TL;DR

- Market data platform Antenna highlights five factors of importance in the year ahead: pursuing scale, revenue optimization, dual revenue streams, owning the customer relationship, and customer segmentation.

- Perhaps the most important battle is now around owning the customer relationship, but customer segmentation could be the defining topic going forward.

- With an increased focus on profitable growth, SVODs are becoming more aggressive in their efforts to maximize revenue, even at the expense of some topline subscriber growth.

READ MORE: The State of Subscriptions Report (Antenna)

SVODs are experiencing tremendous volatility and we should expect more targeted acquisition strategies from the major streamers, an increased focus on pricing and packaging, and numerous moves to mitigate churn.

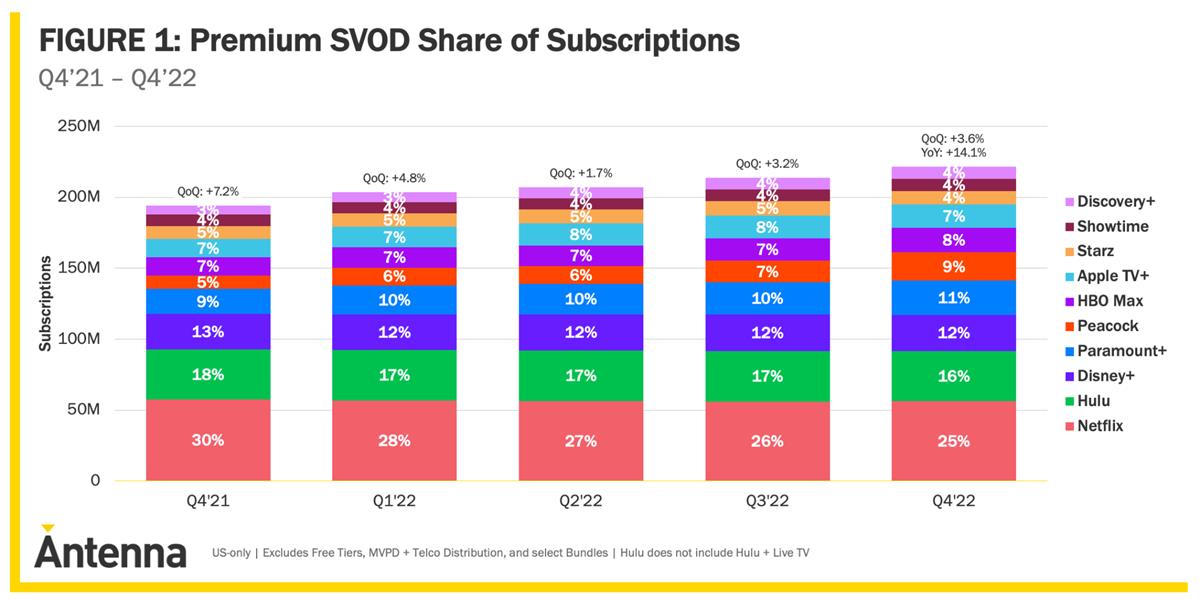

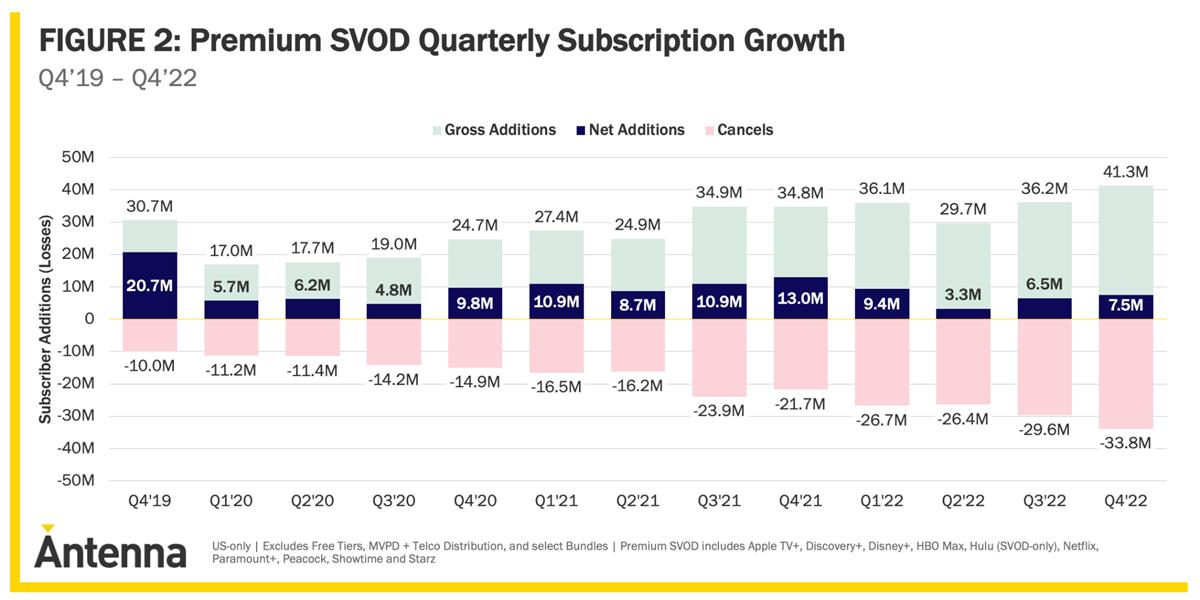

According to market data platform Antenna in its latest report, “The State of Subscriptions,” last year represented a turning point for premium SVODs. While total subscriptions grew substantially at 14.1% over the prior year, that rate of growth was significantly slower than 2021’s 28.9%. Worryingly, Antenna observed 117 million cancels across Premium SVODs in 2022, up 49% from the prior year.

