TL;DR

- SVOD price hikes may be approaching their peak: Consumers will likely balance costs and content with ad-supported tiers, contracts, and more bundles, but these may be short-term solutions to preserving profitability for streamers.

- Social media and unbundling pay TV have trained consumers to expect more customized and personalized content and advertising. Deloitte suggest these are levers to build greater consumer engagement and value.

- The biggest challenge for SVOD providers and studios is that they are no longer addressing a mass culture, but a fragmented landscape of competing digital entertainment options.

More evidence if it were needed that the video streaming model is shape-shifting under its own weight forcing players to adapt a much more sophisticated approach to market.

In its analysis from November 2023, Omdia found the number of SVOD services per home has declined in a number of markets for the first time. Market analyst Antenna in its latest “State of Subscriptions” report also finds that subscriber growth among Premium SVODs slowed last year to 10%. Deloitte in its “2024 Digital Media Trends” report found more than a third of Americans no longer think subscription VOD is worth the price they are paying.

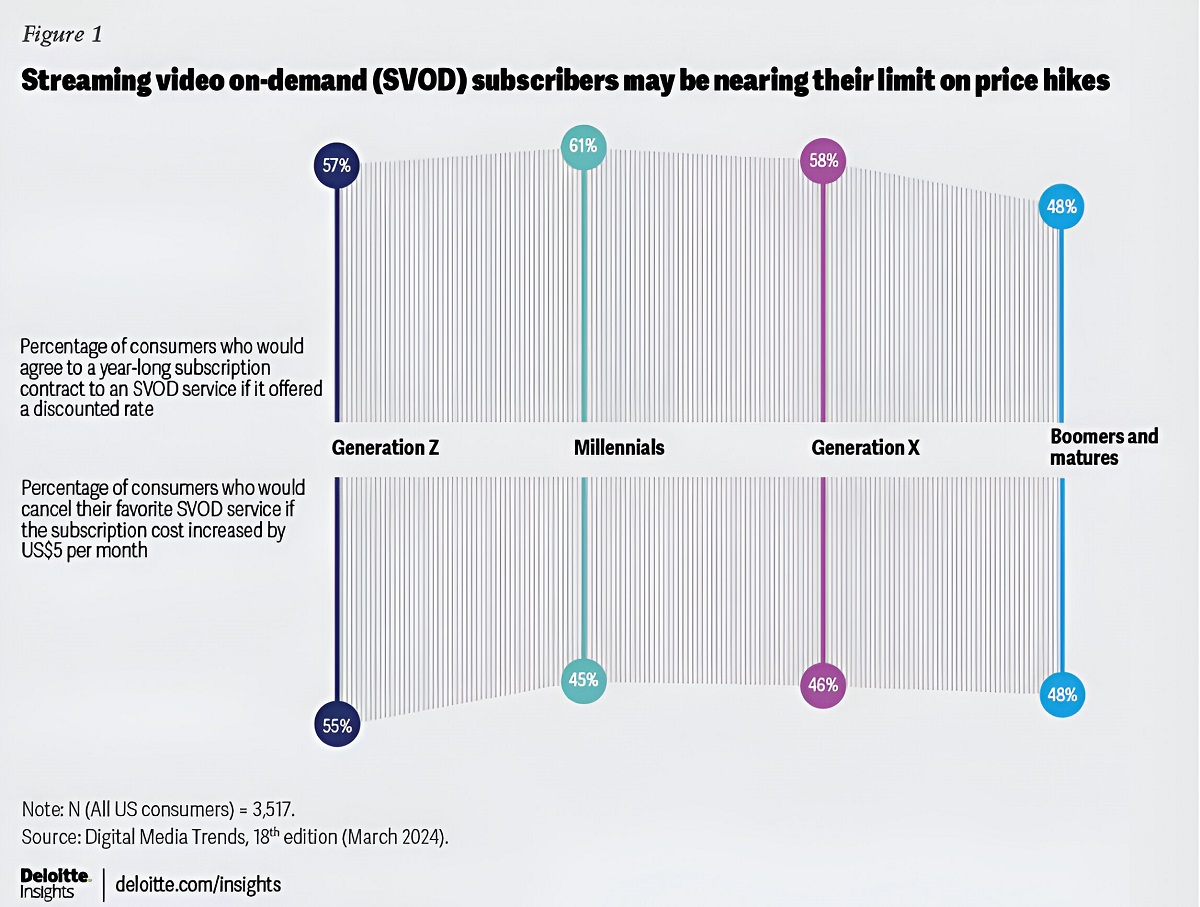

On average, Deloitte says, US households spend $61 per month on streaming services. That’s a 27% increase over last year’s average of $48 per month. And streaming services might want to think twice before increasing prices further, as nearly half (48%) of the people Deloitte spoke with said they would cancel their streaming service — even their favorite one — if prices went up by $5 per month or more.

