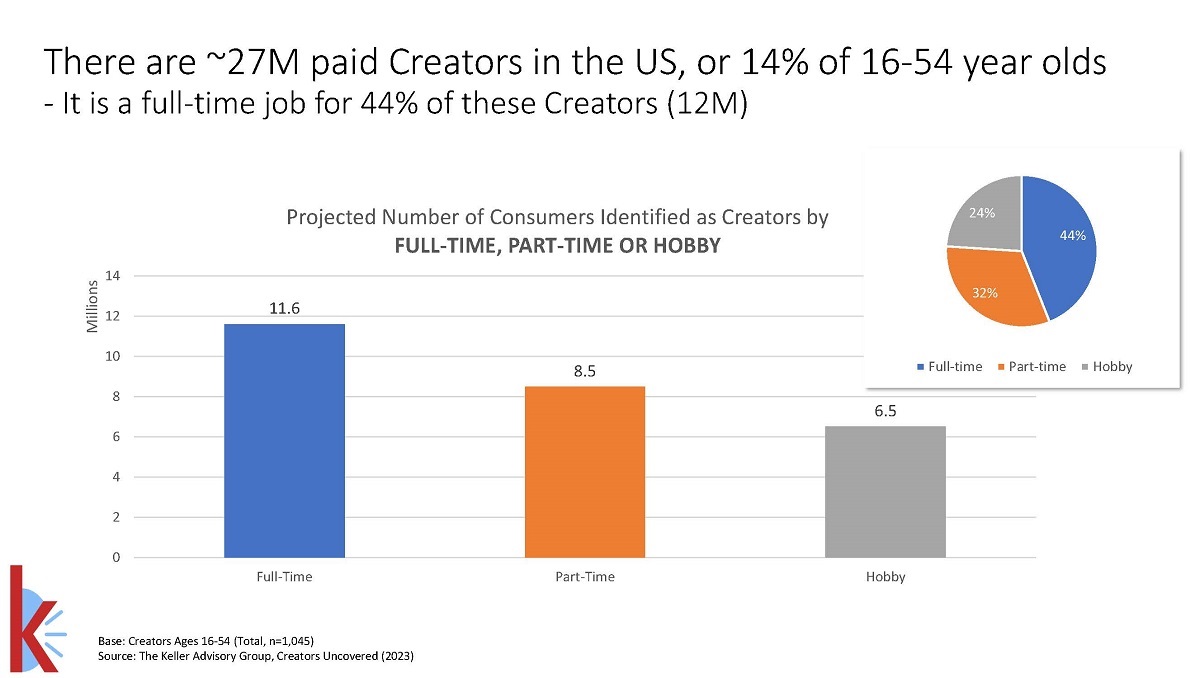

You may have heard that the creator economy is projected to grow to a $480 billion-industry by 2027, but did you know that there are now approximately more than 50 million creators working in the industry in 2024? And 4% of those workers earn more than $100,000 annually. Those figures are according to Kajabi’s The State of Creators ’24 Report.

From Kajabi’s The State of Creators ’24 Report

This report focuses on the creators earning six-figures or more, assessing what they have in common to divine what makes for success in the creator economy.

How Creators (Really) Make Their Money

First, there’s more to being a successful creator than social media posts and striking brand deals (although creators do say those are key!).

To crack the six-figure ceiling, creators say they must diversify their revenue streams, with five (!) or more sources of income being a differentiator — and those making more than $150k annually report using at least seven to make that salary, according to Kajabi’s survey.

From Kajabi’s The State of Creators ’24 Report

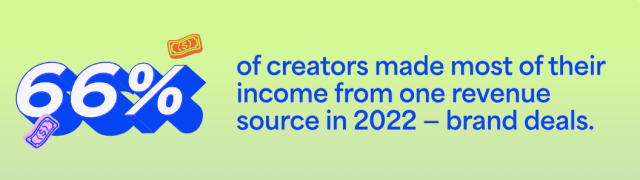

This is especially revealing because 66% of creators say they made the majority of their income from brand deals alone. However, these types of partnerships are fickle, and three-quarters of those who self-identify as top earners say that multiple revenue streams are crucial to financial success. “[D]iversifying their income streams empowers creators to turn down deals that could compromise their authenticity,” according to the report.

However, it’s worth noting that even authentic but successful creators say they can be tempted to compromise – for the right price. More than half of those in the $100k+ bracket said they might work with a brand whose values didn’t align with their own if the payoff was right (a specific number was not named).