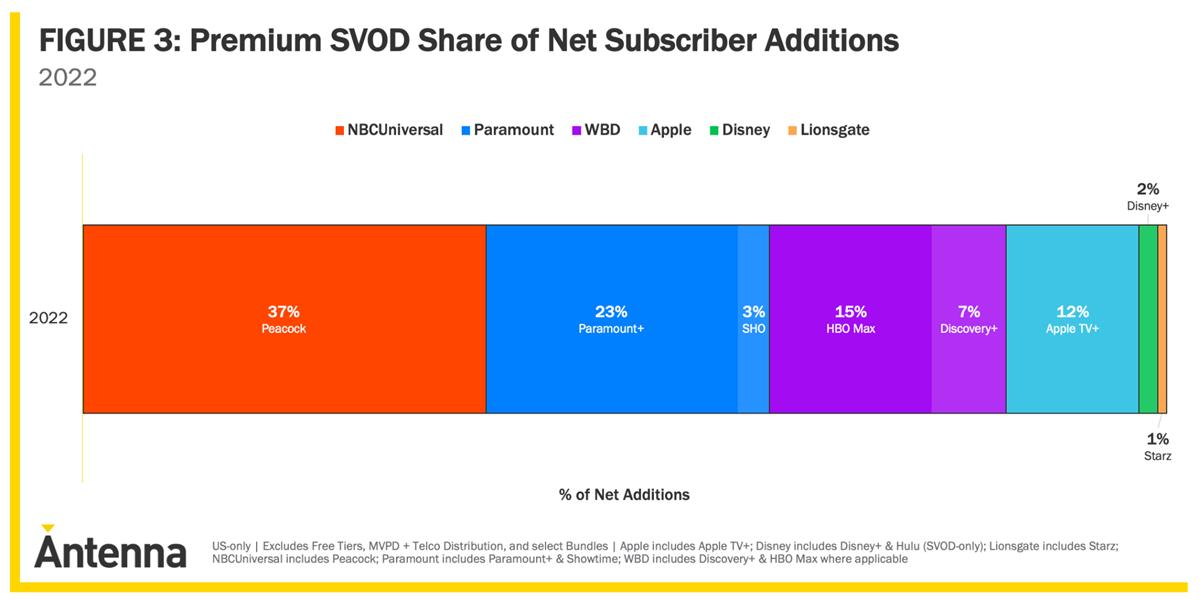

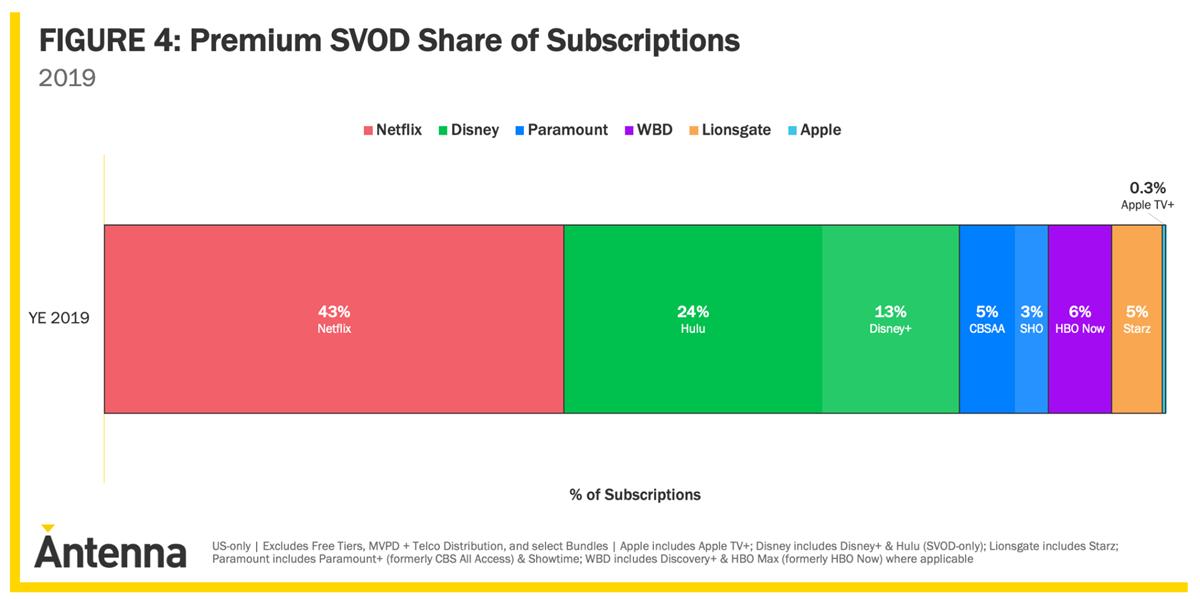

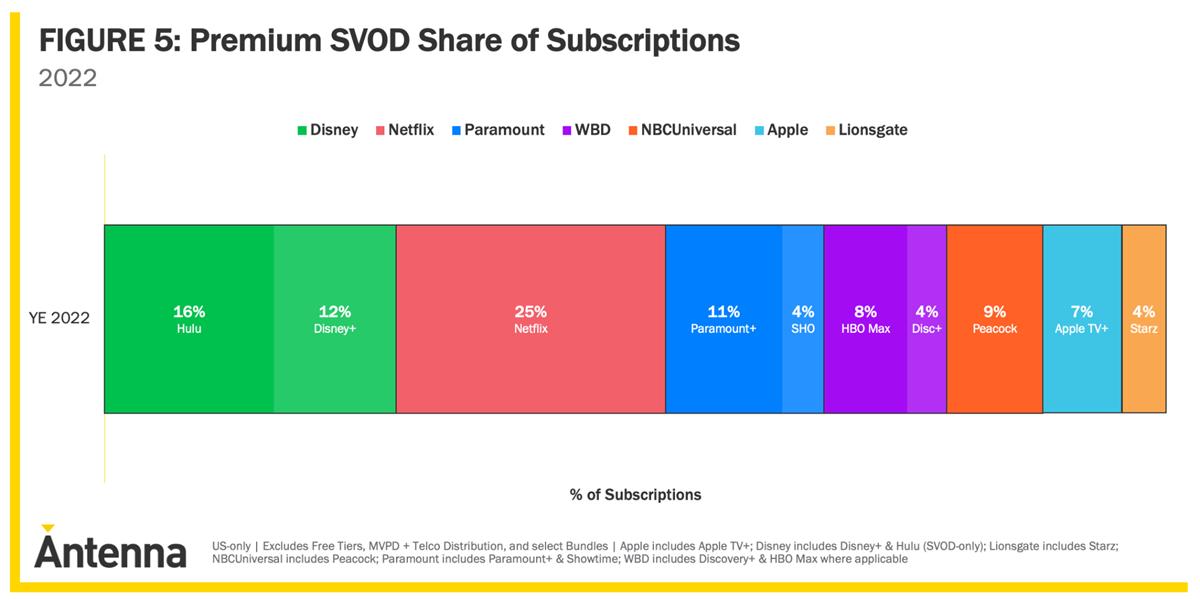

NBCU, Paramount, and WBD were especially successful at growing their subs in 2022 taking share from Netflix and Disney although the latter two still lead the pack.

“With an increased focus on profitable growth, SVODs are becoming more aggressive in their efforts to maximize revenue, even at the expense of some topline subscriber growth,” Antenna reports.