“With 36% of Americans surveyed believing content on SVOD isn’t worth the money, providers shouldn’t assume that advertising, bundles, and contracts are enough to help their business,” said Deloitte.

Its survey data shows that US consumers are questioning the value of streaming media while also declaring their unwillingness to ever pay for social media.

“This is a generational shift,” the report stated. With some eldest millennials in their 40s, “it’s no longer merely ‘younger generations’ who are giving their time equally to TV and movies, social media and user-generated content, and immersive and social gaming.”

Cancellations are already a problem for the industry, notes Chris Morris, analyzing the Deloitte report at Fast Company. Deloitte reports that 40% of consumers have cancelled a streaming service in the past six months.

READ MORE: More than a third of streaming subscribers say it’s not worth the price (Fast Company)

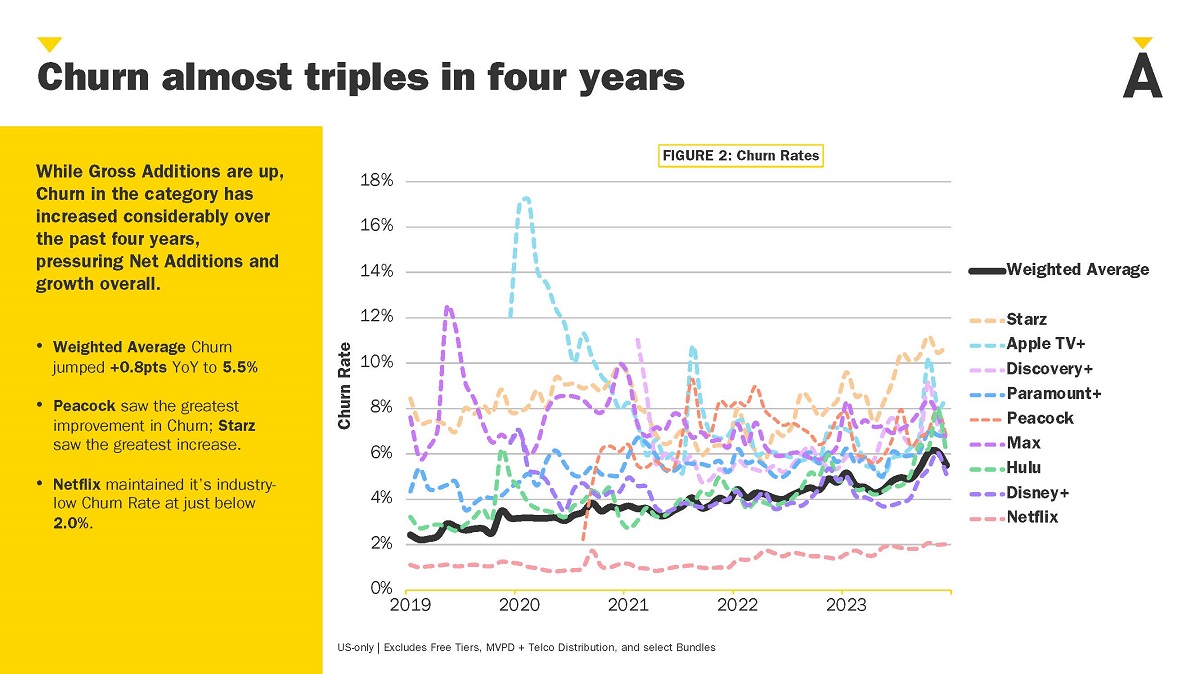

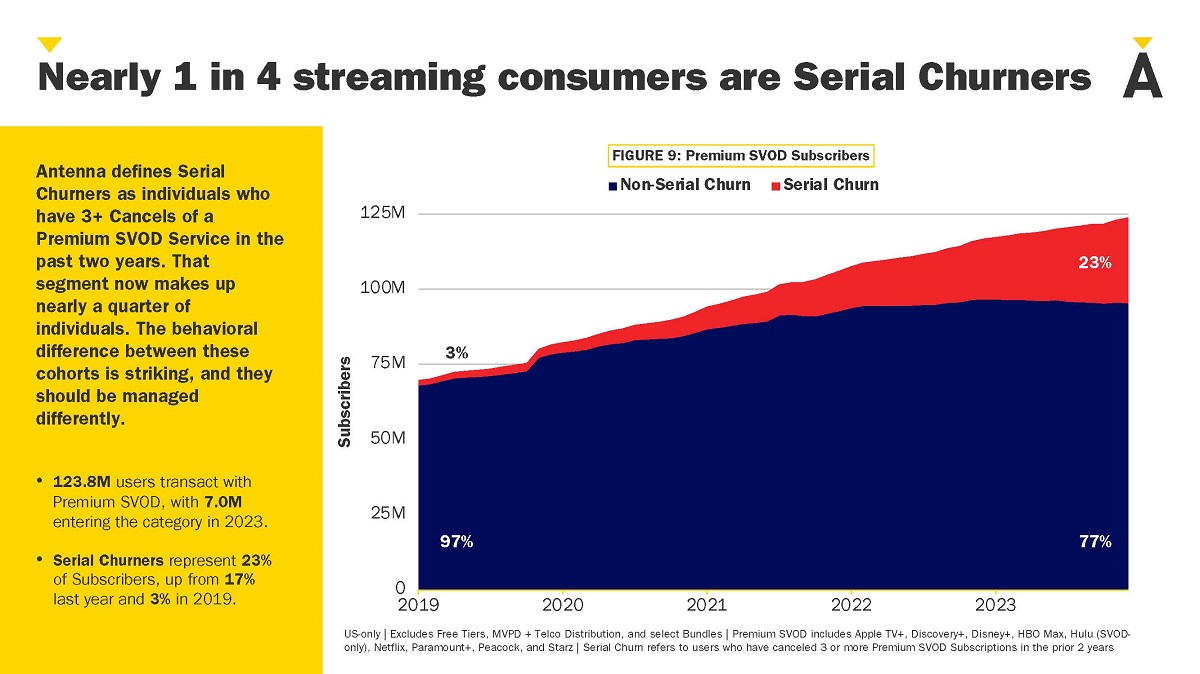

Antenna found that churn had tripled in the last four years, pressuring net additions and growth overall. It also identified a category of “Serial Churners” — individuals who have three or more cancellations of a premium SVOD service in the past two years. That segment now comprises nearly a quarter of users.