So if you can’t go all-in on brand deals, what are other popular options? Those in the six-figure-plus club told Kajabi they make money from passive income (such as digital products, platform payouts and physical products) as well as coaching and consulting jobs, which they may do in person or online.

The most popular digital offerings include: online courses, digital downloads, subscriptions or memberships, and online consulting/coaching.

From Kajabi’s The State of Creators ’24 Report

Social Is About Engagement (and Lead Gen)

The Creator Economy may be synonymous with social media, but they’re not one and the same. As Kajabi puts it: “Social platforms are great for building audiences, not businesses.”

Successful creators are able to translate followers into customers using lead gen tactics, leveraging audience interaction and community into cash generated on platforms that they own.

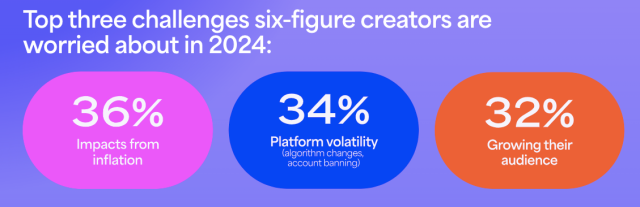

However, creators are not likely to abandon social media any time soon. Even six-figure creators would have trouble if they lost access to a platform. Losing YouTube would mean missing out on at least $50,000 annually for 42% of creators making $100k+. Instagram going under would account for the same loss for 38% of those surveyed; TikTok would mean the same for 37%; and 36% said the same would be true for Facebook.

From Kajabi’s The State of Creators ’24 Report

Despite those numbers, half of creators indicated that they do not trust the very social media platforms that made them popular. They’ve been burned before, after all. Kajabi notes that it will be interesting to see if TikTok’s Creativity Program will shift creators’ attitudes.

Six-Figure Creator Demographics

The most successful creators as of 2024 are:

Male (57%)

Have a bachelor’s degree or higher education (80%)

Work full-time as creators (86%)

Create content for business and marketing, finance or real estate niches

They also tend to reach this financial tier relatively quickly. Four in ten of the six-figure earners reached that status within two years of working in the Creator Economy. Notably, the content niches that catapult creators into this range the fastest are beauty, fitness and gaming.

Their Thoughts on Today’s Hot Topics

Kajabi also inquired about these creators’ attitudes toward two of the buzziest subjects of 2023: AI and unionization.

AI emerged as a key differentiator for creators who’ve had financial success. They tend to utilize it twice as often as their counterparts making $99k or less, with 29% reporting that they leverage AI tools daily, and 43% say they use it weekly.

“Six-figure creators are bullish on AI in 2024 specifically to save time and ultimately help reduce creator burnout,” according to Kajabi.

Also, success has not made creators want to go it alone. Likely driven by their distrust of the social companies, almost 50% of these creators say they’d be interested in joining a creator union if one were formed. Notably, their interest was higher than that of their peers earning less cash.

The AI Broadcast TV and AI VFX & Motion workshops will also be offered at the 2024 NAB Show in Las Vegas, available to NAB Show registrants for $299. Both three-hour sessions are scheduled for Wednesday, April 17 at 2 p.m. (PT) and in the South Hall of the Las Vegas Convention Center.

NAB Show and FMC also offer a corresponding certification for each course of study. Certification exams cost $149 and are scheduled for 45 minutes. Those who are certified will then be added to a published database of AI professionals.

“NAB Show is committed to empowering broadcasters and professionals across the full range of creative fields with the knowledge to integrate AI into their work, in a way that ensures they are able to remain current and innovative,” said NAB Global Connections and Events EVP and Managing Director Chris Brown.

These Are the Entertainment Industry Jobs That’ll Be Impacted by AI (Yes, Some for the Wrong Reasons)

From director Paul Verhoeven’s “RoboCop,” courtesy of Warner Bros.

TL;DR

CVL Economics surveyed 300 leaders in the entertainment industry about generative AI to investigate how uptake of the technology will likely affect M&E jobs in the near term.

A number of job functions are projected to be especially vulnerable: sound designers, 3D modelers and foreign language dubbers. Also at high risk: Those seeking entry level positions and contract work. Writers and vocal/music performers are expected to fare better, at least in the near term.

However, the associations that commissioned the study intend to use the information to fight back against the negative impacts of Gen AI uptake during their upcoming contract negotiations.