Price increases are the most obvious example of this: Netflix, Apple TV+, Disney+, and Hulu all raised fees in 2022, and HBO Max did so this January. Paramount and NBCU also announced pricing moves in the opening months of 2023.

Intra-company bundles are another strategy to drive increased Average Revenue Per User (ARPU).

Antenna estimates that the Disney Bundle now accounts for 22% of subscriptions for Disney+, 18% for Hulu, and 60% for ESPN+. The Apple One bundle accounts for 31% of Apple TV+ subscriptions, and subscribers to the Paramount+ and Showtime bundle grew 251% in 2022.

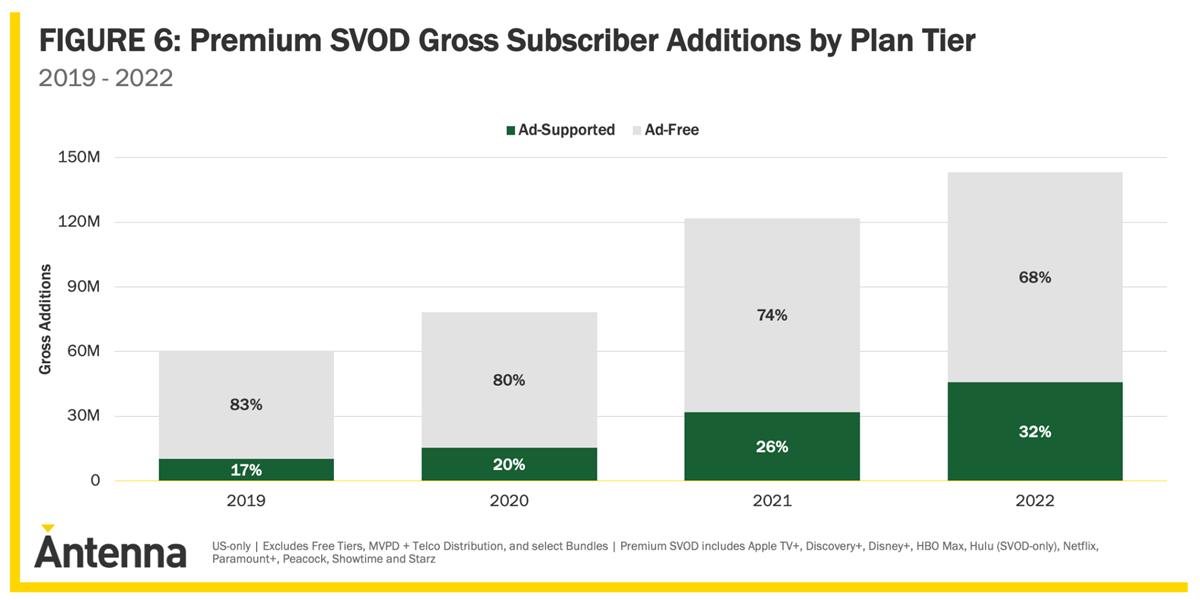

The role of advertising continues to grow in importance to premium SVODs, as a part of their profitable growth strategies. In 2020, only one in five new sign-ups were to ad-supported plans; last year, it was nearly one in three.