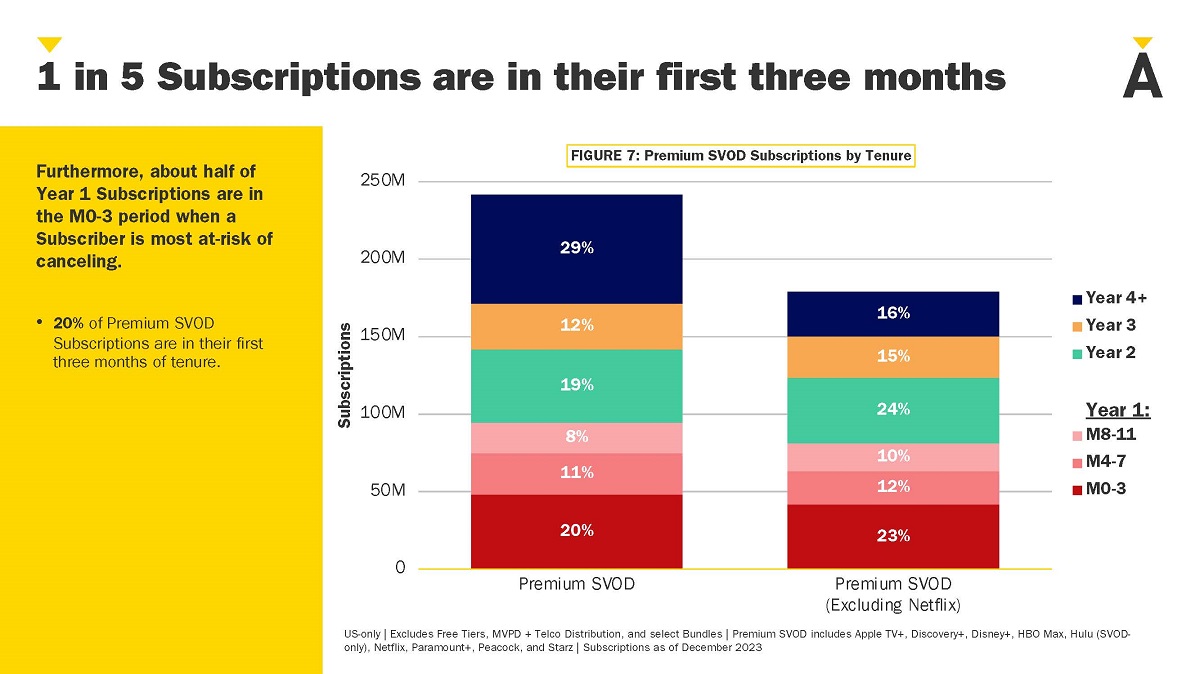

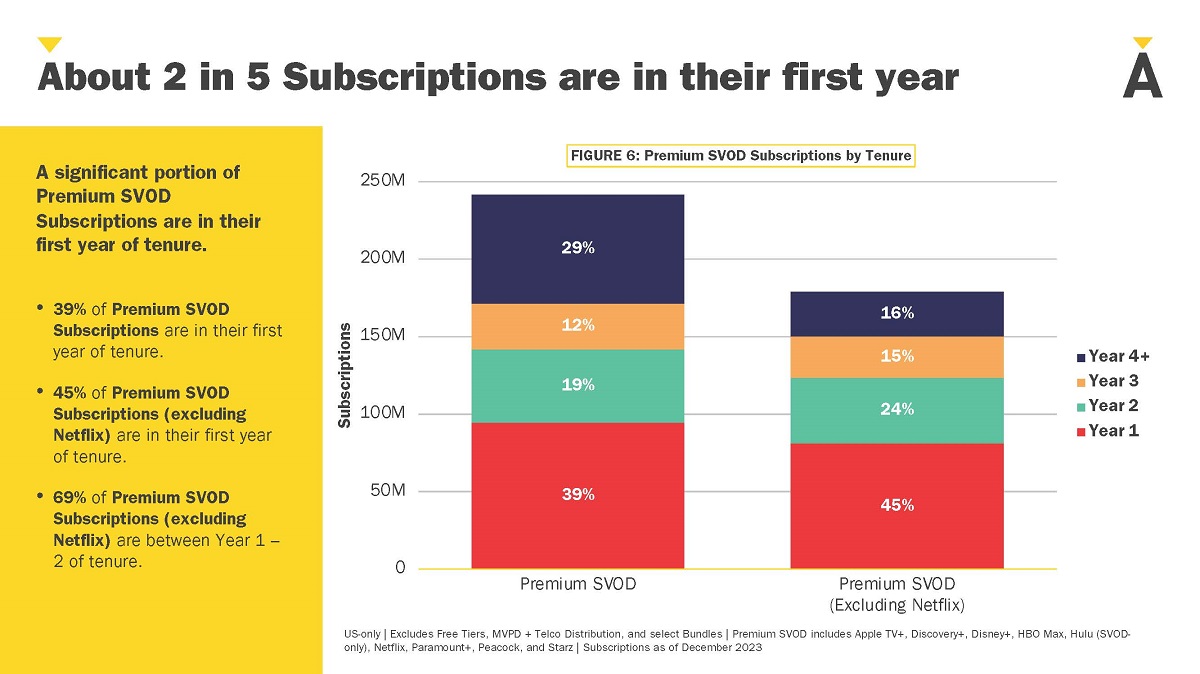

Antenna attributes the overall increase in churn to the surge in mergers and acquisitions among the major streamers since 2019. Almost half of Premium SVOD Subscriptions (excluding Netflix) are in their first year of tenure, it notes.