Do you think your job is safe in the age of Gen AI? I have some not-so-great news for you: Your boss’s boss probably doesn’t agree.

In Q4 2023, the consultancy surveyed 300 entertainment business leaders to assess how generative AI will likely affect the M&E workforce.

Respondents represented six sectors: the film, television, animation, music and sound recording and gaming industries. About two-thirds of those questioned agreed implementation of Gen AI is likely to “play a role in consolidating or replacing existing job titles,” according to the study.

Generative AI has come to the forefront of the public imagination “[a]t a time when several entertainment industries are facing challenges,” the report notes, adding that “the desire to increase productivity, cut costs, and identify new revenue streams will be top of mind.”

But the good news is that a majority of respondents said, “GenAI has already led to the creation of new job titles and roles in their organization and anticorporate GenAI technology will be responsible for the creation of new job opportunities.” (But that’s no guarantee that the scales will ultimately balance for workers in any industry.)

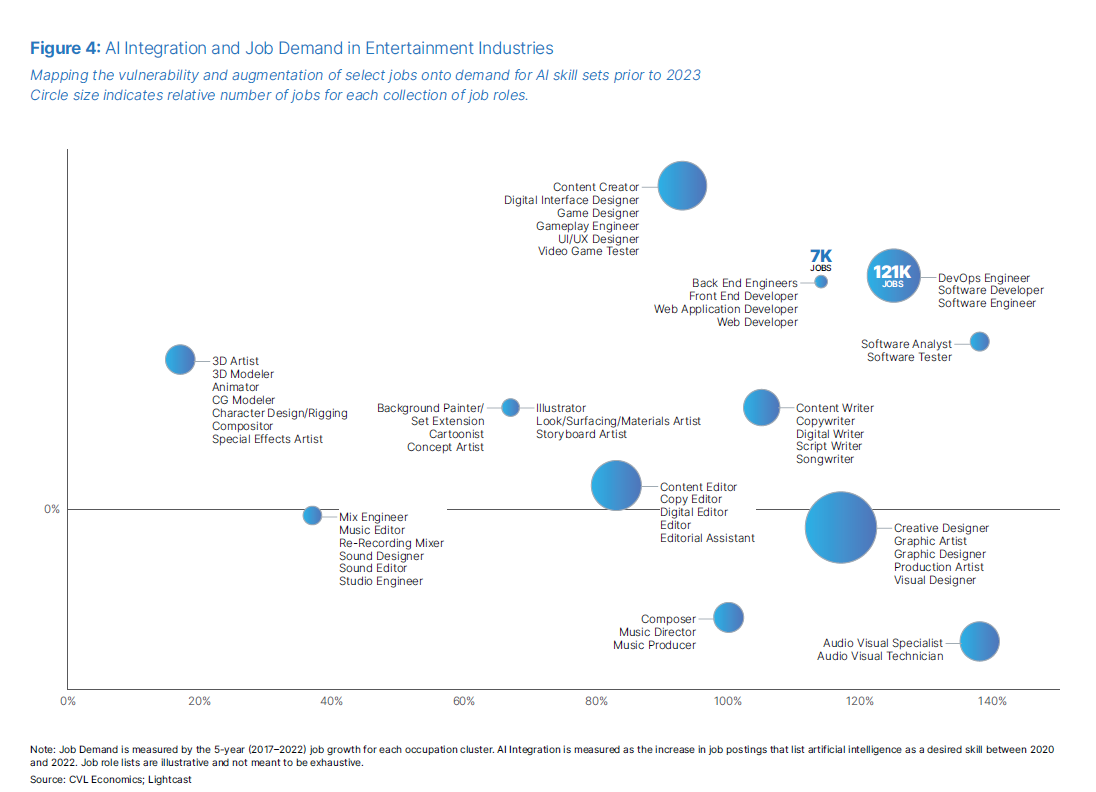

For context: “[T]he pace of AI integration into creative job roles is increasing at a rapid clip; between 2020 and 2022, for example, the number of job postings that listed the ability to use artificial intelligence tools as a desired skill increased by 122%,” The Hollywood Reporter’s Winston Cho points out in his coverage of the report.