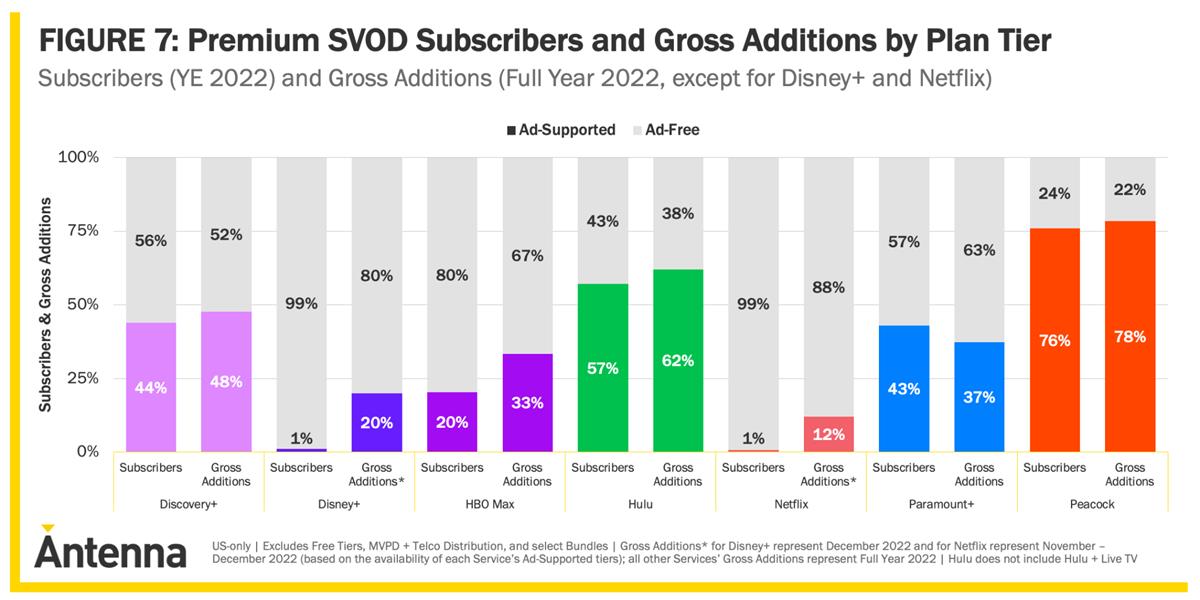

The four services that have had ad-supported plans since their inception — Peacock, Hulu, Paramount+, and Discovery+ — each have at least 43% of Subscribers on the ad-supported option.

And ads are gaining ground. The proportion of 2022 Gross Adds (i.e., new customers) who selected the ad-supported option is higher than the existing subscriber base for six of the seven premium SVODs.