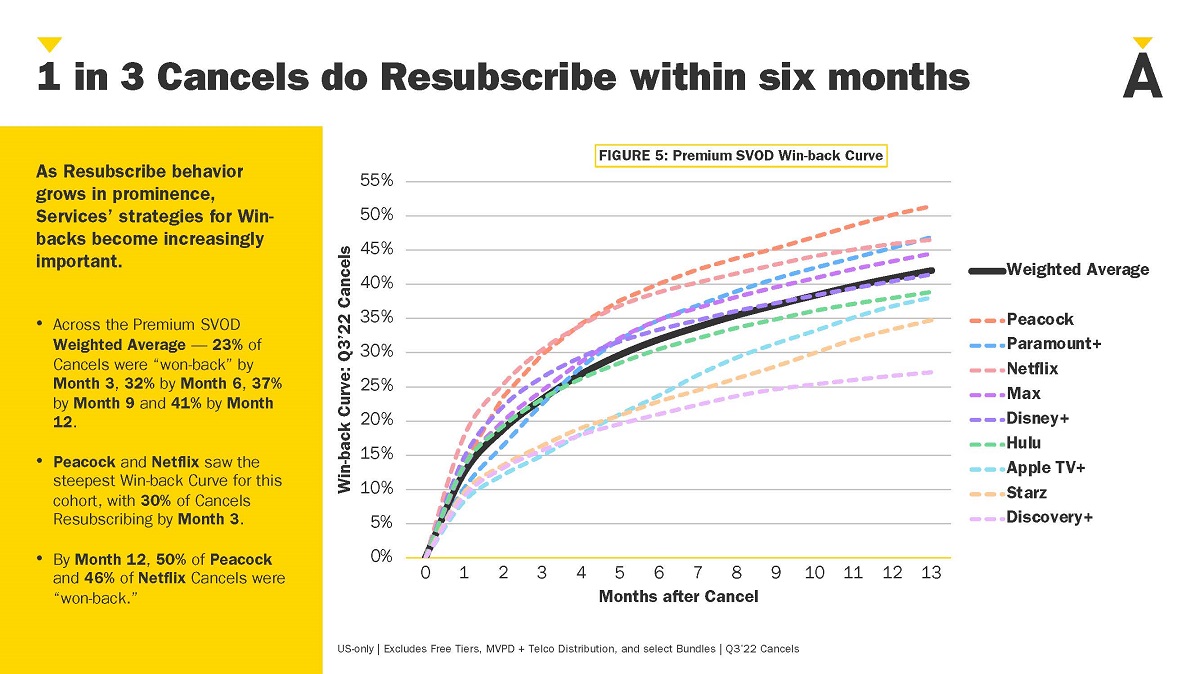

On the plus side, 10% of cancellations resubscribe the next month, and one in three are back by six months after cancelling.

Antenna concludes that if the previous stage of the streamer business model was focused on acquisition to amass scale, the next stage necessitates a shift to managing their subscribers.

“This will translate to much more sophisticated marketing and product strategies, new success KPIs, and a whole lot more reliance on data,” says Antenna, which of course can deliver all of this.

READ MORE: Antenna Q1’24 State of Subscriptions Report: Premium SVOD (Antenna)

Part of the problem is that viewer’s time is being more and more fragmented away from TV, away from streaming TV and onto social media sites and video games.

As Deloitte put it in its report, “Streaming video at a crossroads: Redesign yesterday’s models or reinvent for tomorrow?,” consumer expectations of M&E may now be shaped more by social media, content creators, and video games than by TV and films. How people weigh the value of entertainment options appears to be changing shape as well.

“The biggest challenge for SVOD providers and studios may be that they are no longer addressing a mass culture, but rather a fragmented landscape of competing digital entertainment options,” Deloitte execs state. “Trying to rebuild pay TV business models around streaming services could help reduce SVOD churn and slow attrition in the near term, but the long game for success will likely involve reinventing the medium to be more personalized, more shoppable, and more social.”

Providers will also likely need to widen their scope beyond TV and films to reach modern audiences, it suggests, and make their IP work across social and video games.

“The industry has had 20 years to understand the size and shape of the streaming disruption. Now they should come together to work to build something truly contemporary.”

This would include partnering with social media creators and influencers to facilitate “discovery, hype, and trust,” and using generative AI to improve the quality of content creation. However, Deloitte warns that this could also “lead to a flood of cheap and novel content that further dissolves the boundaries between ‘real’ and synthetic, commodity and premium.”

READ MORE: Streaming video at a crossroads: Redesign yesterday’s models or reinvent for tomorrow? (Deloitte)

Simultaneously, free video stacking is still on the rise. YouTube’s continued growth as the top video service provider in key markets, is charted by Omdia. Strong growth in other social video platforms and Free ad-supported television (FAST) services sees free as the major streaming strategy that all major SVOD services are leaning into.

Also in Europe, the legacy of public service broadcasting remains strong, with traditional free TV and broadcaster video on demand (BVOD) services in high demand.

“The allure of social media platforms such as TikTok and Instagram Reels has reshaped how individuals consume video content,” says Omdia analyst Maria Rua Aguete. “The appetite for free content is ever-increasing and the major streamers are clearly leaning into this as a strategy. With engaging formats and vast user bases, social media services offer compelling alternatives to mainstream streaming services.”

READ MORE: YouTube tops most popular video services as free viewing increases lead over SVOD (Omdia)

Why subscribe to The Angle?

Exclusive Insights: Get editorial roundups of the cutting-edge content that matters most.

Behind-the-Scenes Access: Peek behind the curtain with in-depth Q&As featuring industry experts and thought leaders.

Unparalleled Access: NAB Amplify is your digital hub for technology, trends, and insights unavailable anywhere else.

Join a community of professionals who are as passionate about the future of film, television, and digital storytelling as you are. Subscribe to The Angle today!