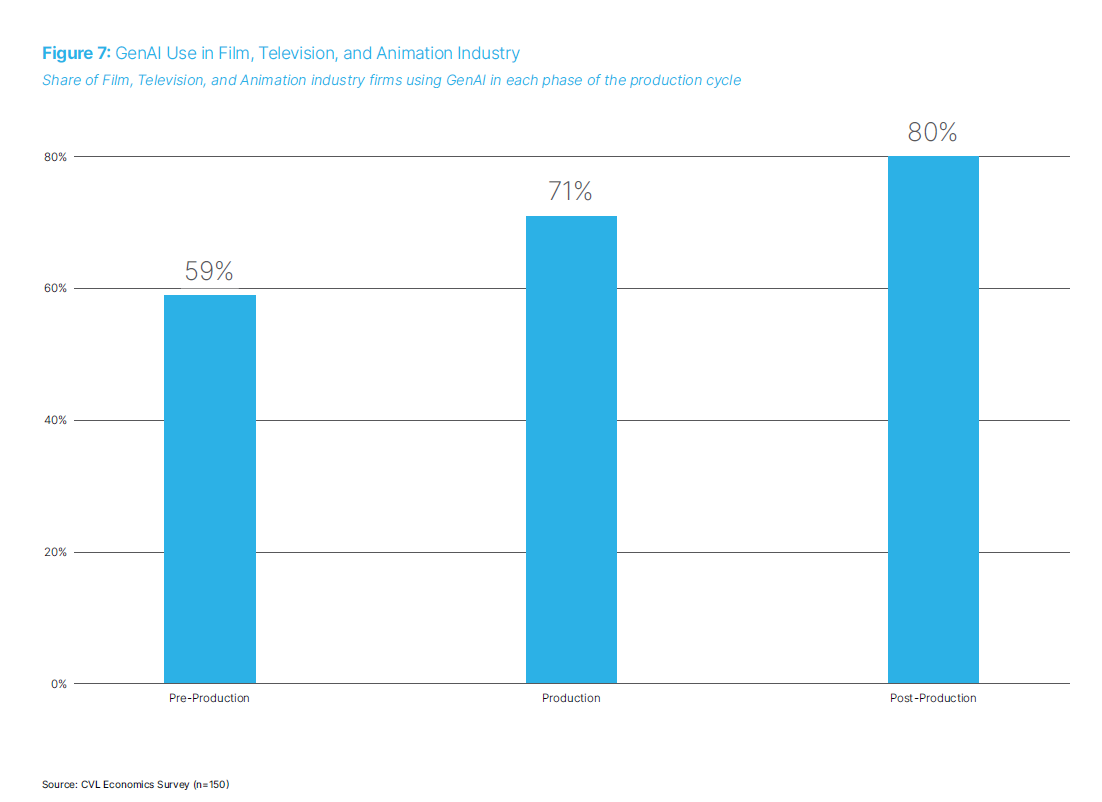

GenAI use in film, television and animation, Cr: CVL

CVL writes: “[C]reative workers will be facing an era of disruption, defined by the consolidation of some job roles, the replacement of existing job roles with new ones, and the elimination of many jobs entirely.

But We’re Not Taking This Lying Down

Disney Animation Technical Director Brandon Jarratt, who serves on the Animation Guild’s executive board and AI task force, told the LA Times’ Christi Carras that Local 839 will use the study to inform strategy and goals for upcoming negotiations.

The Animation Guild is not the only M&E union likely to follow the blueprint laid out by the WGA and SAG. CVL notes 8% of jobs in the arts, design, and entertainment have representation and collective bargaining. That figure is higher when you narrow it down to the motion picture and sound recording industries (17%) and broadcasting (11%).

CVL concluded that “[c]reative industry leaders are largely embracing GenAI technology, and most recognize that operational benefits in the future will come at a cost to many creative workers.”

The Animation Guild, Jarratt told Carras, aims to “help set the industry standard for what kind of tools are appropriate and … going to help artists, and which ones are going to hurt them and hurt their livelihoods.”

After all, “[t]he tool itself is almost never the issue,” Jarratt explained to Carras. “The studios are always looking for ways to spend less money. And if they feel like they’re going to be able to cut budgets in order to meet shareholder projections or whatever, then they’re going to try to exploit that in any way they can — and that’s where the fear comes from.”

Lest you think that fear is overblown: In November, DreamWorks founder Jeffrey Katzenberg predicted that Gen AI will replace up to 90% of film animation jobs, THR’s Cho notes.

“We’re seeing a lot of role consolidation and reduction,” Concept Art Assn. co-founder Nicole Hendrix told Cho. “A lot of people are out of work right now.”

As a whole, the media and entertainment industry seems more inclined to embrace generative AI — and more likely to be early adopters. CVL reports that 25% said they are currently using some kind of Gen AI, and nearly half (47%) indicated they are planning to implement generative AI soon, in some fashion.