Owning the Customer Relationship

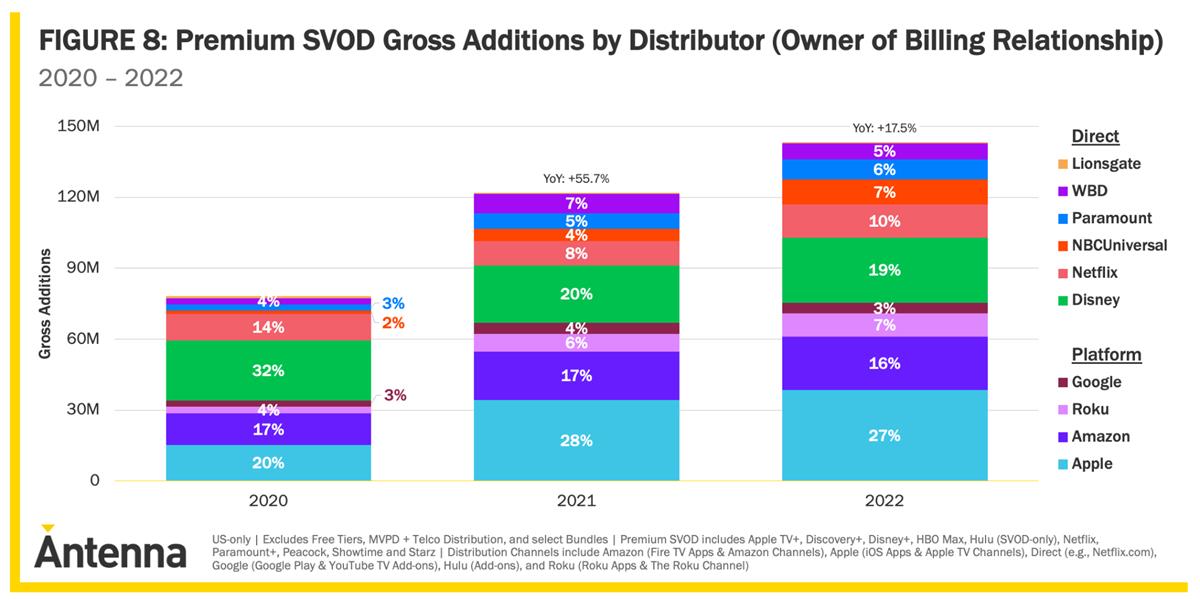

An increasingly important battle is the competition for the customer relationship. 53% of Gross Adds that Antenna observed in 2022 came through a distribution platform — Apple, Amazon, Roku or Google — not directly with the services themselves.

“D2C models are great for brands because they do not share margin with retailers or wholesalers, and they fully control the customer relationship. When an SVOD service wins a customer through a distribution partner, they typically share the economics, and the distribution partner controls portions of the customer data and communication (sometimes, a lot of it).”

These distribution arrangements can potentially deliver substantial incremental customers. And in environments like Amazon channels which load the services’ programming directly into their app, SVODs can save product development and upkeep costs because they do not have to operate their own proprietary app.

Antenna says, “Balancing the benefits and challenges of distributing in third-party environments is a key issue that Services will consider as they manage to profitable growth in the coming years.”

The final theme is one that Antenna think will be a defining topic for subscription marketers for years to come: customer segmentation.

There are many different approaches for segmenting consumers, but two which it believe are especially important for subscription marketers are re-subscribers and serial churners.

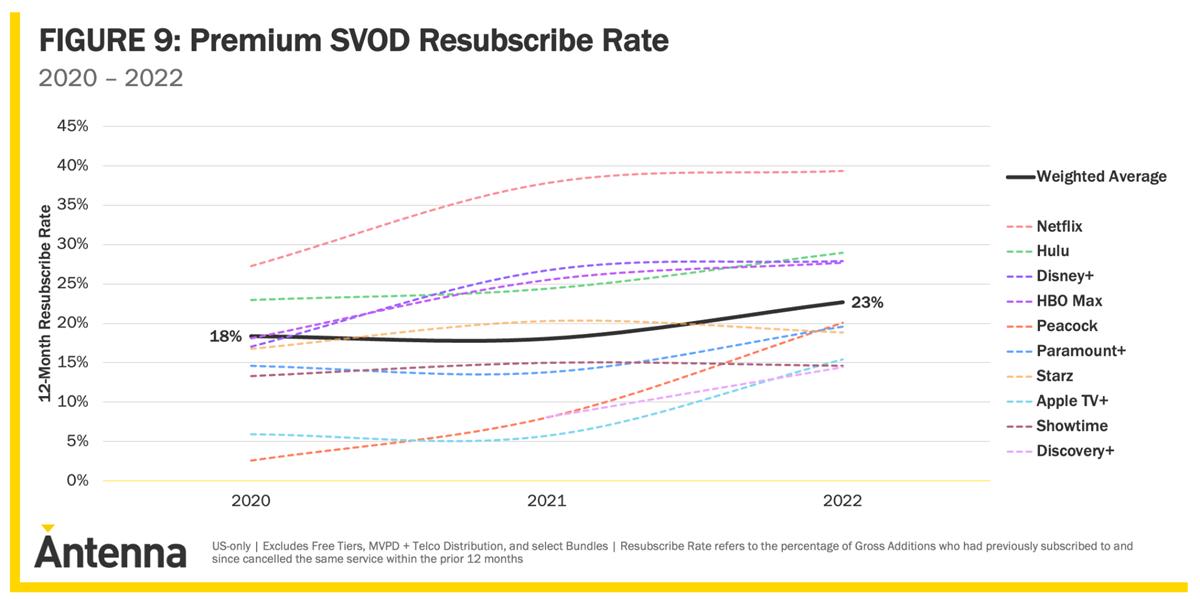

Re-subscribers are consumers who sign up for a service after previously cancelling it and made up 23% of all gross additions in 2022.