CVL calculated that Gen AI is likely to disrupt “approximately 203,800 payroll jobs” in the US.

In the parlance of the study, a “job is considered disrupted when a significant amount of tasks within that role are consolidated, replaced or eliminated as a result of AI,” per Carras.

She writes, “In an industry already brought to its knees by the COVID-19 pandemic, overspending during the streaming wars, overlapping labor disputes and mass layoff-inducing corporate mergers, AI is just one more wrench to worry about for entertainment workers.”

“Among the top tasks flagged as likely to be impacted by AI: creating realistic sound design for film, TV or games; developing 3D assets; and creating realistic sounding foreign-language dubbing. The tasks least likely to be affected include writing film, TV or game scripts, as well as performing music or vocals,” Cho summarized.

Note that more than half of those expected to be affected reside in a handful of U.S. states: California, New York, Georgia and Washington (places known for their connections to film, television and gaming).

They also point out that gig workers and freelancers are likely to be hit hard by the incorporation of AI tools; they concede that “change may not be systematically understood or visible beyond anecdotal data” for these types of workers.

Still, it’s worth pointing out, since the report estimates that 29% of U.S. arts, design, entertainment and media workers are self-employed or operate in a similarly independent fashion, more than four times the national average for all major occupation sectors.

CVL tried to suss out the impact by comparing the firms that lean heavily on freelancers with their attitudes toward early Gen AI adoption, and there was an overlap for nearly 8 in 10 companies.

Also likely to be on the Gen AI chopping block are entry level positions, which will have downstream effects on the talent pool. The report frets that this in turn will limit networking opportunities and the acquisition of “domain knowledge,” which are cumulative.

“When you’re looking at any technology that’s essentially replacing [or consolidating] a junior or entry-level role … it is harming the ecosystem,” The Concept Art Assn.’s Hendrix told Carras. “What does that mean if nobody’s really entering in and the bar is now this immovable wall?”

And unless firms are especially careful, DEI initiatives are likely to suffer, CVL cautions.

“Aspiring workers from less affluent and underrepresented backgrounds have historically leveraged these entry-level roles as a pathway into the entertainment industries and to higher-paying positions,” Cho writes.

However, all of these outcomes are not inevitable (except, perhaps the integration of generative AI into nearly every workflow in the same way that the Internet has permeated our lives). Understanding trend lines is not synonymous with seeing an unchangeable future. Unions and regulatory bodies will have a say in how this plays out, in addition to corporations and creatives.

As Cho puts it: “The future is not yet written, and it needn’t be generated by AI.”

Amid fears over the use of generative AI in Hollywood, artificial intelligence seems less likely to replace humans than to assist them.

February 8, 2024

Posted

February 7, 2024

Reading Between the Lines: Gen Z Really Loves Closed Captions

Maude Apatow in HBO’s “Euphoria,” photo by Eddy Chen/HBO

TL;DR

More than half of Gen Z and millennial media consumers prefer subtitles, according to new survey results from YPulse and Preply.

While subtitles haven’t always been seen as a first choice, they’ve grown in ubiquity — especially with the rise of online videos that include automatic captioning.

Captions help watchers keep up with murmuring dialogue, distinguish thick accents and get a head start on a scene.

Closed captions aren’t just for the hearing impaired — the rise in its popularity is being driven by younger viewers who are in fact making the use of subtitles while watching television the norm.

In a new “TV and Entertainment report,” YPulse found that more than half of 13-39-year-olds prefer to use subtitles.

And it’s not just because they need them; the younger generation makes use of reading text while watching movies/TV to keep up with murmuring dialogue, to distinguish less familiar accents, and some say just to get a head start on a scene and go back to looking at their phone.

Per the report, 59% of Gen Z survey respondents and 52% of millennials said they use subtitles. 61% of Gen Z males say they prefer to use them.

These are no outliers. A 2023 report by Preply found Gen Z overwhelmingly the generation most likely to be turning on subtitles (70% of Gen Z respondents said so compared to 53% of Millennials, and just 35% of Baby Boomers).

As to why Gen Z likes to turn on text while watching their shows, part of it, according to Wilson Chapman at IndieWire, is that people in that generation grew up watching videos on social media, where subtitles are the algorithmically encouraged default.

Sara Fischer at Axios writes that TikTok helped normalize captions for young media consumers, who are now turning regularly to subtitles as part of their streaming habits.

“TikTok has an auto caption feature that a lot of content creators will use,” Axios reporter April Rubin told WGBH Morning Edition co-host Jeremy Siegel. “And so people are just a little bit more used to reading as they watch. Another factor that may play into this is that it has been a little tougher to maintain quality sound in the streaming era. So they could be watching subtitles just because they’re missing some of the dialogue with background noise or changing volumes.”

Younger kids actively need subtitles to enjoy the content they are watching, according to a Kids Industries survey of US and UK parents with kids 5-15 years old. In this case, subtitles add an increased dimension of understanding to viewing. Watching content with closed captions can reportedly improve literacy, vocabulary, and the speed of reading, the report said.

“For kids’ media brands, the widespread use of closed captions should be a sign to improve accuracy and make sure subtitles are available for all programs,” suggests YPulse.

But closed captions are being used more by all of us. A 2022 report by Netflix revealed that 40% of its global users use closed captions on all the time, while 80% switch them on at least once a month.

In its survey Preply determined that half of Americans used closed captions with the top reason (cited by 72% of respondents) being that subtitles make dialogue easier to understand.

As Chapman lays out in IndieWire, the causes behind muddled dialogue are many and might vary between person to person. For some, the problem is the design of modern televisions; the majority of which place internal speakers at the bottom of the set instead of facing towards the audience, causing significantly worse audio quality. Other issues are caused by sound designs optimized for theatrical experiences, which can result in compressed audio when translated to home.

“A lot of people struggle to hear dialogue now, so turning on closed captioning to decipher what people are saying has become a no brainer move,” he says.

An article in British broadsheet The Guardian also focuses on the issue of hard-to-hear dialogue which is a known issue in the industry, according to sound mixer Guntis Sics (Thor: Ragnarok), who is quoted in the piece.

Where once actors had to project loudly towards a fixed microphone on set. more portable mics has allowed a shift towards a more intimate and naturalistic style of performance, where actors can speak more softly — or, some might say, mumble.

“Antony Hopkins on Thor spoke like a normal human being, whereas on a lot of other films, there’s a new style with young actors — it’s like they just talk to themselves. That might work in a cinema, but not necessarily when it gets into people’s lounge rooms,” Sics says.

The Guardian’s Katie Cunningham also suggests sound mixes have become more complicated — fine for the 22.2 speakers of Dolby Atmos in a theater but indistinct when played back through a TV’s tiny and tinny speakers.

“When sound is mixed with the best possible audio experience in mind much of that detail can be lost when it’s folded down to laptop speakers, or even your television. It’s often the dialogue that suffers most.”

If you haven’t invested in an expensive speaker set up at home then reliance on the TV’s speaker output alone “could leave you with a subpar experience.”

Of course, the volume of foreign language shows and the phenomenal popularity of some of them — from Squid Game to Money Heist — demands subtitles, but even English-language shows seem too hard for many Americans to understand.

British comedies and dramas that aren’t the usual period dramas like The Crown are often acted with authentic local accents. Peaky Blinders (Birmingham), Derry Girls (Northern Irish) and even contestants on reality TV shows like Love Island are called out. As is Irish Oscar-winning drama The Banshees of Inisherin.

“If people get used to using subtitles where it’s basically required, it becomes a matter of habit to keep them in use even when watching American productions,” says Chapman.

In her article, she states the captioning services market in the US as valued at nearly $170 million in 2022. Studios however often outsource the work to companies like Rev, which in turn has 75,000 international freelancers on its books for transcription work.

Some studios issue very specific subtitle requirements. Netflix’s style guide includes rules like a limit of 42 characters per line, a set reading speed of up to 20 characters-per-second for adult shows (up to 17 for children’s programs) and an emphasis that “dialogue must never be censored.”

To prepare for live events like awards shows, captioners are given a script in advance of everything from the teleprompter — except for the names of the winners. When people ad-lib or give their acceptance speeches, the captioners are working from scratch.

“The person gets up and thanks someone with a very complicated name. We take a guess at it, but we’re going to spell it wrong. That’s bound to happen,” says Heather York, VP of marketing for captioning company Vitac.

Streamers often ask for subtitles in up to nine languages before their shows drop, creating a new challenge for service providers.

“We’ve got to pivot with our workflows, with our resources,” says Deluxe senior VP Magda Jagucka. “That process to bring non-English original content to global audiences requires multiple translation and adaptation steps.”