“Netflix has a high re-subscriber number simply because so many Americans have already subscribed to the service at some point in the past. Put another way, Netflix is running out of Americans who have never tried Netflix!“

On the other end of the spectrum, Peacock had almost no re-subscribers in 2020 because it launched in April of that year, but already by 2022, 20% of their Gross Adds were observed by Antenna to be re-subscribers.

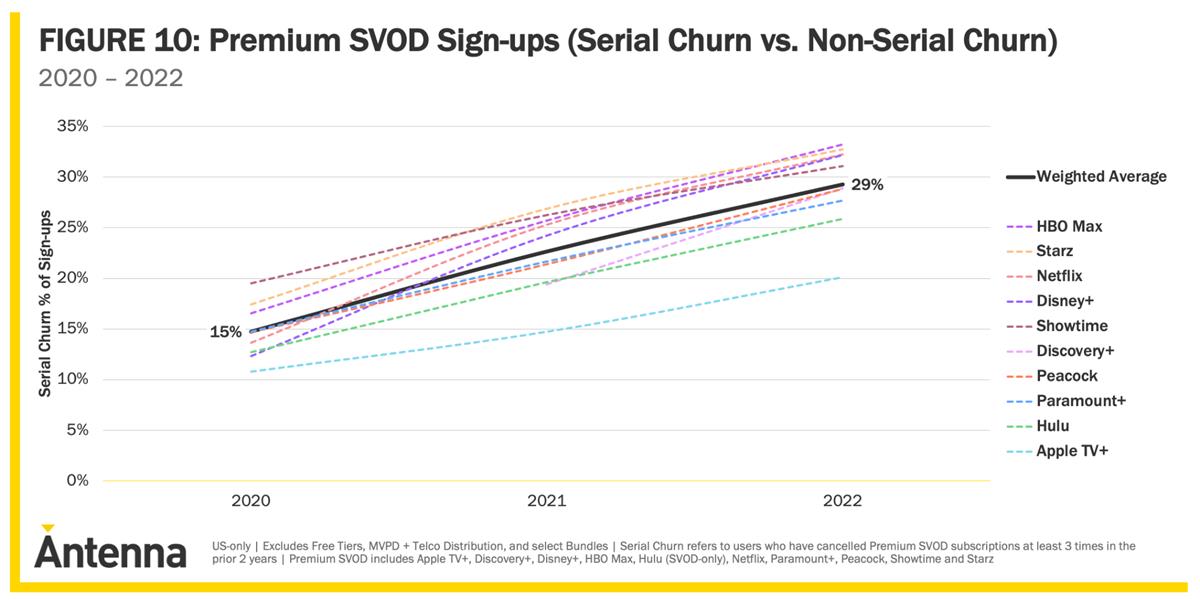

Serial churners are those individuals frequently moving in and out of services — often to chase hit shows they want to watch at that moment.

Antenna measures them as individuals who have at least three cancels in the past two years among the 10 premium SVOD services it measures.

So by that definition, one in five Americans is a serial churner and accounted for 29% of sign-ups in 2022, up from 15% in 2020.

Netflix is seeing a particularly pronounced growth, with serial churners making up 32% of sign-ups in 2022, versus 13% in 2020.

Per Antenna, “It is crucial that services segment out these serial churners. For one thing, their survival curves are much steeper than the rest of subscribers, resulting in lower customer lifetime values. If a service is not distinguishing between these two segments, then their analysis of cost of acquisition will be misleading.”

While changing macroeconomic conditions have played a factor in all these changes, the adjustment is also suitable in the context of a more mature market and a more fickle – or more sophisticated — consumer.